Picture supply: Getty Pictures

On the lookout for one of the best low-cost UK progress shares to purchase for the New Yr? Listed below are two of my favourites.

Marston’s

Buying and selling circumstances have gotten more and more troublesome for the normal public home. Altering shopper habits, low-cost grocery store booze, and hovering prices have all smashed profitability acros the sector.

Mixed, these pressures have seen 2,000 pubs shut their doorways for good because the begin of 2020, based on Altus Group.

However Metropolis analysts don’t maintain any fears for Marston’s (LSE:MARS). They count on robust earnings progress during to monetary 2027, because the desk under reveals.

| Monetary yr ending 30 September | Predicted progress |

|---|---|

| 2025 | 56% |

| 2026 | 15% |

| 2027 | 12% |

Marston’s isn’t proof against broader pressures within the pub sector. However its gross sales are outperforming the broad trade due to its diversified property. Its portfolio contains a fair unfold of differentiated venues out of your native conventional pub to sports activities pubs, grownup eating pubs, and household pubs.

It’s a recipe that’s proving to be a winner. Reported and like-for-like revenues had been up 3% and 4.8% within the final fiscal yr, pushing underlying working revenue 17.9% larger.

Market-beating gross sales aren’t the one spectacular factor at Marston’s. Margins are booming due to initiatives like reducing labour and vitality prices, altering pub menus, and bettering income per buyer.

Final yr, the underlying EBITDA margin leapt 190 foundation factors to 21.4%. And Marston’s is focusing on margin growth “of 200-300 foundation factors” from this level on as its effectivity technique rolls on.

I’m nonetheless a bit involved concerning the excessive ranges of debt the pub operator’s servicing. This has dropped considerably, however net-debt-to-EBITDA was nonetheless excessive at 6.5 instances as of September.

However the cheapness of Marston’s shares nonetheless makes it price a really shut look, in my view. Its ahead price-to-earnings (P/E) ratio is 5.4 instances, whereas its price-to-earnings progress (PEG) a number of is simply 0.1.

Any studying under one implies {that a} inventory is undervalued.

TBC Financial institution

Political uncertainty in Georgia makes investing in its native corporations larger threat than regular. The financial influence of whether or not the nation chooses nearer ties to Russia or the EU shall be vital.

But some Georgian shares are so low-cost they’re nonetheless price an in depth look, in my opinion. TBC Financial institution (LSE:TBCG), as an example, has a ahead P/E ratio of three.9 instances and a PEG ratio of 0.2.

A low valuation isn’t the one enticing factor that TBC Financial institution shares with Marston’s. Because the desk reveals, earnings listed below are additionally tipped to proceed taking off:

| Monetary yr ending 31 December | Predicted progress |

|---|---|

| 2025 | 20% |

| 2026 | 19% |

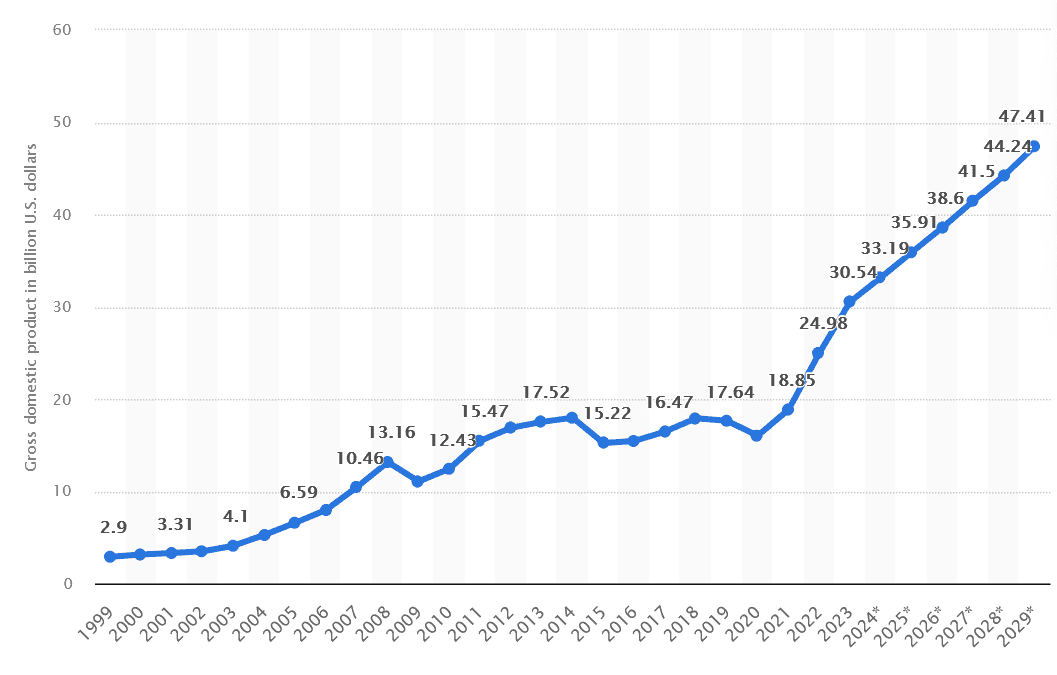

This isn’t a shock (to me a minimum of) given the continuing energy of Georgia’s economic system. Newest information confirmed GDP develop a whopping 11% in quarter three, the form of determine the UK — and with it home banks like Lloyds — can solely dream of.

Cyclical shares like TBC Financial institution are reaping the rewards of this breakneck progress. Due to hovering mortgage demand, TBC’s pre-tax revenue leapt 19.1% within the three months to September.

WIth low banking product penetration persisting, I’m anticipating the financial institution to proceed having fun with staggering earnings progress because the economic system grows. Analysts at Statista predict supportive GDP progress to proceed to 2029 a minimum of, as proven under:

It’s not with out threat, as I point out. However the risk for additional substantial earnings and share worth progress makes TBC a progress share to think about.