Godrej Agrovet Ltd. – Feed-to-Meals Agri Enterprise

Based in 1991 and headquartered in Mumbai, Godrej Agrovet Restricted is one in every of India’s main built-in meals and agri-business firms with a diversified presence throughout the agricultural worth chain. The corporate operates throughout key segments together with Animal Vitamin, Crop Care, Dairy, Meals, and Oil Palm, and holds management positions in a number of classes, together with being India’s largest producer of crude palm oil and a number one participant within the animal feed business. By means of its three way partnership with ACI Restricted, the corporate additionally has a robust presence in Bangladesh’s animal diet market. Godrej Agrovet operates a widespread manufacturing community with over 60 manufacturing amenities throughout India.

Merchandise and Providers

The corporate operates throughout diversified agri and meals companies, catering to a number of segments of the agricultural worth chain:

- Animal Vitamin – Provides a variety of animal feed merchandise throughout cattle, poultry, and aqua feed segments, with a robust pan-India presence.

- Oil Palm Enterprise – India’s largest producer of crude palm oil, engaged in oil palm plantation growth and processing.

- Crop Care – Offers agrochemical and crop safety options catering to the whole crop lifecycle, together with plant progress regulators, herbicides, pesticides, and fungicides.

- Dairy Enterprise – Markets milk and value-added dairy merchandise beneath the Godrej Jersey model.

- Poultry & Processed Meals – Provides poultry merchandise and ready-to-cook/snack merchandise beneath the Actual Good Hen and Yummiez manufacturers.

- Astec LifeSciences – Engaged within the manufacturing of energetic components, intermediates, and formulations for the agrochemical business via Astec LifeSciences Restricted.

Subsidiaries – As of FY25, the corporate has 7 subsidiaries and 1 three way partnership.

Funding Rationale

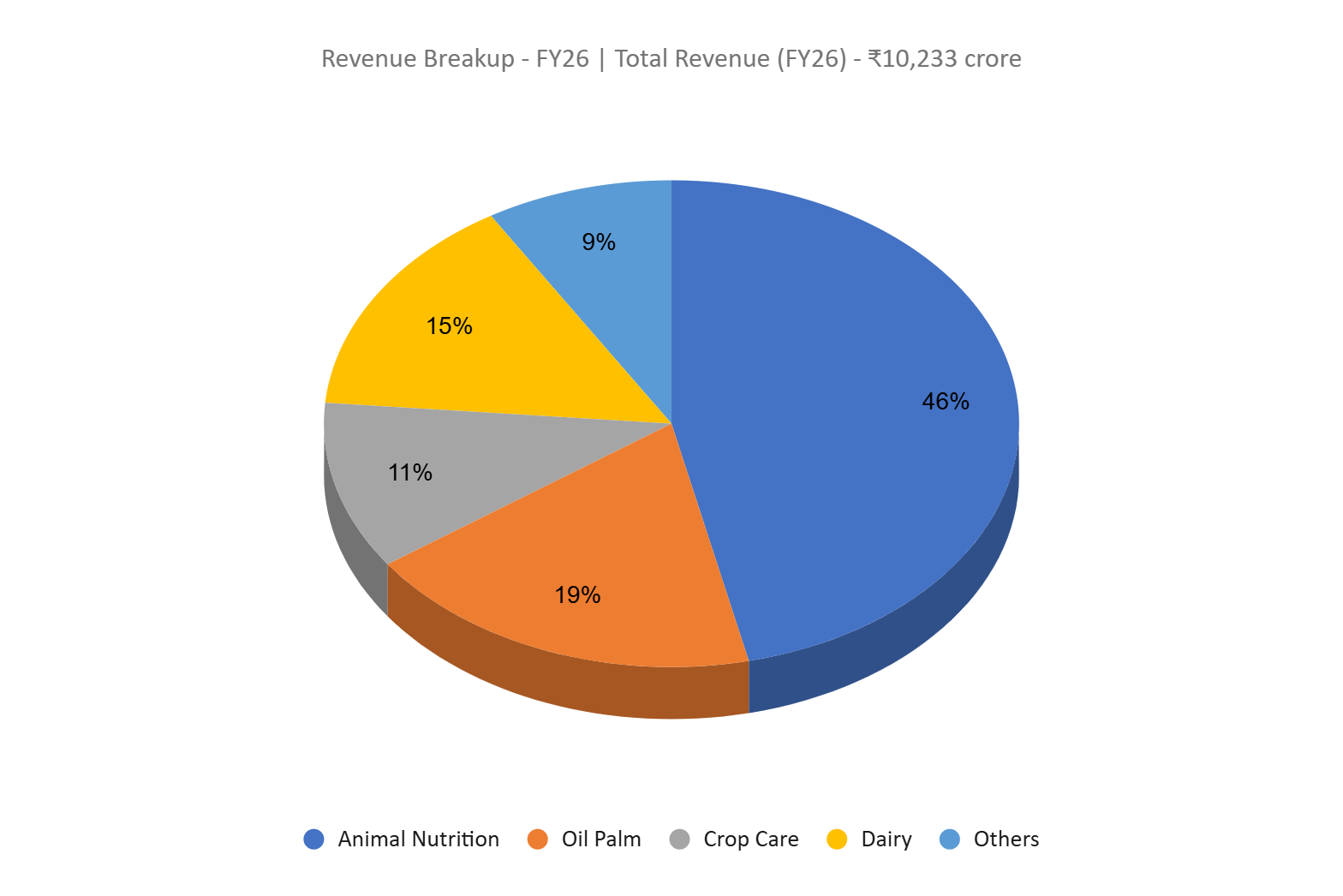

- Animal Vitamin enterprise witnessing robust volume-led progress with bettering profitability – The corporate’s Animal Vitamin section, contributing practically 46% of total revenues, continued to ship robust broad-based progress, with volumes rising 12% in FY26 and additional accelerating to fifteen% YoY in Q4FY26. Progress was led by the cattle feed section, the place volumes elevated 24% YoY through the quarter, supported by rising demand and deeper market penetration. The corporate’s growth past its historically robust Western India markets into Central and Japanese India has began yielding tangible outcomes, offering incremental progress avenues. Moreover, the growing contribution from premium and value-added merchandise resembling Dhanalaxmi G and Bypro Plus aided each realisations and product combine enchancment. Operational efficiencies and higher combine led to EBIT margin growth to 10.4% in Q4FY26 versus 5.7% within the corresponding interval final yr. Section EBIT grew 20% YoY throughout FY26, reflecting the sustainability of earnings enchancment pushed by geographic growth, premiumisation, and powerful execution.

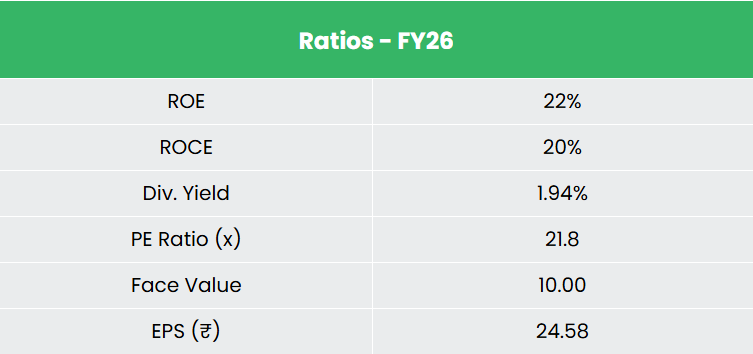

- Enhancing capital effectivity and restoration throughout companies to assist earnings progress – The corporate has witnessed a pointy enchancment in capital effectivity over the past three years, with ROCE bettering from 13% in FY24 to 16% in FY25 and additional to twenty% in FY26. The development has been pushed largely by higher working capital administration, as internet working capital days decreased considerably from 45 days in FY24 to 25 days in FY26, releasing practically ₹486 crore of capital. On the profitability entrance, PBT grew 17% YoY to ₹569 crore in FY26 regardless of income progress of 9%, indicating significant margin growth and improved operational effectivity. Notably, this efficiency got here regardless of weak point in sure segments, together with decrease crop care margins, stress within the dairy enterprise, and income decline in Godrej Meals. Trying forward, the corporate seems well-positioned for a broader earnings restoration in FY27. Astec LifeSciences has improved from EBITDA losses to breakeven and is concentrating on wholesome income progress, whereas the crop care enterprise is predicted to get well from Q2FY27 supported by channel stock normalisation and scaling up of latest merchandise resembling Takai and Ashitaka. Moreover, easing milk procurement price pressures and bettering branded product combine within the Meals section are more likely to assist margin restoration. Administration has guided for early double-digit income progress together with mid-teen PBT progress in FY27, which may additional strengthen profitability as a number of enterprise segments contribute concurrently.

- Q4FY26 – In the course of the quarter, the corporate generated its highest ever quarterly income of ₹2,333 crore, a rise of 9.3% in comparison with the ₹2,134 crore of Q4FY25. EBITDA elevated from ₹160 crore of Q4FY25 to ₹173 crore of Q4FY26, a progress of 8.5%. The corporate reported internet revenue of ₹74 crore, a rise by 11.3% YoY in comparison with ₹66 crore of the corresponding interval of the earlier yr.

- FY26 – In the course of the FY, the corporate generated income of ₹10,233 crore, a rise of 9.1% in comparison with the FY25 income. EBITDA is at Rs.936 crore, up by 10.8% YoY. The corporate reported internet revenue of Rs.440 crore, a rise of 13.9% YoY.

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 3% and 26% respectively between FY24-26. The corporate has a wholesome capital construction with a debt-to-equity ratio of 0.77. Common 3-year ROE and ROCE is round 18% and 17% for FY24-26 interval.

Trade

India’s agriculture and allied sector is a structural pillar of the economic system, contributing ~18% of GDP and using practically half the workforce. The nation holds dominant international positions – largest cattle herd, largest space beneath wheat, rice and cotton, and the world’s prime producer of milk, pulses and spices. The sector is projected to maintain ~4% progress over the following decade, supported by rising home meals demand, growing mechanisation and know-how adoption, and a strengthening export pipeline. Inside agriculture, livestock has emerged because the faster-growing sub-sector, increasing at a 7.1% CAGR over the previous decade versus ~3.5% for crops, now contributing ~16% of farmers’ revenue – a structural shift that’s reshaping how capital and coverage consideration is allotted throughout the sector. Taken collectively, India’s inherent agricultural scale, beneficial demographics, and an more and more organised agribusiness panorama create a sturdy long-term progress backdrop for the sector.

Progress Drivers

- The Union Cupboard authorised the Prime Minister Dhan-Dhaanya Krishi Yojana (PMDDKY) price ₹24,000 crore (US$ 2.79 billion) from FY26 to assist the sector.

- The Division of Agriculture and Farmers’ Welfare price range has grown from ₹21,934 crore in FY2013-14 to roughly ₹1,30,692 crore in FY2026-27, reflecting a ~6x enhance in authorities agricultural spending over the previous decade.

- The Division of Animal Husbandry and Dairying acquired its highest-ever price range allocation of ₹6,153 crore in FY2026-27, a 27% soar year-on-year.

Peer Evaluation

Rivals: Avanti Feeds Ltd, Mukka Proteins Ltd, and many others.

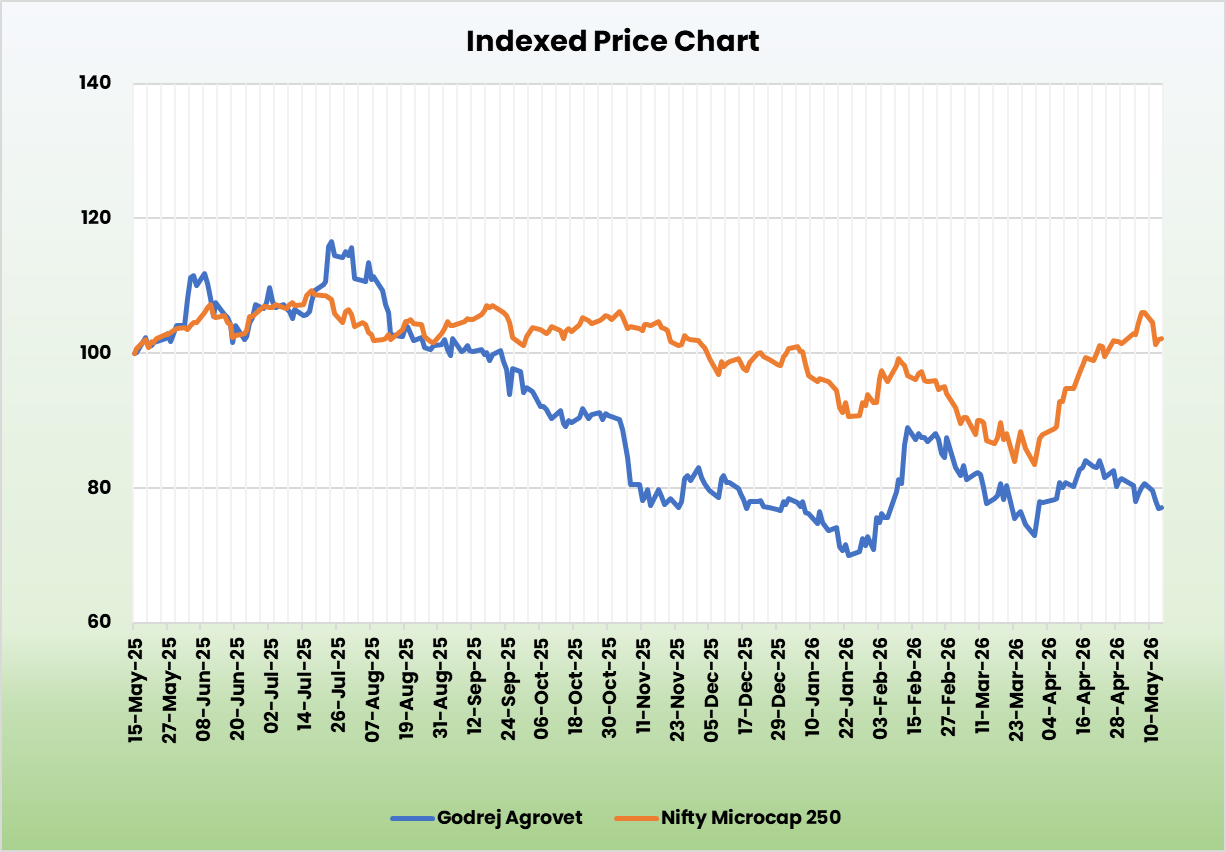

Compared to the above opponents, Godrej Agrovet is a fairly valued inventory with wholesome returns on the capital employed and secure progress in gross sales.

Outlook

Godrej Agrovet enters FY27 with administration guiding early double-digit income progress and mid-teens PBT progress. The animal diet enterprise, which drove the FY26 story, is sustaining momentum with broad-based quantity progress and geographic growth into Central and East India nonetheless in early phases. Oil palm provides one other quantity progress lever with early double-digit growth anticipated in FY27. On capital allocation, the corporate has guided ₹400 crore in complete capex with ~₹100-125 crore money surplus remaining, and a long-term capex framework of ~₹350 crore yearly with 75-80% directed towards progress. With working capital days compressed to 25, ROCE at 20% and bettering, and drag companies like Astec and Godrej Meals now turning round, FY27 is about up as the primary yr the place most segments contribute concurrently.

Valuations

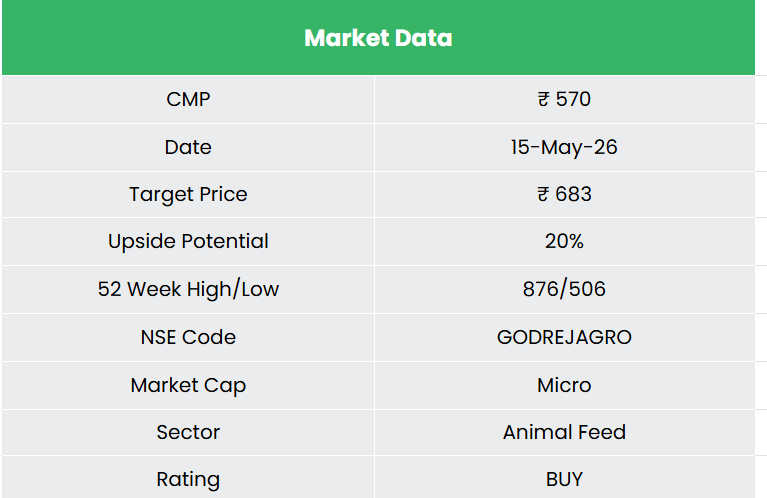

We anticipate Godrej Agrovet to proceed its progress momentum underpinned by accelerating quantity momentum in branded cattle feed, an bettering combine in value-added poultry and dairy, and an anticipated restoration in crop safety and Astec LifeSciences in FY27. We suggest a BUY ranking within the inventory with the goal worth (TP) of ₹683, 26x FY28E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully.

SWOT Evaluation

| Power | Weak spot |

|

|

| Alternatives | Threats |

|

|

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM on no account assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Publish Views:

30

{kind=link}