Be a part of Our Telegram channel to remain updated on breaking information protection

US banks are urging Congress to shut a stablecoin yield “loophole” that they warn might drain as much as $6.6 trillion in deposits from the standard banking system, probably destabilizing credit score flows to American companies and households.

The Financial institution Coverage Institute (BPI), in addition to the American Bankers Affiliation, Shopper Bankers Affiliation, the Monetary Providers Discussion board, and the Impartial Neighborhood Banks of America all voiced their considerations in a letter to Congress yesterday.

They expressed considerations in regards to the present wording within the Guiding and Establishing Nationwide Innovation for US Stablecoins (GENIUS) Act. Signed into regulation on July 18, 2025, the Act establishes guidelines and laws for stablecoin issuers to comply with.

The GENIUS Act is among the many most transformative legal guidelines in a long time.@Jerallaire, with @RichardQuest on @CNN, explains what this implies for stablecoins. pic.twitter.com/BMLiwJix3Q

— Circle (@circle) July 23, 2025

Amongst these guidelines is the prohibition on stablecoin issuers that stops them from providing curiosity or yield on to holders. Based on the BIP, nonetheless, the Act doesn’t explicitly prolong the ban to crypto exchanges or affiliated companies.

Within the letter, the BIP warned that ”with out an specific prohibition making use of to exchanges, which act as a distribution channel for stablecoin issuers or enterprise associates, the necessities within the GENIUS Act will be simply evaded and undermined by permitting cost of curiosity not directly to holders of stablecoins.”

“The end result will probably be higher deposit flight danger, particularly in instances of stress,” which the BIP says may have a adverse impression on credit score creation “all through the economic system” and set off $6.6 trillion in deposit outflows from the standard banking system.

The results of that taking place will probably be “increased rates of interest, fewer loans, and elevated prices for Essential Avenue companies and households,” the banking group stated.

Stablecoins Are Essentially Totally different From Conventional Yield-Bearing Merchandise

The banking group stated that stablecoins are basically totally different from financial institution deposits and cash market funds as a result of they don’t fund loans or spend money on securities to provide holders yields.

As an alternative, stablecoin issuers corresponding to Tether (issuer of USDT) and Circle (issuer of USDC) generate and move on returns in a number of methods to holders by way of third social gathering platforms.

Each of these corporations maintain the identical quantity of reserves in fiat, of their case the US greenback, as the quantity of their tokens which can be in circulation to make sure their blockchain-based tokens preserve a 1:1 peg to the dollar.

These reserves are largely in short-term, curiosity bearing belongings corresponding to US Treasuries, which the issuers then pay the curiosity from to holders.

Nevertheless, due to the GENIUS Act’s prohibition, issuers are usually not allowed to immediately distribute the curiosity to holders. To get round this, issuers like Tether and Circle enter into revenue-sharing agreements with third events or flip to lending and custodial platforms like BlockFi and Gemini.

For instance, Coinbase at the moment provides a 4.1% yield to anybody who holds USDC on its platform.

There are additionally yield-bearing stablecoins corresponding to OUSD and sDAI that mechanically embed returns from DeFi lending, real-world asset yields or implement different methods immediately into the token. Nevertheless, these stablecoins have a tendency to return with increased ranges of danger when in comparison with USDT and USDC, primarily sensible contract, market and liquidity dangers.

These distinctions, stated the BIP, “are why cost stablecoins shouldn’t pay curiosity the way in which extremely regulated and supervised banks do on deposits or supply yield as cash market funds do.”

Stablecoin Market A Small Share Of US Cash Provide

The GENIUS Act’s signing final month was celebrated as a significant milestone and watershed second for the crypto area. Many noticed its passing and subsequent signing as step one in the direction of US regulators providing the business some long-awaited authorized readability.

Its signing additionally comes as US President Donald Trump and federal companies push to make the US the crypto capital of the world.

Inside the first week of the GENIUS Act being signed, the market capitalization for stablecoins jumped $4 billion to $264 billion, in accordance to knowledge from DefiLlama.

Stablecoin market cap (Supply: DefiLlama)

Prior to now week, the mixed valuation of stablecoins in circulation has risen greater than 1%, round $2.76 billion to face at about $271.37 billion as of 6:23 a.m. EST.

That development is predicted to proceed within the coming years. In an April 30 report, the US Treasury predicted that the stablecoin market might attain round $2 trillion by 2028.

On Aug. 8, the S&P International Scores made historical past and assigned a “B” credit standing to stablecoin protocol, Sky Protocol. The platform operates the DAI and USDS stablecoins.

Regardless of the rising capitalization and recognition of stablecoins, the sector nonetheless makes up a fraction of the US cash provide. As of the top of June, the US Federal Reserve (Fed) reported that the US cash provide stood at $22 trillion.

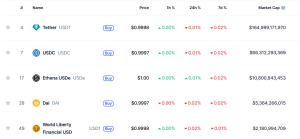

Tether’s USDT stays the most important stablecoin by market cap by a cushty margin. CoinMarketCap knowledge places its valuation at $164.99 billion.

Prime stablecoins by market cap (Supply: CoinMarketCap)

USDC, which is backed by the New York Inventory Alternate (NYSE)-listed agency Circle, is the second largest stablecoin available in the market with its capitalization standing at over $66.31 billion.

Associated Articles:

Greatest Pockets – Diversify Your Crypto Portfolio

- Simple to Use, Characteristic-Pushed Crypto Pockets

- Get Early Entry to Upcoming Token ICOs

- Multi-Chain, Multi-Pockets, Non-Custodial

- Now On App Retailer, Google Play

- Stake To Earn Native Token $BEST

- 250,000+ Month-to-month Energetic Customers

Be a part of Our Telegram channel to remain updated on breaking information protection

Hi!

stockwaves.in, Thanks for the time and heart you put into posting and moderating.

I recently published my ebooks and training videos on

https://www.hotelreceptionisttraining.com/

They feel like a rare find for anyone interested in hospitality management studies. These ebooks and videos have already been welcomed and found very useful by students in Russia, the USA, France, the UK, Australia, Spain, and Vietnam—helping learners and professionals strengthen their real hotel reception skills. I believe visitors and readers here might also find them practical and inspiring.

Unlike many resources that stay only on theory, this ebook and training video set is closely connected to today’s hotel business. It comes with full step-by-step training videos that guide learners through real front desk guest service situations—showing exactly how to welcome, assist, and serve hotel guests in a professional way. That’s what makes these materials special: they combine academic knowledge with real practice.

With respect to the owners of stockwaves.in who keep this platform alive, I kindly ask to share this small contribution. For readers and visitors, these skills and interview tips can truly help anyone interested in becoming a hotel receptionist prepare with confidence and secure a good job at hotels and resorts worldwide. If found suitable, I’d be grateful for it to remain here so it can reach those who need it.

Why These Ebooks and Training Videos Are Special

They uniquely combine academic pathways such as a bachelor’s degree in hospitality management or a advanced hotel management course with very practical guidance on the front desk agent description. They also cover the hotel front desk job description, and detailed hotel front desk tasks.

The materials go further by explaining the reservation systems in hotels, check-in and check-out procedures, guest service handling, and practical guest service recovery—covering nearly every situation that arises in the daily business of hotel reception.

Beyond theory, my ebooks and training videos connect the academic side of hospitality management studies with the real-life practice of hotel front desk duties and responsibilities.

– For students and readers: they bridge classroom study with career preparation, showing how hotel and management course theory link directly to front desk skills.

– For professionals and community visitors: they support career growth through questions for receptionist, with step-by-step questions to ask a receptionist in an interview. There’s also guidance on writing a strong receptionist description for resume.

As someone who has taught hospitality management programs for nearly 30 years, I rarely see materials that balance the academic foundation with the day-to-day job description of front desk receptionist in hotel so effectively. This training not only teaches but also simulates real hotel reception challenges—making it as close to on-the-job learning as possible, while still providing structured guidance.

I hope the owners of stockwaves.in, and the readers/visitors of stockwaves.in, will support my ebooks and training videos so more people can access the information and gain the essential skills needed to become a professional hotel receptionist in any hotel or resort worldwide.

Either way, thank you, stockwaves.in, for maintaining such a respectful space online.

Hi!

stockwaves.in, It’s clear you put real effort into your site—thank you.

I recently published my ebooks and training videos on

https://www.hotelreceptionisttraining.com/

They feel like a hidden gem for anyone interested in hospitality management and tourism. These ebooks and videos have already been welcomed and found very useful by students in Russia, the USA, France, the UK, Australia, Spain, and Vietnam—helping learners and professionals strengthen their real hotel reception skills. I believe visitors and readers here might also find them practical and inspiring.

Unlike many resources that stay only on theory, this ebook and training video set is closely connected to today’s hotel business. It comes with full step-by-step training videos that guide learners through real front desk guest service situations—showing exactly how to welcome, assist, and serve hotel guests in a professional way. That’s what makes these materials special: they combine academic knowledge with real practice.

With respect to the owners of stockwaves.in who keep this platform alive, I kindly ask to share this small contribution. For readers and visitors, these skills and interview tips can truly help anyone interested in becoming a hotel receptionist prepare with confidence and secure a good job at hotels and resorts worldwide. If found suitable, I’d be grateful for it to remain here so it can reach those who need it.

Why These Ebooks and Training Videos Are Special

They uniquely combine academic pathways such as a bachelor of hospitality management or a advanced hotel management course with very practical guidance on the duties of a front desk agent. They also cover the hotel front desk receptionist job description, and detailed hotel front desk tasks.

The materials go further by explaining the hotel reservation process, check-in and check-out procedures, guest relations, and practical guest service recovery—covering nearly every situation that arises in the daily business of hotel reception.

Beyond theory, my ebooks and training videos connect the academic side of resort management with the real-life practice of hotel front desk duties.

– For students and readers: they bridge classroom study with career preparation, showing how hotel and management course theory link directly to front desk skills.

– For professionals and community visitors: they support career growth through questions for receptionist, with step-by-step interview questions for receptionist with answers. There’s also guidance on writing a strong receptionist job description for resume.

As someone who has taught resort management for nearly 30 years, I rarely see materials that balance the academic foundation with the day-to-day hotel front desk job responsibilities so effectively. This training not only teaches but also simulates real hotel reception challenges—making it as close to on-the-job learning as possible, while still providing structured guidance.

I hope the owners of stockwaves.in, and the readers/visitors of stockwaves.in, will support my ebooks and training videos so more people can access the information and gain the essential skills needed to become a professional hotel receptionist in any hotel or resort worldwide.

Keep up the great work—your consistency matters.

Hello, friend!

stockwaves.in, Your consistency and kindness in this space don’t go unnoticed.

I recently published my ebooks and training videos on

https://www.hotelreceptionisttraining.com/

They feel like a rare find for anyone interested in hotel and management. These ebooks and videos have already been welcomed and found very useful by students in Russia, the USA, France, the UK, Australia, Spain, and Vietnam—helping learners and professionals strengthen their real hotel reception skills. I believe visitors and readers here might also find them practical and inspiring.

Unlike many resources that stay only on theory, this ebook and training video set is closely connected to today’s hotel business. It comes with full step-by-step training videos that guide learners through real front desk guest service situations—showing exactly how to welcome, assist, and serve hotel guests in a professional way. That’s what makes these materials special: they combine academic knowledge with real practice.

With respect to the owners of stockwaves.in who keep this platform alive, I kindly ask to share this small contribution. For readers and visitors, these skills and interview tips can truly help anyone interested in becoming a hotel receptionist prepare with confidence and secure a good job at hotels and resorts worldwide. If found suitable, I’d be grateful for it to remain here so it can reach those who need it.

Why These Ebooks and Training Videos Are Special

They uniquely combine academic pathways such as a bachelor of hospitality management or a advanced hotel management course with very practical guidance on the hotel front desk job duties. They also cover the hotel front desk job description, and detailed hotel front desk duties and responsibilities.

The materials go further by explaining the reservation systems in hotels, check-in and check-out procedures, guest service handling, and dealing with guest complaints—covering nearly every situation that arises in the daily business of a front office operation.

Beyond theory, my ebooks and training videos connect the academic side of hospitality management studies with the real-life practice of hotel front desk duties and responsibilities.

– For students and readers: they bridge classroom study with career preparation, showing how hotel management certificate programs link directly to front desk skills.

– For professionals and community visitors: they support career growth through questions for receptionist, with step-by-step questions to ask a receptionist in an interview. There’s also guidance on writing a strong receptionist job description for resume.

As someone who has taught resort management for nearly 30 years, I rarely see materials that balance the academic foundation with the day-to-day job description of front desk receptionist in hotel so effectively. This training not only teaches but also simulates real hotel reception challenges—making it as close to on-the-job learning as possible, while still providing structured guidance.

I hope the owners of stockwaves.in, and the readers/visitors of stockwaves.in, will support my ebooks and training videos so more people can access the information and gain the essential skills needed to become a professional hotel receptionist in any hotel or resort worldwide.

Thanks again for all the work you do here.

This was a great read—thanks for sharing!

Just thought I’d drop in that could be useful to anyone in the hospitality and tourism space. We recently launched a super easy-to-use smart tourism chatbot designed especially for hospitality businesses looking to boost bookings, guest satisfaction, and 24/7 support—on autopilot.

It’s a lightweight HTML chatbot code that installs in minutes—no tech skills needed. This hospitality chatbot runs all day and night to answer FAQs, even connecting with WhatsApp.

See full details and live demo here:

https://chatbotforleads.blogspot.com/2025/04/boost-bookings-and-guest-satisfaction.html

But here’s the best part: besides hotel and tourism, we also offer a full range of chatbot solutions that work beautifully on any website, in any industry, to drive sales in a simple, smart, and wonderful way—only $69 lifetime. No subscriptions. No tech headaches.

Use it as a customer support assistant—and test it out instantly on our blog.

With nearly 30 years of experience in hospitality, we built this tool to be one of the most practical options available for small businesses.

So if you’re ready to engage more guests, or just want a chatbot that works—we’d love for you to check it out.

Hope it helps!

Greetings stockwaves.in,

You’re providing high-quality content for your readers.

We support website owners and bloggers to get genuine, niche-specific traffic and convert visitors into potential clients. Using the same method that reached you — posting focused blog comments and contact form messages in your niche and location — our chatbot engages these visitors automatically to capture leads efficiently.

As a special offer, if you purchase our chatbot service (normally $69, now $49), simply tell us your website, and we will manage the comment and contact form service for you. We’ll create 1,000 targeted comments or submissions to bring visitors interested in your niche and location — worldwide.

We provide chatbots for many niches: all-purpose bots, real estate, dental, education, hotels & tourism, bars, cafés, automotive, and more.

See the full system here: https://chatbotforleads.blogspot.com/ — it shows precisely how the traffic and lead generation works in action.

Many thanks for taking a moment to read this, and Hope this can bring some value to your audience and business.

Hey stockwaves.in,

You’re providing very useful content for your readers.

We support website owners and bloggers to get genuine, niche-specific traffic and convert visitors into potential clients. Using the same method that reached you — posting focused blog comments and contact form messages in your niche and location — our chatbot engages these visitors automatically to capture leads efficiently.

As a special offer, if you purchase our chatbot service (normally $69, now $49), simply tell us your website, and we will manage the comment and contact form service for you. We’ll create 1000 custom comments and messages to bring visitors interested in your niche and location — worldwide.

We provide chatbots for many niches: all-purpose bots, real estate, dental, education, hotels & tourism, bars, cafés, automotive, and more.

See the full system here: https://chatbotforleads.blogspot.com/ — it shows clearly how the traffic and lead generation works in action.

Appreciate your attention, and Wishing you more engagement and growth with your content.

Hi there stockwaves.in,

You’re providing such valuable content for your readers.

We support website owners and bloggers to get qualified traffic and convert visitors into potential clients. Using the same method that reached you — posting focused blog comments and contact form messages in your niche and location — our chatbot engages these visitors automatically to capture leads efficiently.

As a special offer, if you purchase our chatbot service (normally $69, now $49), simply tell us your website, and we will handle the comment and contact form service for you. We’ll create a thousand niche-specific entries to bring visitors interested in your niche and location — by country or even by city.

We provide chatbots for many niches: all-purpose bots, real estate, dental, education, hotels & tourism, bars, cafés, automotive, and more.

See the full system here: https://chatbotforleads.blogspot.com/ — it shows exactly how the traffic and lead generation works in action.

Appreciate your attention, and Wishing you and your website continued success.