Picture supply: Getty Photographs

Searching for one of the best low cost UK shares to purchase proper now? Listed here are two I feel deserve severe consideration proper now.

RWS Holdings

The projected rise of synthetic intelligence (AI) poses a danger to an unlimited vary of corporations. This consists of RWS Holdings (LSE:RWS), which supplies translation and localisation companies to companies across the globe.

But, whereas this disruptive menace calls for severe consideration, I feel the corporate is probably not as affected as some concern. It’s because a few of the sectors it covers — assume authorized companies, life sciences, and aerospace and defence, for example — require 100% content material accuracy all the time.

As an example, any inaccuracies in jet design documentation may compromise security, resulting in pricey errors and even catastrophic outcomes. Is it seemingly that corporations will need to entrust such tasks AI? I’m not so positive, that means companies which have specialist technical information like RWS will stay in excessive demand.

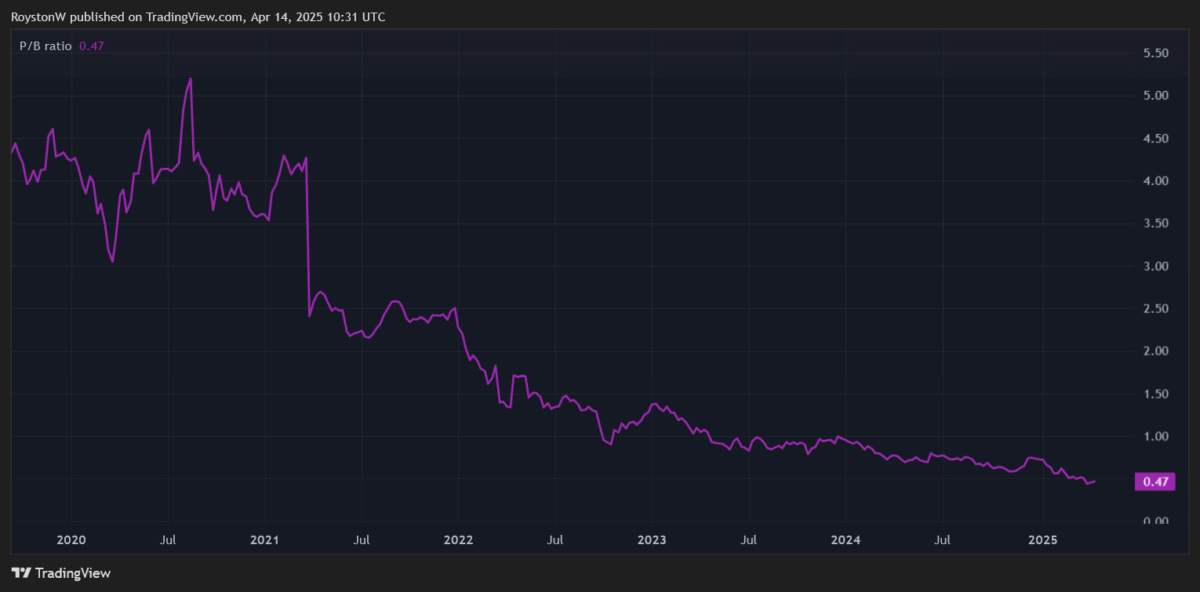

At present costs, I feel the corporate may very well be an excellent cut price share to think about. At 115p, it trades on a ahead price-to-earnings (P/E) ratio of 5.7 occasions, and its price-to-book (P/B) ratio is beneath 0.5.

Any P/B under one signifies {that a} share is affordable relative to the worth of its belongings.

Lastly, with an 11% ahead dividend yield, RWS shares have one of many highest dividend yields on the London inventory market as we speak. Money payouts right here have risen constantly since 2016.

It’s essential to notice that RWS’ sliding share worth has pumped the yield as much as present ranges. I’m optimistic that they’ll rebound, however there may very well be extra turbulence within the close to time period if worries over AI and the broader financial system develop.

The Renewables Infrastructure Group

Utilites shares like Renewables Infrastructure Group (LSE:TRIG) have been hit badly by higher-than-usual rates of interest since late 2022. And whereas charges are starting to return down, indicators of returning inflation may hamper any additional plans by central banks to loosen financial coverage.

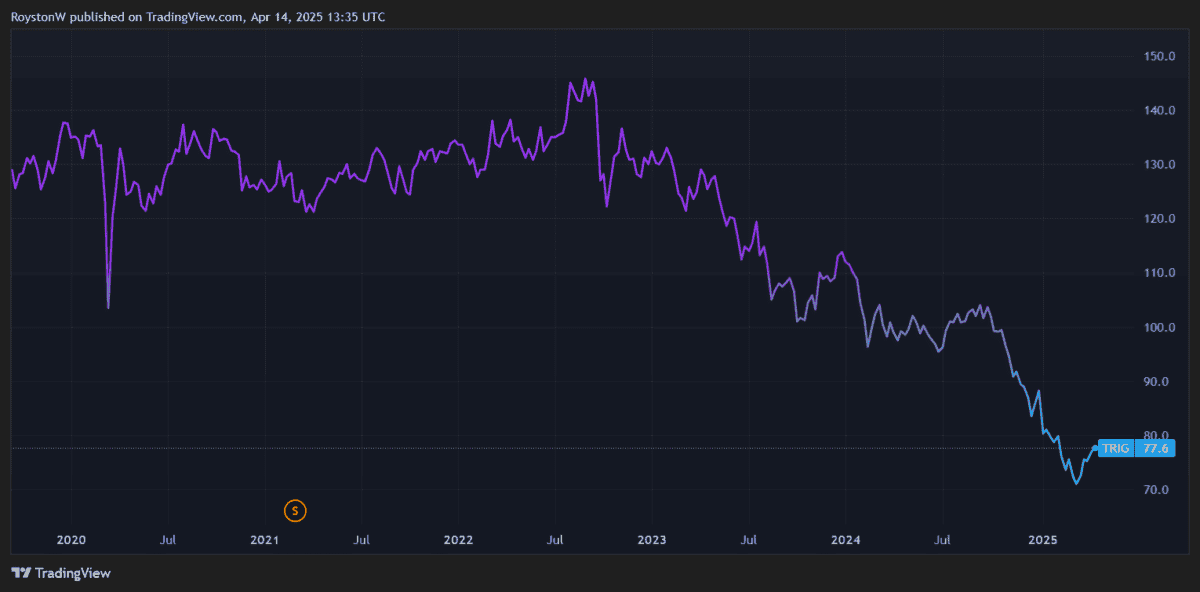

But it’s my perception that this menace to Renewables Infrastructure is greater than baked into the cheapness of its shares. In the present day, the corporate trades at 77.9p per share, which is 33.4% decrease than its estimated web asset worth (NAV) per share.

On prime of this, its ahead P/E ratio is an undemanding 9.6 occasions. And the agency’s corresponding dividend yield is a large 9.7%.

I feel excessive worth weak spot in recent times could have created a gorgeous shopping for alternative for affected person traders. Whereas the corporate could endure some near-term turbulence, I feel income may soar long term as world vitality demand will increase.

The Worldwide Vitality Company (IEA) forecasts that energy demand from knowledge centres alone will double between now and 2030, a sum equal to the whole electrical energy consumption of Japan as we speak. With international locations taking steps to cut back their fossil gasoline uptake, renewable vitality shares have appreciable earnings potential.

Renewables Infrastructure is considered one of my favorite performs on this theme. With photo voltaic, wind, and battery storage belongings protecting the breadth of Europe in its portfolio, it supplies a diversified (and subsequently decrease danger) means for traders to achieve publicity.