Picture supply: Getty Photos

Nvidia (NASDAQ: NVDA) inventory has misplaced a little bit of its shine in current months. Since peaking at $149 in early January, it has dropped 33% to simply beneath $100 (as I kind).

That mentioned, the Nvidia share value is about to open round 5% larger as we speak (23 April). The explanation? Soothing phrases round China tariffs from President Trump, who has additionally distanced himself from the notion of eradicating the US Federal Reserve chair. The entire US inventory market is able to bounce larger as we speak.

Sadly, a de-escalation within the US-China commerce struggle is unlikely to result in Nvidia being allowed to export its dumbed-down H20 AI accelerators to China. The 2 superpowers are nonetheless locked in a battle for international supremacy, with AI know-how on the forefront of that.

On 15 April, Nvidia introduced that it expects to take a cost of as much as $5.5bn on this quarter resulting from export restrictions. In mild of this, I feel it’s price looking on the newest Nvidia progress and share value targets.

Progress forecasts

Let’s begin with Q1 this yr, which is because of be reported in direction of the tip of Could. Proper now, analysts count on the semiconductor colossus to generate earnings per share (EPS) of $0.89. That’s down barely from current forecasts.

Having mentioned that, this determine would nonetheless be 46% larger than the EPS of $0.61 achieved in Q1 final yr.

By way of income, Nvidia is forecast to put up $43.1bn (65% year-on-year progress). For context, that will be roughly 51% greater than the agency’s whole 2023 monetary yr (spanning most of 2022, earlier than ChatGPT was launched).

In different phrases, Nvidia is now making considerably extra per quarter than it was making per yr simply a few years again!

Turning to the total yr, analysts at present see income surging 54% to $201bn, with EPS of $4.43 (48% progress). Then income is forecast to leap above $300bn by FY29. Hardly pedestrian!

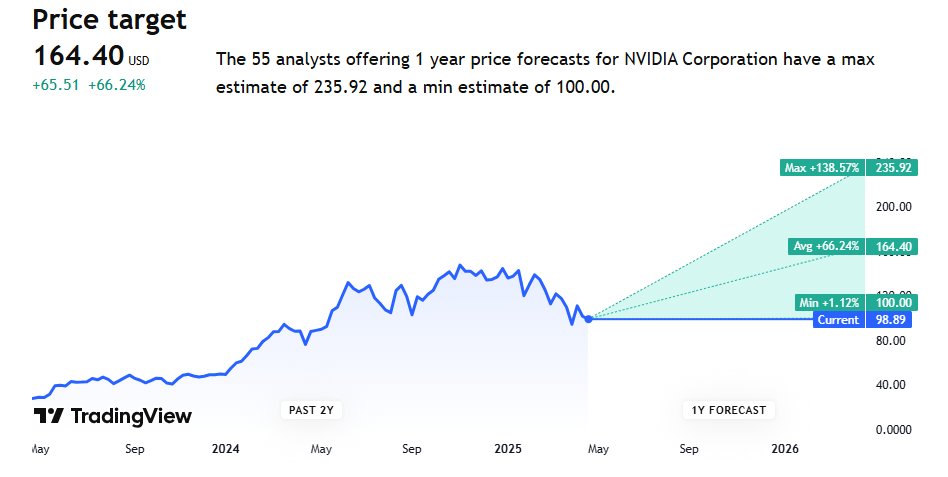

Share value goal

Do not forget that these figures are forecast even when AI-related gross sales to China are progressively being choked off. The thoughts boggles to assume how briskly Nvidia could be rising if it was free to promote its strongest AI chips to Alibaba, Tencent, Baidu, ByteDance, and the remainder.

On this situation, you would need to assume excessive double-digit progress for years on finish, in all probability placing the agency’s market cap considerably larger than its present $2.4trn.

Alas for shareholders, the Chinese language AI sector is now turning to Huawei as Nvidia exits the AI market altogether. This situation, mixed with tariffs and the danger that US tech giants might decrease their AI-related spending, has damage sentiment for Nvidia shares.

In response, many analyst groups have not too long ago been reducing their value targets. Financial institution of America Securities, for instance, has decreased its goal from $200 to $160.

The present consensus amongst Wall Road analysts is $164 — roughly 66% larger than the present degree.

Based mostly on this yr’s EPS estimate, the inventory’s forward-looking price-to-earnings (P/E) ratio is simply 23. That is forecast to fall to slightly beneath 18 by subsequent yr.

Nvidia doesn’t come with out threat, together with rising competitors and provide chain uncertainties associated to the brewing commerce struggle. However at its present valuation, I feel it’s price contemplating for long-term traders.

Q1 2025 earnings")