This submit on Bayesian inference is the second of a multi-part sequence on Bayesian statistics and strategies utilized in quantitative finance.

In my earlier submit, I gave a leisurely introduction to Bayesian statistics and whereas doing so distinguished between the frequentist and the Bayesian outlook of the world. I dwelt on how every of their underlying philosophies influenced their evaluation of varied probabilistic phenomena. I then mentioned the Bayes’ Theorem together with some illustrations to assist lay the constructing blocks of Bayesian statistics.

Intent of this Put up

My goal right here is to assist develop a deeper understanding of statistical evaluation by specializing in the methodologies adopted by frequentist statistics and Bayesian statistics. I consciously select to deal with the programming and simulation facets utilizing Python in my subsequent submit.

I now instantiate the beforehand mentioned concepts with a easy coin-tossing instance tailored from “Introduction to Bayesian Econometrics (2nd Version)”.

Instance: A Repeated Coin-Tossing Experiment

Suppose we’re focused on estimating the bias of a coin whose equity is unknown. We outline θ (the Greek letter ‘theta’) because the likelihood of getting a head after a coin is tossed. θ is the unknown parameter we wish to estimate. We intend to take action by inspecting the outcomes of tossing the coin a number of instances. Allow us to denote y as a realization of the random variable Y (representing the end result of a coin toss). Let Y=1 if a coin toss leads to heads and Y=0 if a coin toss leads to tails. Basically, we’re assigning 1 to heads and 0 to tails.

∴ P(Y=1|θ)=θ ; P(Y=0|θ)=1−θ

Primarily based on our above setup, Y may be modelled as a Bernoulli distribution which we denote as

Y ∼ Bernoulli (θ)

I now briefly view our experimental setup by means of the lens of the frequentist and the Bayesian earlier than continuing with our estimation of the unknown parameter θ.

Two Views on the Experiment Setup

In classical statistics (i.e. the frequentist method), our parameter θ is a set however unknown worth mendacity between 0 and 1. The information we acquire is one realization of a recurrent (i.e. repeating this n-toss experiment say N instances) experiment. Classical estimation methods like the tactic of most probability are used to reach at θ̄̂ (known as ‘theta hat’), an estimate for the unknown parameter θ. In statistics, we normally categorical an estimate by placing a hat over the title of the parameter. I dilate this concept within the subsequent part. To restate what has been stated beforehand, we observe that within the frequentist universe, the parameter is fastened however the information is various.

Bayesian statistics is basically totally different. Right here, the parameter θ is handled as a random variable since there may be uncertainty about its worth. It, subsequently, is sensible for us to treat our parameter as a random variable which can have an related likelihood distribution. In an effort to apply Bayesian inference, we flip our consideration to one of many elementary legal guidelines of likelihood principle, Bayes’ Theorem that we had seen beforehand.

I exploit the mathematical type of Bayes’ Theorem as a strategy to set up a reference to Bayesian inference.

……..  (1)

(1)

To repeat what I stated in my earlier submit, what makes this theorem so helpful is it permits us to invert a conditional likelihood. So if we observe a phenomenon and acquire information or proof about it, the concept helps us analytically outline the conditional likelihood of various potential causes given the proof.

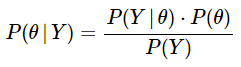

Let’s now apply this to our instance through the use of the notations we had outlined earlier. I label A = θ and B = y. Within the discipline of Bayesian statistics, there are particular names used for every of those phrases which I spell out beneath and use subsequently. (1) may be rewritten as:

…….. (2)

…….. (2)

the place:

P(θ) is the prior likelihood. We categorical our perception in regards to the trigger θ BEFORE observing the proof Y. In our instance, the prior can be quantifying our a priori perception on the equity of the coin (right here we are able to begin with the belief that it’s an unbiased coin, so θ = 1/2). P(Y|θ) is the probability. Right here is the place the true motion occurs. That is the likelihood of the noticed pattern or proof given the hypothesized trigger. Allow us to, with out lack of generality, assume that we acquire 5 heads in 8 coin tosses. Presuming the coin to be unbiased as specified above, the probability can be the likelihood of observing 5 heads in 8 tosses on condition that θ = 1/2. P(θ|Y) is the posterior likelihood. That is the likelihood of the underlying trigger θ AFTER observing the proof y. Right here, we compute our up to date or a posteriori perception on the bias of the coin after observing 5 heads in 8 coin tosses utilizing Bayes’ theorem. P(Y) is the likelihood of the information or proof. We generally additionally name this the marginal probability. That is obtained by taking the weighted sum (or integral) of the probability operate of the proof throughout all potential values of θ. In our instance, we’d compute the likelihood of 5 heads in 8 coin tosses for all potential beliefs about θ. This time period is used to normalize the posterior likelihood. Since it’s impartial of the parameter to be estimated θ, it’s mathematically extra tractable to specific the posterior likelihood as:

P(θ|Y) ∝ P(Y|θ) × P(θ) …….(3)

(3) is crucial expression in Bayesian statistics and bears repeating. For readability, I paraphrase what I stated earlier. Bayesian inference permits us to turnaround conditional chances i.e. use the prior chances and the probability capabilities to offer a connecting hyperlink to the posterior chances i.e. P(θ|Y) granted that we solely know P(Y|θ) and the prior, P(θ). I discover it useful to view (3) as:

Posterior Chance ∝ Probability × Prior Chance ………. (4)

The experimental goal is to get an estimate of the unknown parameter θ based mostly on the end result of n impartial coin tosses. The coin tosses generate the pattern or information y = (y1, y2, …, yn), the place yi is 1 or 0 based mostly on the results of the ith coin toss.

I now present the frequentist and Bayesian approaches to fulfilling this goal. Be happy to cursorily skim by means of the derivations I contact upon right here in case you are not within the arithmetic behind it. You possibly can nonetheless develop enough intuitions and study to make use of Bayesian methods in follow.

Estimating θ: The Frequentist Strategy

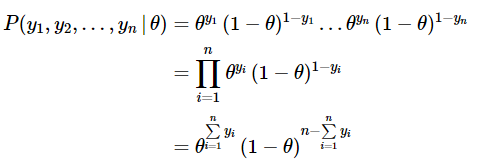

We compute the joint likelihood operate utilizing the utmost probability estimation (MLE) method. The likelihood of the end result for a single coin toss may be elegantly expressed as:

![]()

For a given worth of θ, the joint likelihood of the end result for n impartial coin tosses is the product of the likelihood of every particular person consequence:

……. (5)

……. (5)

As we are able to see in (4), the expression labored out is a operate of the unknown parameter θ given the observations from our experiment. This operate of θ is known as the probability operate and is normally referred to within the literature as:

![]() ……….. (6)

……….. (6)

OR

![]() …………… (7)

…………… (7)

We wish to compute the worth of θ which is most definitely to have yielded the noticed set of outcomes. That is known as the most probability estimate, θ̄̂ (‘theta hat’). For analytically computing it, we trivially take the primary order spinoff of (6) with respect to the parameter and set it equal to zero. It’s prudent to additionally take the second spinoff and examine the signal of its worth at θ = θ̄̂ to make sure that the estimate is certainly the maxima. We frequently usually take the log of the probability operate because it drastically simplifies the dedication of the utmost probability estimator θ̄̂ . It ought to subsequently not shock you that the literature is replete with log probability capabilities and their options.

Estimating θ: The Bayesian Strategy

I now change the notations we now have used to this point to make them a bit of extra exact mathematically. I’ll use these notations all through this sequence now. The rationale for this alteration is in order that we are able to suitably ascribe every time period with symbols that remind us of their random nature. There’s uncertainty over the values of θ, Y, and many others., we, subsequently, regard them as random variables and assign them corresponding likelihood distributions which I do beneath.

Notations for the Density and Distribution Capabilities

- π(⋅) (the Greek letter ‘pi’) to indicate the likelihood distribution operate of the prior (that is pertaining to θ) and π(⋅|y) to indicate the posterior density operate of the parameter we try and estimate.

- f(⋅) to indicate the likelihood density operate (pdf) for steady random variables and p(.) which is the likelihood mass operate (pmf) of discrete random variables. Nevertheless, for simplicity, I exploit f(⋅) regardless of whether or not the random variable Y is steady or discrete.

- The joint density operate will proceed to be denoted as L(θ|⋅). to indicate the probability operate which is the joint density of the pattern values and is normally the product of the pdf’s/pmf’s of the pattern values from our information.

Keep in mind that θ is the parameter we try to estimate.

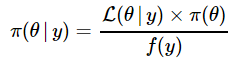

(2) and (3) may be rewritten as

π(θ|y) = [f(y|θ)⋅π(θ)] / f(y) ……(8)

π(θ|y)∝f(y|θ)×π(θ) …………….(9)

Acknowledged in phrases, the posterior distribution operate is proportional to the probability operate instances the prior distribution operate. I redraw your consideration to (4) and current it in congruence with our new notations.

Posterior PDF ∝ Probability × Prior PDF ……….(10)

I now rewrite (8) and (9) utilizing the probability operate L(θ|Y) outlined earlier in (7).

……… (11)

……… (11)

![]() ………..(12)

………..(12)

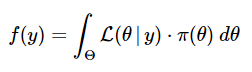

The denominator of (11) is the likelihood distribution of the proof or information. I reiterate what I’ve beforehand talked about whereas inspecting (3): A helpful means of contemplating the posterior density is utilizing the proportionality method as seen in (12). That means, we need not fear in regards to the f(y) time period on the RHS of (11).

For the mathematically curious amongst you, I now take you briefly down a pointless rabbit gap to clarify it incompletely. Maybe, later in our journey, I could write a separate submit brooding on these trivialities.

In (11), f(y) is the proportionality fixed that makes the posterior distribution a correct density operate integrating to 1. After we look at it extra carefully, we see that’s, actually, the unconditional (marginal) distribution of the random variable Y. We will decide it analytically by integrating over all potential values of the parameter θ. Since we’re integrating out θ, we discover that f(y) doesn’t rely on θ.

OR

(11) and (12) symbolize the steady variations of the Bayes’ Theorem.

The posterior distribution is central to Bayesian statistics and inference as a result of it blends all of the up to date details about the parameter θ in a single expression. This contains details about θ earlier than the observations have been inspected and that is captured by means of the prior distribution. The data contained within the observations is captured by means of the probability operate.

We will regard (11) as a technique of updating data and this concept is additional exemplified by the prior-posterior nomenclature.

- The prior distribution of θ, π(θ) represents the data out there about its potential values earlier than recording the observations y.

- The probability operate L(θ|y) of θ is then decided based mostly on the observations y.

- The posterior distribution of θ, π(θ|y) summarizes all of the out there details about the unknown parameter θ after recording and incorporating the observations y.

The Bayesian estimate of θ can be the weighted common of the prior estimate and the utmost probability estimate, θ̄̂ . Because the variety of observations n will increase and approached infinity, the burden on the prior estimate approaches zero and the burden on the MLE approaches one. This suggests that the Bayesian and frequentist estimates would converge as our pattern measurement will get bigger.

To make clear, in a classical or frequentist setting, the standard estimator of the parameter, θ is the ML estimator, θ̄̂ . Right here, the prior is implicitly handled as a relentless.

Abstract

I’ve devoted this submit to deriving the basic results of Bayesian statistics, viz. (10) . The essence of this expression is to symbolize uncertainty by combining the information obtained from two sources – observations and prior beliefs. In doing so, I launched the ideas of prior distributions, probability capabilities and posterior distributions in addition to the comparability of the frequentist and Bayesian methodologies. In my subsequent submit, I intend to make good my promise of illustrating the above instance with simulations in Python.

Bayesian statistics is a vital a part of quantitative methods that are a part of an algorithmic dealer’s handbook. The Govt Programme in Algorithmic Buying and selling (EPAT™) course by QuantInsti® covers coaching modules like Statistics & Econometrics, Monetary Computing & Know-how, and Algorithmic & Quantitative Buying and selling that equip you with the required ability units for making use of varied buying and selling devices and platforms to be a profitable dealer.

Disclaimer: All investments and buying and selling within the inventory market contain danger. Any selections to position trades within the monetary markets, together with buying and selling in inventory or choices or different monetary devices is a private determination that ought to solely be made after thorough analysis, together with a private danger and monetary evaluation and the engagement {of professional} help to the extent you imagine essential. The buying and selling methods or associated data talked about on this article is for informational functions solely.