Picture supply: Getty Photos

Reflecting choppiness within the international financial system during the last decade, Glencore (LSE:GLEN) shares have been equally unstable as commodity costs have lurched up and down.

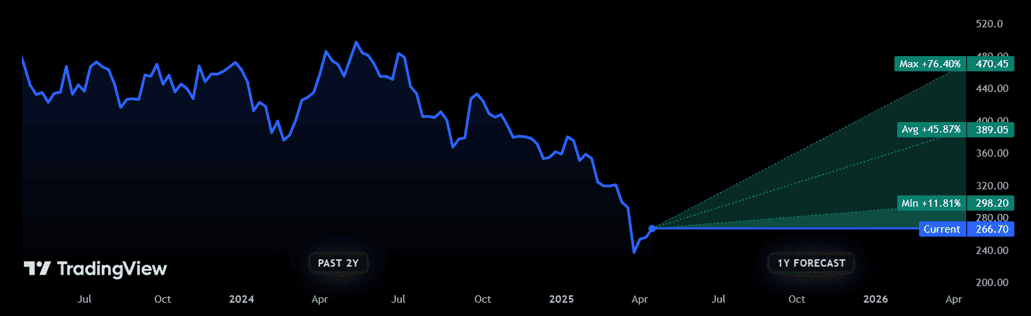

After hitting document highs of 584.5p per share in January 2023, Glencore’s share value has tumbled to present ranges of 266.7p. This more moderen collapse means somebody who parked £10,000 within the FTSE 100 firm a decade in the past, at 313.7p, would have seen the worth of their funding drop to £8,508.

But because of dividend funds totalling 124p per share over that interval, they’d have managed to eke out a optimistic return of 24.6%. For that £10k preliminary funding they’d have made a complete return of £12,459.

That’s not terrible within the context of latest macroeconomic upheavals, together with China’s financial slowdown, the worldwide pandemic and, extra lately, the worldwide introduction of latest commerce tariffs. Nevertheless, Glencore’s shares have nonetheless disenchanted in comparison with the broader Footsie (the index’s complete return is 85% over the identical interval).

However might issues be wanting up for Glencore’s share value? And may buyers think about shopping for the commodities big at this time?

Vibrant forecasts

The dangerous information is that share value forecasts for the following 10 years are unavailable. However on the plus facet, Metropolis analysts are unanimous of their perception that Glencore shares will bounce again sharply over the approaching yr.

Of the 16 brokers with rankings on the enterprise, the least optimistic believes costs will rebound near 300p over the following 12 months. That also represents a double-digit-percentage enhance. Analysts consensus is that Glencore shares will spring again to only under 390p by subsequent April. One particularly bullish forecaster has tipped costs to maneuver above 470p.

Commerce speak

Nevertheless, their capability to rebound can be compromised if thumping commerce tariffs come into impact. Newest import information from China — by far the world’s largest copper client — confirmed inbound purple metallic shipments hunch 5.2% between January and March. That is dangerous information for Glencore, which generates substantial earnings from the manufacturing and buying and selling of copper. However the story doesn’t finish right here, because the agency additionally offers in lots of different cyclical commodities together with aluminium, nickel, aluminium, oil and coal.

Encouragingly, President Trump has cooled hypothesis over a full-blown commerce battle in latest periods. Some tariffs have been delayed, and this week he mentioned charges on China would “come down considerably.” Nevertheless, buyers must be conscious that the state of affairs is fluid, and that the mere menace of commerce frictions is sufficient to considerably harm international development.

Time to purchase Glencore shares?

Some long-term buyers won’t be postpone by this instant uncertainty nonetheless. And as somebody who holds mining shares, I’m definitely upbeat concerning the sector’s outlook to 2035. Put merely, the demand outlook for a lot of industrial metals stays extraordinarily brilliant for the following decade. That is because of the spectrum of structural alternatives that Glencore has an opportunity to capitalise on.

The expansion of renewable vitality, as an example, is tipped to supercharge consumption of copper, aluminium, nickel and iron ore. Different phenomena like rising market urbanisation, the booming digital financial system, and resurgent defence spending all bode effectively for metals demand.

In the present day, Glencore shares commerce on a ahead price-to-earnings (P/E) ratio of 13.2 occasions. At this degree, I believe the FTSE 100 miner is price a severe look.