The 12 months 2025 is predicted to be the 12 months of IPOs. After HDB Monetary Providers, one more NBFC, Tata Capital, has secured Sebi approval for itemizing.

When well-funded teams like HDFC and Tata are looking for to leverage the bull market valuations by way of the IPOs, will others keep behind?

In the previous couple of years, a number of new-age expertise entities have gone public regardless of being loss-making on the time of their IPOs, together with Nykaa (FSN E-Commerce Ventures), Zomato, Paytm (One97 Communications) and Policybazaar (PB Fintech) initially fuelled optimism amongst traders. Nevertheless, a lot of the shares nosedived within the subsequent months.

But when the inventory markets proceed to spin a dreamy story of valuations hovering greater, 2025 may even see a repeat of 2021.

Some questions should be answered right here. Ought to traders latch on to IPOs of well-marketed new-age companies solely due to the promise of fast returns? Are they even sure of the enterprise fashions providing excessive progress in future? Or are they solely facilitating the exit of the VCs and PE traders at steep valuations?

Reality is, a few of the most understated and boring companies which have many years of earnings historical past fail to get investor curiosity in bull markets. It’s solely whenever you put the numbers in perspective and consider the protection of the enterprise mannequin that you simply realise what you might be lacking.

Living proof is the nation’s largest financial institution and a monetary juggernaut, State Financial institution of India.

The financial institution’s authorities possession, susceptibility to slippage in high quality of loans, duty of accelerating the banking protection within the nation have all put collectively stored the financial institution out of radar of progress traders.

True to expectations, the inventory of SBI has languished every now and then as a result of poor high quality of earnings progress and steadiness sheet. However over an extended time period, say many years, the financial institution has managed to greater than make-up for the misplaced years.

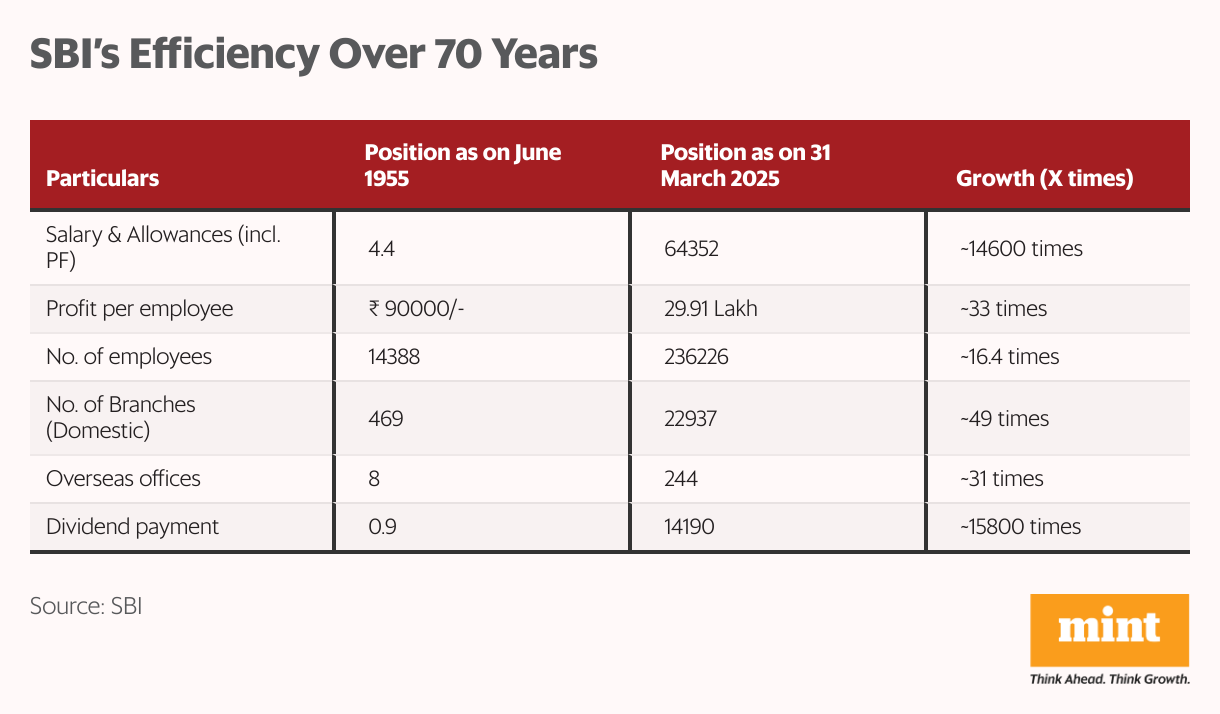

The financial institution just lately revealed some statistics of the expansion in its steadiness sheet versus the expansion in India’s GDP and the numbers are spectacular to say the least.

SBI’s earnings have grown at a staggering 52,000 instances versus the GDP progress of three,000 instances up to now seven many years.

After all, PSU banks have sometimes been low-margin, low-return-on-equity companies with excessive manpower and department operation prices.

However over time, SBI has managed to maintain a detailed watch on effectivity metrics like revenue per worker. Additionally, the financial institution has seen a pointy progress in worker prices to maintain up the expertise acquisition in new enterprise segments and compete with non-public sector friends.

The truth that the dividend paid out by the financial institution has additionally grown at a CAGR of 14.8% over the previous 70 years, reveals how the inventory has been remunerative not only for the federal government but additionally for minority shareholders.

Regardless of stiff competitors from the non-public sector and multinational banks, SBI has managed to maintain a dominant market share throughout product classes. Even within the case of technology-led choices like cell banking and UPI transactions, the financial institution has maintained its stronghold.

Being the federal government’s banker, SBI will definitely, every now and then, face the impression of coverage obligations.

Nevertheless, the financial institution will maintain a wholesome tempo of progress and profitability for a number of many years.

When such shares are buying and selling under two instances guide worth and 10 instances earnings, is there actually a have to chase IPOs at lofty valuations?

Completely happy Investing.

Disclaimer: This text is for data functions solely. It isn’t a inventory advice and shouldn’t be handled as such.

This text is syndicated from Equitymaster.com.