Picture supply: Getty Pictures

With shelter from capital revenue and dividend taxes, the Self-Invested Private Pension (SIPP) is usually a actual sport changer for concentrating on a long-term passive revenue.

On this respect, it is similar to the Shares and Shares ISA. Nevertheless, this monetary product has an added bonus: tax reduction, which is paid on the following charges:

- 20% for basic-rate taxpayers

- 40% for higher-rate taxpayers

- 45% for additional-rate taxpayers

These tax financial savings and tax reduction give share buyers an unbelievable benefit to construct wealth. With extra capital to take a position, people can pace up the compounding course of and develop their wealth sooner over time. An added bonus is that 25% of the SIPP can finally be withdrawn freed from tax.

Please be aware that tax remedy is determined by the person circumstances of every consumer and could also be topic to alter in future. The content material on this article is supplied for data functions solely. It’s not meant to be, neither does it represent, any type of tax recommendation. Readers are liable for finishing up their very own due diligence and for acquiring skilled recommendation earlier than making any funding selections.

Put merely, this implies somebody who invests lower than £250 a month may realistically intention for a £2,000 month-to-month second revenue by the point they retire.

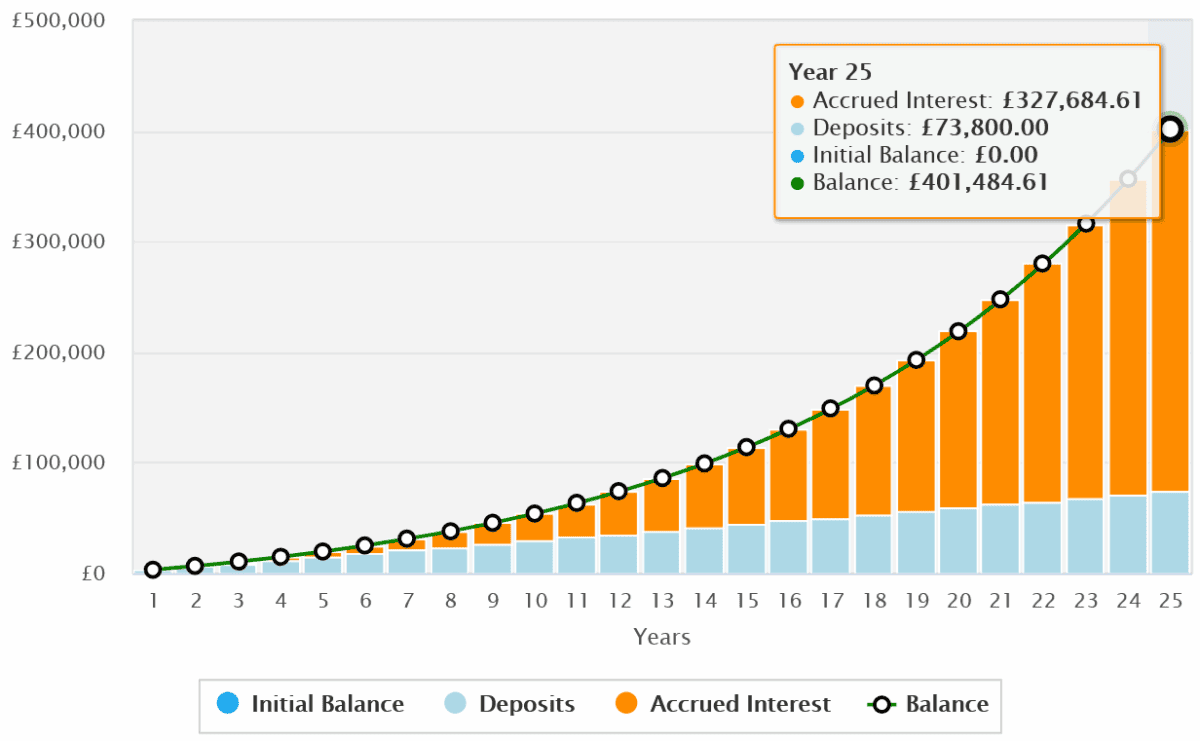

Concentrating on a £400k pension

A well-liked passive revenue technique with SIPP customers is to put money into dividend-paying shares.

An investor taking place this route would want a pension pot of £400k for an revenue of £2k a month. That’s assuming they put money into 6%-yielding dividend shares. Greater-yielding shares are generally out there that might cut back the wanted pot measurement. However these shares may be riskier as a consequence of points like sector focus, decrease development potential, and stability sheet instability.

Share buyers have many choices out there to them to focus on this £400,000 portfolio. I personally like the concept of investing in a variety of world shares, which offers large-range development and revenue alternatives. On the identical time, this diversified strategy additionally lets me unfold danger.

By holding a basket of shares that replicates the MSCI World Index, a person may goal that £400k SIPP with a month-to-month funding of slightly below £250 (£246) over 25 years. That determine consists of tax reduction, too.

This calculation is predicated on the index’s 10-year common annual return of 11.2%.

Utilizing international funds for a SIPP revenue

The MSCI World Index consists of 1,322 completely different corporations. Clearly, including this variety of shares right into a SIPP would require appreciable effort and price. Many of those shares could be unavailable to private pension buyers too. So this strategy is clearly off limits.

Fortunately, although, buyers can goal the index with the assistance of an exchange-traded fund (ETF). The iShares Core MSCI World Index (LSE:IWDG) — launched in 2017 — is one such funding car.

Monitoring errors are frequent with ETFs, reflecting small gaps between the fund’s efficiency and that of the underlying index. These mirror objects like dealing fees, commerce timings, and dividend reinvestment.

Nevertheless, well-managed funds considerably cut back (if not solely remove) the specter of extensive divergences. This iShares one has a three-year monitoring error of simply 1.42%, in response to Morningstar.

Whereas nicely diversified by sector and nation, I just like the fund’s excessive weighting of know-how shares (26.7% of the entire portfolio). Shares like Nvidia and Microsoft have important development potential because the digital economic system quickly expands.

Previous efficiency isn’t a assure of future returns. However I really feel SIPP buyers looking for a big revenue ought to severely think about international share ETFs like this one.