Picture supply: Getty Pictures

Alphabet (NASDAQ:GOOGL) shares are on my watchlist. The inventory’s fallen 11% over the previous month and much more from its early February highs. Due to this dip, the inventory’s one-year efficiency is now simply 10%.

As such, £10,000 invested a yr in the past would now be price slightly below £11,000. That’s additionally factoring in the truth that Alphabet shares are denominated in {dollars} and the pound has appreciated barely over the previous yr.

Clearly, this isn’t a foul return. Nevertheless, whereas Alphabet lacks the flicker of a few of its mega-cap, huge tech friends, I’m beginning to surprise if it’s a bit of missed.

What the info tells us

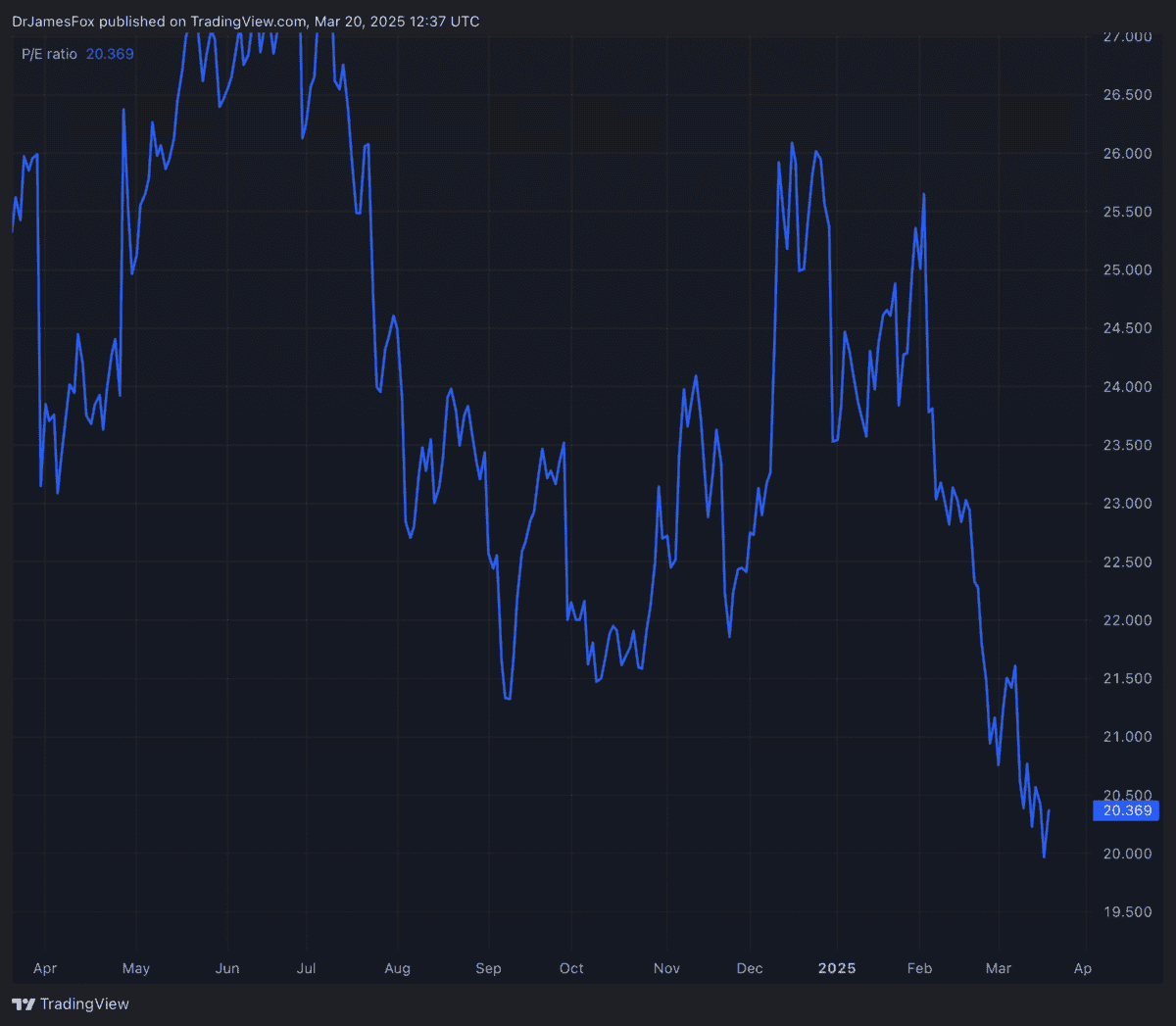

Let’s begin with the boring however most vital half. By way of valuation, Alphabet’s ahead price-to-earnings (P/E) ratio is eighteen.3 instances, which does signify a big premium to the communication companies sector common (13.3 instances), however a reduction to the knowledge know-how sector common (21.8 instances).

It’s additionally a budget ‘Magnificent Seven’ inventory, based mostly on the ahead P/E ratio. The closest peer is Meta, at 23.5 instances.

Alphabet’s price-to-earnings-to-growth (PEG) ratio can be a key signal of an undervalued inventory. At present, Alphabet’s PEG ratio stands at 1.10, which is decrease than the communication service sector median of 1.27 and knowledge know-how sector 1.67. The metric’s achieved by dividing the ahead P/E ratio (18.3) by the anticipated earnings progress price. Curiously, that is additionally the second-cheapest PEG ratio among the many Magnificent Seven, except Nvidia.

This mix of a stable money place, manageable debt, and enticing valuation is definitely interesting to me. Alphabet has $95.6bn in money, although its latest buy of Wiz might need barely lowered this. Whole debt present sits at $28.1bn.

Catalysts and dangers

Alphabet’s a tech big with its enterprise power coming from its dominant place in digital promoting. It controls extra that 90% of the search market share, and continues to see progress is YouTube and Google Cloud. Collectively, its diversified income streams, together with cloud companies and {hardware}, present stability amid sector shifts.

Catalysts embody Waymo’s enlargement, together with key markets like Tokyo and Silicon Valley, marking its first worldwide foray and scaling autonomous ride-hailing companies. Partnerships with Uber and plans to extend rides from 200,000+ per week spotlight near-term progress potential.

Lengthy-term prospects embody the enterprise’s investments in quantum computing. Alphabet’s Willow processor lately demonstrated breakthroughs in error discount and processing velocity, although commercialisation stays years away. And whereas there are many small rivals on this sector, I’m backing a mega-cap inventory like Alphabet to be the primary to commercialise the know-how.

Nevertheless, dangers loom from regulatory scrutiny (antitrust instances), synthetic intelligence (AI) competitors and excessive capital expenditure, which might put strain on profitability. What’s extra, Google Cloud’s slower-than-expected progress and quantum computing’s unproven practicality add uncertainty as we glance additional into the longer term. Tesla will even be a significant competitor in autonomous ride-hailing when it catches up.

Nonetheless, I’m nonetheless contemplating including this inventory to my portfolio. Along with the above, the Relative Energy Index — a technical indicator that measures share worth actions — suggests the inventory’s near ‘oversold’ territory.

Explore the world of BitStarz, grab your crypto welcome pack: $500 + 180 FS, awarded Best Casino multiple times. BitStarz mirror helps bypass restrictions.

Stay in control with a verified casino mirror

Smart players always keep a casino mirror link saved for emergencies.

Echte Gewinnchancen und hohe Limits � nur bei LeonBet.