AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $0.21

EPS YoY -25.0%|Rev YoY +71.5%|Web Margin -275.2%

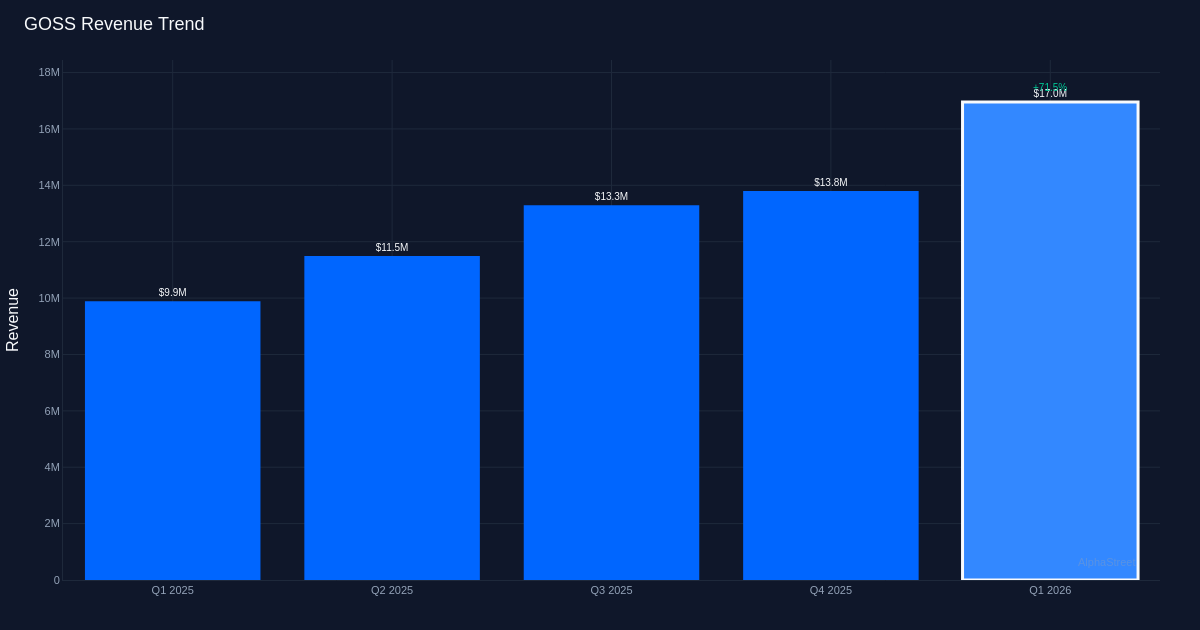

Gossamer Bio stumbled in Q1 2026, posting a loss per share of $0.20 that missed analyst expectations by 17.6%, marking the corporate’s incapability to beat estimates in its final reported quarter. The biotechnology agency continues to burn money regardless of notable income development, as its web margin of -274.7% underscores the persistent hole between top-line growth and profitability. The miss got here regardless of income reaching $17.0 million, up 71.5% year-over-year, suggesting operational bills and monetary obligations are outpacing the corporate’s skill to monetize its platform.

The standard of the quarter’s outcomes reveals an intriguing paradox: accelerating income alongside deteriorating absolute losses. Whereas the corporate’s web lack of $46.7 million seems worse than the prior 12 months’s $36.6 million in absolute phrases, the crucial metric is margin enchancment. The web margin of -274.7% represents a considerable 95.0 proportion level enchancment from the year-ago interval’s -369.7%, indicating that income is scaling sooner than losses are accumulating. Working margin equally improved to -263.9%, although the corporate stays deeply cash-flow unfavourable. This sample is attribute of clinical-stage biotechs ramping business actions, however the magnitude of losses relative to income suggests the corporate continues to be removed from a sustainable financial mannequin.

Income trajectory reveals constant sequential acceleration throughout 4 quarters, establishing a reputable development narrative at the same time as profitability stays elusive. The development from $11.5 million in Q2 2025 to $13.3 million in Q3, $13.8 million in This fall, and now $17.0 million in Q1 2026 demonstrates consecutive quarterly development with enhancing momentum. The 23.2% sequential leap from This fall to Q1 is especially notable on condition that first quarters typically face seasonal headwinds in pharmaceutical commercialization. This trajectory suggests underlying demand is strengthening, although the modest absolute income base means the corporate requires a number of quarters of comparable development earlier than reaching scale that might materially affect its money burn fee.

Administration’s strategic give attention to debt restructuring emerged as a key theme, with the corporate reaching substantial stability sheet reduction that extends its operational runway. As administration said in ready remarks, “This takes our excellent convertible debt from 200 million all the way down to 72 million, a discount of $128 million and extends our debt maturity from 2027 to 2030.” This restructuring is crucial context for deciphering the quarter’s miss—the corporate seems to be prioritizing monetary flexibility over near-term earnings optimization. With money, money equivalents and marketable securities of $99.2 million as of quarter-end, administration indicated, “Based mostly on our present plans, we count on our money runway to increase into the primary quarter of 2027.” This nine-month runway is regarding for a clinical-stage biotech, suggesting imminent capital wants except income development accelerates dramatically or further financing materializes.

The corporate’s improvement pipeline commentary revealed ongoing uncertainty round key scientific knowledge timelines, which can clarify investor warning. When pressed on scientific trial length, administration acknowledged, “In regards to the questions at 48 weeks of 72 weeks, we don’t have the information but, however we are going to look into it.” This lack of readability on pivotal trial readouts introduces execution threat that compounds the corporate’s money runway issues. For a biotech buying and selling at $0.21 per share, knowledge visibility is paramount.

The loss-per-share deterioration from $0.16 a 12 months in the past to $0.20 at the moment represents a 25.0% widening that conflicts with the margin enchancment narrative, pointing to share depend growth as a probable offender. This disconnect between enhancing margins and worsening per-share losses usually indicators dilutive financing actions, which might be per a clinical-stage firm managing a good money place. The debt restructuring talked about by administration could have concerned fairness elements that elevated the share depend, a typical tradeoff biotech managements settle for to safe runway extension. Traders ought to scrutinize the totally diluted share depend within the full submitting to evaluate the magnitude of dilution absorbed throughout the quarter.

The inventory’s 35% fall suggests the market is discounting the top-line beat towards the EPS miss and looming money wants. At this value degree, the corporate probably trades effectively beneath money per share even after accounting for debt obligations, implying the market assigns minimal worth to the business franchise and pipeline. With out readability on when losses will slender materially or when the following financing will happen, the inventory stays in a precarious place.

What to Watch: The crucial catalyst is whether or not Q2 2026 income can maintain sequential development above 20% to display the Q1 acceleration wasn’t an anomaly. Traders ought to monitor any bulletins concerning the scientific trial timelines that administration indicated require additional evaluation, as knowledge readouts may function inflection factors for valuation. The primary quarter 2027 money runway deadline means financing exercise—whether or not fairness raises, partnerships, or further debt restructuring—will probably materialize inside the subsequent two quarters. Lastly, look ahead to up to date steering on the trail to money circulate breakeven; with no credible timeline to profitability, continued dilution seems inevitable no matter income development charges.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market data. Human editors confirm content material.