Skipper Ltd – Energizing the Future

Established in 1981 and headquartered in Kolkata, Skipper Ltd. is a well-established producer of Transmission and Distribution (T&D) buildings (Towers and Poles). The corporate can also be a outstanding participant within the polymer business and a dependable accomplice for executing vital infrastructure EPC initiatives. The corporate is the most important producer of transmission towers in India and ranks among the many high 10 globally. With 4 manufacturing amenities throughout India, the corporate boasts a mixed annual capability of 300,000 MTPA for engineering merchandise and 62,000 MTPA for polymer pipes and fittings. It presently serves clients in over 50 international locations worldwide.

Merchandise and Providers

The corporate’s choices may be categorized throughout 3 segments:

- Engineering – Manufacturing of T&D buildings similar to energy distribution poles, energy transmission and telecom towers, railway buildings, monopoles, MS and excessive tensile angles.

- Infrastructure – EPC initiatives specialising in stay line operations, retrofitting and energy evacuation options, coating options.

- Polymer – PVC pipes and fittings, HDPE pipes, tub equipment, tanks, borewell pipes and fittings, CPVC solvent cement, and so forth.

Subsidiaries: As of FY24, the corporate has 1 three way partnership and no different subsidiary/affiliate firm.

Funding Rationale

- Increasing order ebook – In FY25, the corporate reported its highest-ever annual order influx, exceeding Rs.5,335 crore. The year-end order ebook stood at Rs.7,458 crore, additionally a document excessive, with a well-diversified mix- 88% from home and 12% from worldwide markets. Through the 12 months, the corporate secured its first order within the U.S. market by a multi-million-dollar contract with a number one regional EPC participant. It additionally entered the EPC substation phase with a significant transmission line order. The corporate was chosen as a most popular provider and contractor by Energy Grid for larger voltage transmission initiatives and secured key orders, together with the 800 kV Khavda HVDC challenge and several other 765 kV / 400 kV initiatives.

- Progress methods – Skipper is pursuing aggressive development methods, together with a capability enlargement of 75,000 tons already underway and plans for an extra 75,000 tons within the coming 12 months, supported by a Rs.200 crore capex. Within the newest quarter, the corporate’s engineering and polymer segments achieved their highest-ever revenues, every posting 34% year-on-year development. Inside the polymer enterprise, the corporate is sharpening its deal with the plumbing phase and expects 25% – 30% development, together with improved margins. Moreover, the corporate has secured all vital approvals to enter the fuel pipeline phase utilizing MDPE (Medium-Density Polyethylene) pipes, leveraging its present HDPE (Excessive-Density Polyethylene) infrastructure as a part of its broader polymer technique.

- Q4FY25 – Through the quarter, the corporate generated its highest ever quarterly income of Rs.1,288 crore, a rise of 12% in comparison with the Rs.1,154 crore of Q4FY24. Working revenue elevated from Rs.109 crore of Q4FY24 to Rs.124 crore of Q4FY25, a development of 14%. The corporate reported internet revenue of Rs.48 crore, a rise by 90% YoY in comparison with Rs.25 crore of the corresponding interval of the earlier 12 months.

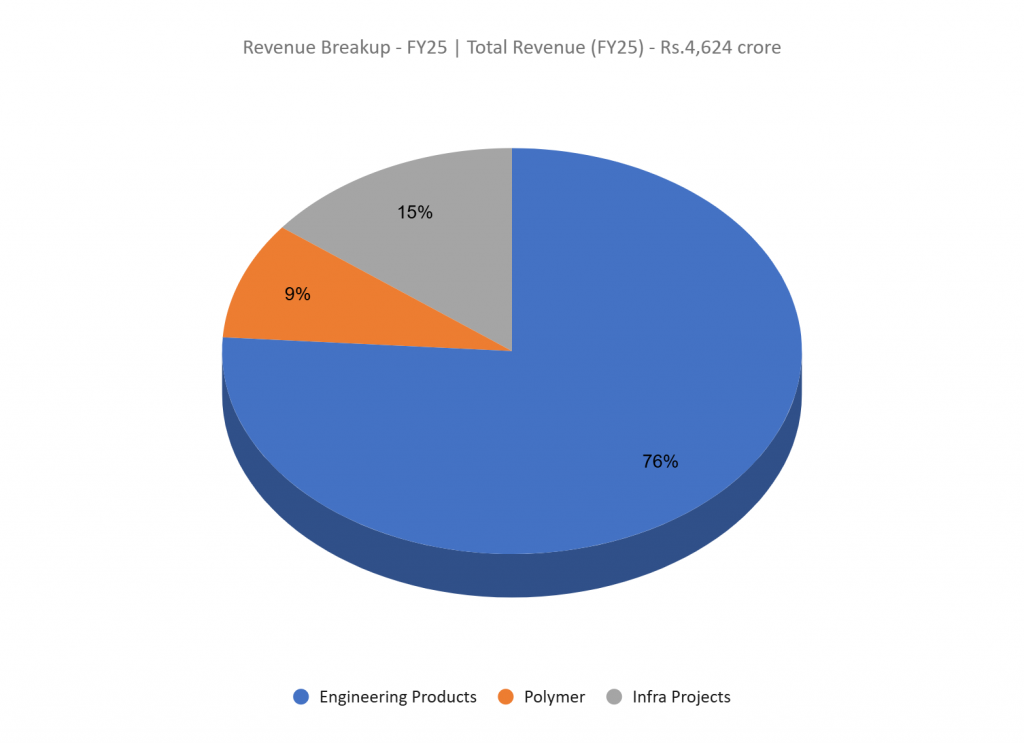

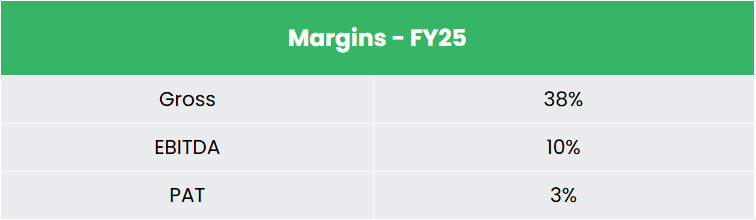

- FY25 – Through the FY, the corporate generated income of Rs.4,624 crore, a rise of 41% in comparison with the FY24 income. Export income grew by 21% through the interval. Working revenue is at Rs.452 crore, up by 41% YoY. The corporate reported internet revenue of Rs.149 crore, a rise of 82% YoY.

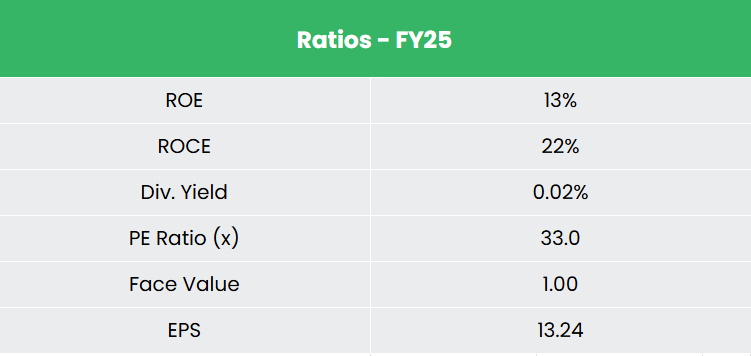

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 39% and 81% respectively between FY23-25. The corporate has a strong capital construction with a debt-to-equity ratio of 0.62. Common 3-year ROE and ROCE is round 10% and 19% for FY23-25 interval.

Business

India’s electrical gear market is predicted to develop from US$ 52.98 billion in 2022 to US$ 125 billion by 2027, registering a robust CAGR of 11.68%, pushed by rising electrification, infrastructure growth, and coverage help. The sector advantages from its shut linkages with capital items, engineering, and development industries. To satisfy rising energy demand – projected at 458 GW by 2032 – the federal government has dedicated Rs.9.15 lakh crore (US$ 109.5 billion) to improve energy infrastructure. With an put in capability of 466.24 GW as of January 2025, India is the world’s third-largest electrical energy producer and client. The deal with common entry to energy, coupled with a shift in the direction of renewables and grid modernization, creates vital long-term alternatives within the T&D area.

Progress Drivers

- Authorities initiatives, such because the PM Gati Shakti Nationwide Grasp Plan, are enjoying an important function in strengthening the capabilities of the T&D sector.

- The federal government has de-licensed the engineering sector with 100% FDI permitted.

- Rising electrical energy demand, accelerated urbanization, the combination of renewable power, ongoing grid digitalization efforts, and the alternative of growing old infrastructure throughout numerous areas are anticipated to function main development catalysts for the T&D business.

Peer Evaluation

Rivals: Elecon Engineering Firm Ltd, CG Energy & Industrial Options Ltd, and so forth.

Among the many above rivals, the corporate stands out with regular income development, steady return ratios, and wholesome earnings potential, reflecting the corporate’s monetary stability and its capability to effectively generate revenue and returns on invested capital.

Outlook

The corporate is witnessing a strong bidding pipeline with a wholesome conversion price, and administration stays assured about sturdy order inflows, which had beforehand been restricted by capability constraints. With its ongoing and deliberate capability expansions, the corporate now has clear income visibility. It’s focusing on a development price of 20–25% over the subsequent 2–3 years and has dedicated Rs.800 crore in capital expenditure over the subsequent 4 years. Moreover, Skipper is eyeing vital alternatives within the U.S. market, with a bid pipeline of round $150 million.

Valuation

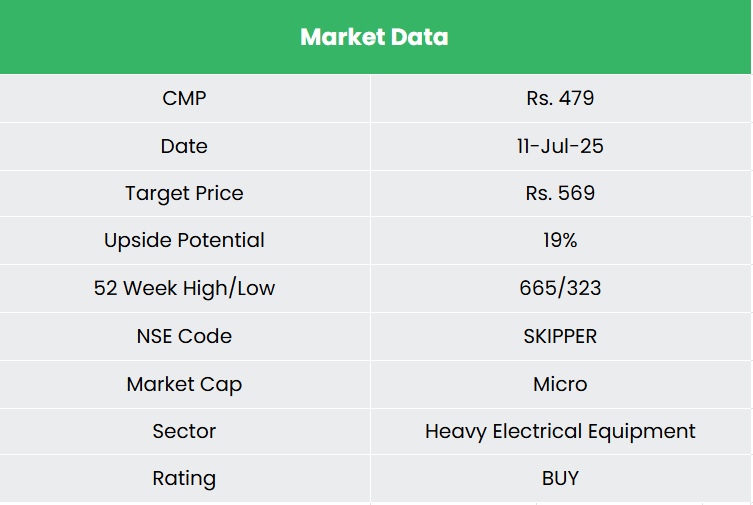

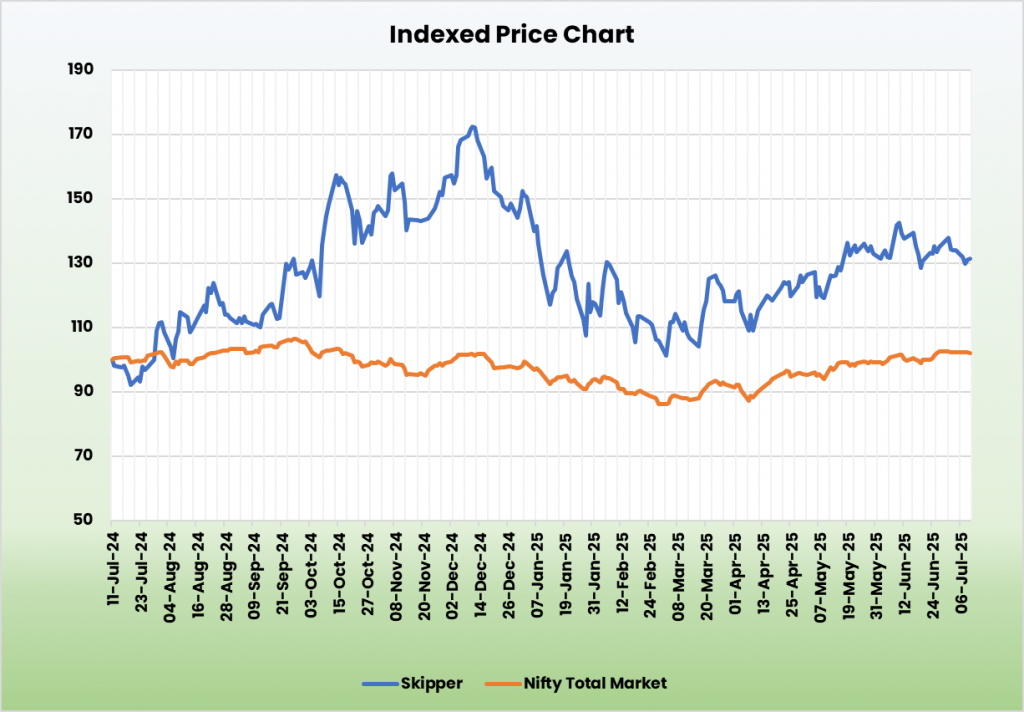

We imagine the corporate is well-positioned to maintain its development momentum, supported by a robust order pipeline and anticipated capability expansions. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.569, 41x FY27E EPS.

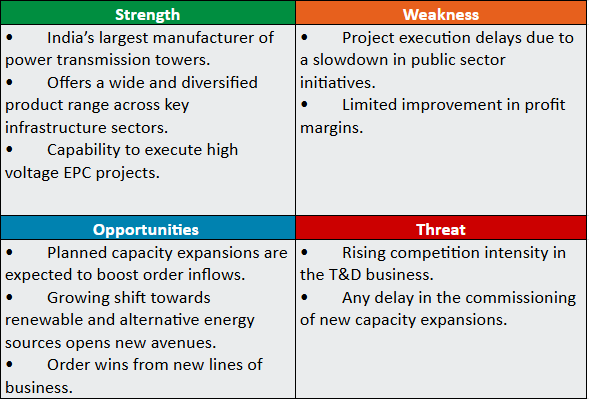

SWOT Evaluation

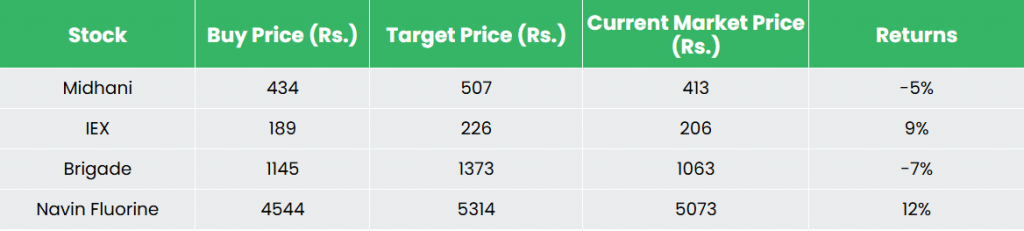

Recap of our earlier suggestions (As on 11 July 2025)

Mishra Dhatu Nigam Ltd

Indian Vitality Change Ltd

Brigade Enterprises Ltd

Navin Fluorine Worldwide Ltd

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM on no account assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Publish Views:

101