One of the anticipated IPOs of 2025, Nationwide Securities Depository Restricted (NSDL), is ready to launch its long-awaited IPO following SEBI’s approval to go public and record itself on the Indian inventory exchanges. The IPO will open from thirtieth July to 1st August.

This IPO goes to be an entire provide on the market(OFS), with as much as 5.01 crore fairness shares being provided to the general public by the administration. It’s to be famous that since NSDL is a professionally managed firm, there are not any promoters, and the funds raised via the IPO will likely be diverted to them and received’t be used for company functions.

The entities which can be going to promote an element/entire of their stake within the agency are the Nationwide Inventory Trade of India(NSE), HDFC Financial institution, SBI, IDBI Financial institution, Union Financial institution of India, and Administrator of the Specified Endeavor of the Unit Belief of India.

Concerning the enterprise, it is among the solely two depositories out there in India, alongside Central Depository Providers Restricted (CDSL), which is already listed on the inventory exchanges. So, since NDSL can be going public, it raises a priority to the general public and current shareholders of CDSL about whether or not to decide on CDSL or the newly listed agency NDSL, which might develop their funding. Let’s see what’s unveiled additional within the article.

Get full particulars in regards to the NSDL IPO—together with dates, value band, and lot dimension—on Zerodha. Keep up to date with all the newest IPO data Click on Right here

Central Depository Providers Restricted (CDSL)

Central Depository Providers Restricted (CDSL) is an Indian securities depository that permits digital holding and switch of monetary securities. It affords providers like dematerialization, commerce settlement, company motion processing, pledging, and e-voting. CDSL ensures safe, paperless, and environment friendly capital market operations for traders, brokers, and corporations.

CDSL can be a professionally managed agency like NSDL, with main shareholders consisting of BSE (15%), Life Insurance coverage Company of India, Nippon India Small Cap Fund, Parag Parikh Flexi Cap Fund, and lots of others.

It has demat custodies value Rs. 71 lakh crores, and as of Q4FY24, it derived 33.9 p.c of its earnings from annual issuer earnings, 22.65 p.c from IPO/CA earnings, 19.14 p.c from transaction costs, 14.45 p.c from on-line knowledge costs, and 9.76 p.c from different operations.

Coming to market dominance within the variety of demat accounts managed, CDSL holds a 76 p.c market share with 15+ Crore demat accounts, a powerful progress pushed primarily by retail and low cost brokers like Zerodha, Groww, and Upstox.

The administration is assured in sustaining its main place, foreseeing India’s capital market progress in addition to conserving in consideration the unpredictability of market volumes and regulatory outcomes. It cites 8x progress in demat accounts in 5 years, with sturdy revenue progress and elevated model significance, together with growth in mutual funds and the insurance coverage phase.

So we simply noticed that CDSL appears to be doing fairly properly within the depository race in opposition to NSDL, with a very good variety of demat accounts in custody with a dominant market share and diversified earnings throughout a number of segments, together with the administration outlook. Now, let’s see what NSDL has to supply that may painting itself head-to-head in opposition to its competitor and entice the general public in the direction of its IPO.

Nationwide Securities Depository Restricted (NSDL)

Nationwide Securities Depository Restricted (NSDL) is India’s first and largest central securities depository, established in 1996 and controlled by SEBI, with the nation’s paper‑based mostly securities system.

It was fashioned as a direct results of the Harshad Mehta rip-off of 1992, and its sole objective was to eradicate dangers like dangerous supply, forgery, and delays in title switch by enabling digital holding, seamless commerce settlement, automated company‑motion processing, and pledging/lending of demat belongings, thereby drastically bettering market security, velocity, and price‑effectivity.

It caters to the varied wants of the securities market in India and launched a number of extra merchandise, e-services, and ancillary value-added providers and initiatives via NSDL and its subsidiaries, NSDL Database Administration Restricted (“NDML”) and NSDL Funds Financial institution Restricted (“NPBL”), thereby rising as a key enabler for the monetary market in India.

NSDL derives recurring revenues from Annual Custody Charges charged to Issuers and Annual Charges charged to Depository Contributors and different via different providers as

- annual charges charged to issuers for international funding restrict monitoring.

- annual charges from brokers for IDeAS service,

- license charges to DPs for offering its DPM software program,

- annual charges from mutual funds in the direction of assertion downloads,

- annual charges from SEZ items in the direction of system utilization and transaction costs;

- annual charges from insurance coverage firms in relation to credit score of insurance policies, and

- annual utilization charges for technology of ITP for registration of NSR.

Earlier, NSDL, via its subsidiary NSDL e-Governance Infrastructure Ltd (now renamed Protean eGov Applied sciences Ltd), used to ship digital infrastructure providers to the federal government and controlled entities equivalent to Aadhaar E-KYC, E-Signature pan providers, id identification, and lots of others. Although it was earlier its subsidiary, Protean is now a separate entity and doesn’t contribute part of NSDL’s income, and NSE nonetheless owns a stake in it together with different skilled managers.

Comparability

Coming again to the depository race, NSDL holds a 24 p.c market share within the variety of demat accounts held in comparison with the dominant participant CDSL (76%), because of its continued enterprise with dominant brokers within the business.

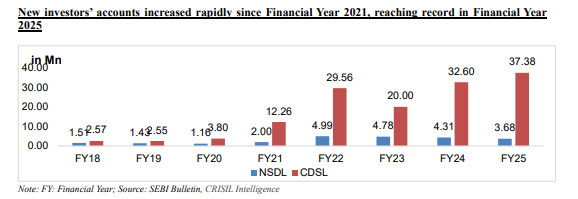

After we have a look at the development of recent investor accounts being opened, it has quickly elevated since COVID-19, when folks had sufficient time to divert their curiosity in the direction of the inventory market, which led to the Nifty rally from 8,083 ranges in April 2020 (post-COVID-19 crash) to 25,062 ranges, which grew by 210%.

As a part of the brand new traders development, the accounts opened throughout the 2 depositories grew from 1.16 Mn and three.80 Mn in FY20 to three.68 Mn and 37.38 Mn throughout NSDL and CDSL. CDSL noticed probably the most new accounts opened, which is 10X in comparison with NSDL, as CDSL works with many of the discounted brokers providing decrease costs, be it AMC, free commerce supply, and lots of extra; most turned in the direction of them, main CDSL to carry the dominant market share with the most important variety of demat accounts held.

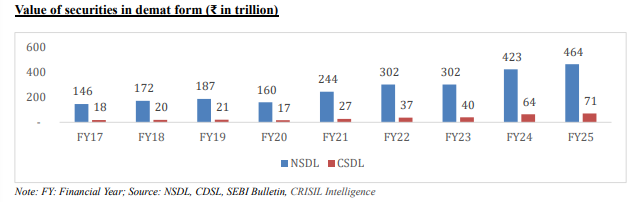

But when we evaluate it solely on the premise of a market share, we’re simply trying on the tip of an iceberg. If we have a look at the amount of securities held in demat type as of FY25, NSDL holds 4.75 Lakh Crore, which is 5.6x instances better in dimension than CDSL, which holds 83,600 Crore.

Amount of securities held in demand type (In Billion)

Following, if we have a look at the worth of securities held in demat type, CDSL holds securities value Rs. 71 trillion, whereas NDSL holds securities value Rs. 464 trillion, which is sort of 6.5x greater than the worth of securities held by CDSL.

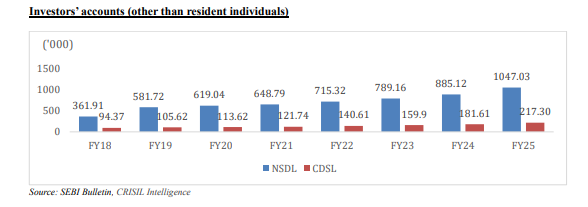

As we mentioned earlier, CDSL is the market chief contemplating the variety of demat accounts held, but when we contemplate the investor accounts held apart from the resident people, NSDL holds an even bigger chunk with a whopping 10.47 lakh accounts in comparison with 2.17 lakh accounts held by CDSL.

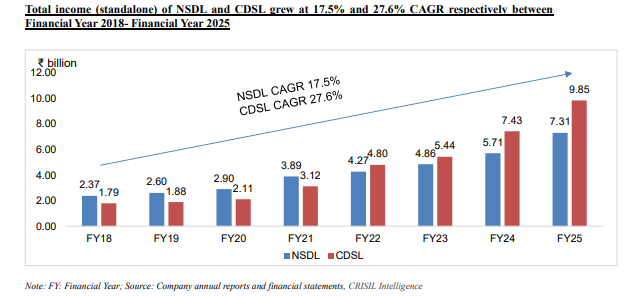

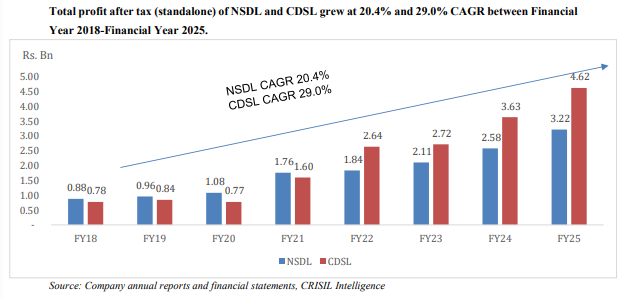

Following the monetary efficiency by going via the info out there within the RHP, the whole standalone earnings of NSDL and CDSL has grown at a CAGR of 17.5 p.c from Rs. 2.37 billion to Rs. 7.31 billion and 27.6 p.c from Rs. 1.79 billion to Rs. 9.85 billion, and coming to profitability, it has grown at a CAGR of 20.4 p.c from Rs. 0.88 billion to Rs. 3.22 billion and Rs. 0.78 billion to Rs. 4.62 billion, respectively, from FY18 to FY25, displaying higher operational effectivity by CDSL.

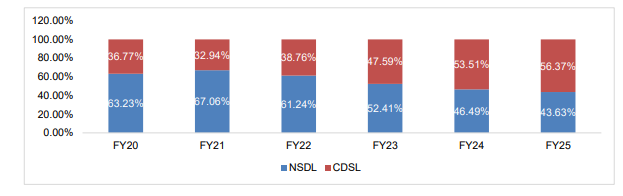

Coming to the operational entrance, as of FY25, the share of NSDL’s and CDSL’s annual costs and custody income within the depositories’ whole annual and custody costs stood at 43.63% and 56.37%, respectively. Over the interval, NSDL derived a lowering share from it from 63.23% to 43.63%, whereas CDSL elevated it from 36.77% to 56.37% over FY20-25.

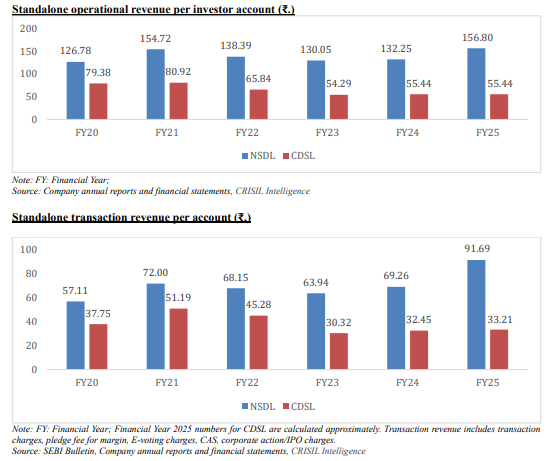

NSDL earns the next operational income per investor and transactional income per account, i.e., Rs. 156.80 and Rs. 91.69, in comparison with CDSL, which earns Rs. 55.44 and Rs. 33.21.

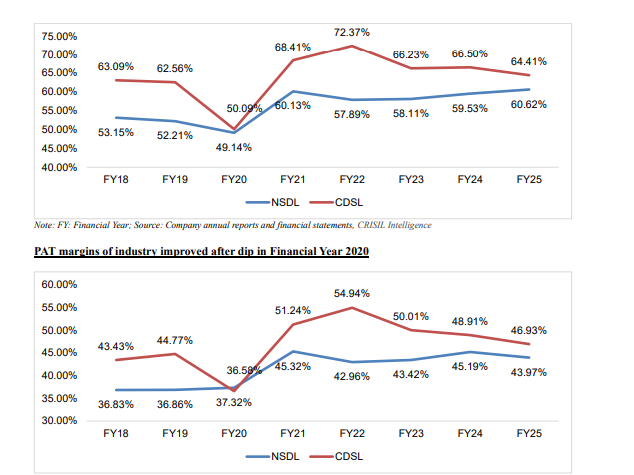

Coming to the EBITDA margins, each skilled a rollercoaster trip from a dip in FY20 (49.14%, 50.09%). CDSL derived increased margins of 72.37% in FY22 and stabilized to 64.41% in FY25, whereas NSDL stored a secure 58-61% margin vary. Following CDSL, which made peak margins of 54.94% in FY22 and made 46.93% in FY25, NSDL stored a secure 43-45% vary.

EBIDTA margins of business improved after dip in monetary yr 2020

Accordingly, trying above, each have carried out properly in a head-to-head competitors over time by bettering their operational effectivity, optimizing their prices and assets, and diversifying into completely different domains of the same nature, thereby rising and increasing their operations and profitability.

Now comes the query is which horse to wager on for the long run? Is it the already listed CDSL that dominates the market in variety of demat accounts held, diversification in enterprise, consistency in progress and margins, and continued enterprise with the well-growing low cost brokers, or NSDL, the “Darkish Horse” sitting on the peak, being the selection of massive institutional traders, holding 5.6x & 6.5x of the amount and worth of securities held by CDSL?

It could properly come right down to the way you wish to play the lengthy sport, backing CDSL’s momentum in retail quantity and razor‑sharp profitability, or NSDL’s unmatched depth in institutional belongings and sticky revenues.” So, will you wager on the confirmed retail titan or the stealthy institutional large?

Written by: Bharath Ok.S

")