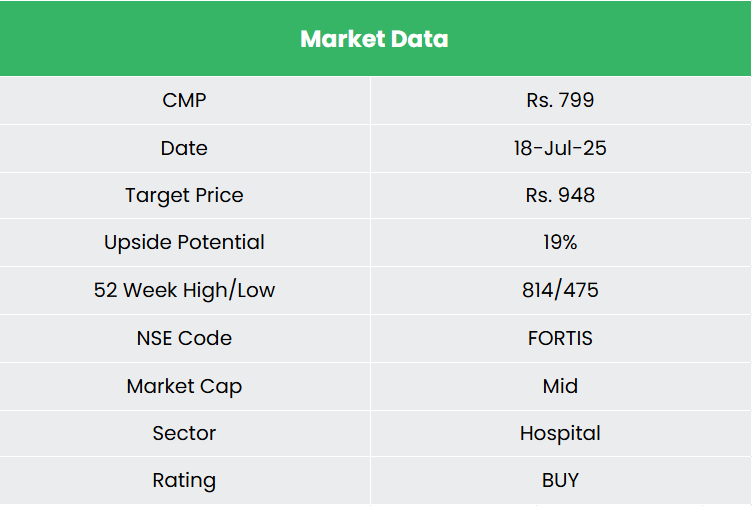

Fortis Healthcare Ltd – Reworking lives, Rising Collectively

Included in 1996 and headquartered in Gurugram, Fortis Healthcare Ltd. is among the largest healthcare companies suppliers in India. The corporate gives a large spectrum of built-in healthcare amenities comprising of hospitals, diagnostics and day care specialty hospitals. As of 31 March 2025, the corporate has a community of 27 hospitals throughout 10 cities, 7,500+ medical doctors, 7,500+ nurses, ~4,750 operational beds. Moreover, the corporate operates its community of diagnostics companies – Agilus Diagnostics Ltd with over 400 labs and 4,100+ buyer touchpoints and a rising presence throughout 1,000+ cities and cities. Along with India, the corporate additionally has presence in UAE, Nepal and Sri Lanka.

Merchandise and Companies

The corporate’s companies might be categorised into two segments:

- Healthcare consists of inpatient and outpatient companies, sale of medical and non-medical gadgets and administration charges from hospital.

- Diagnostics embrace pathology and radiology companies.

Subsidiaries: As of FY25, the corporate has 29 subsidiaries and a couple of associates and joint ventures every.

Funding Rationale

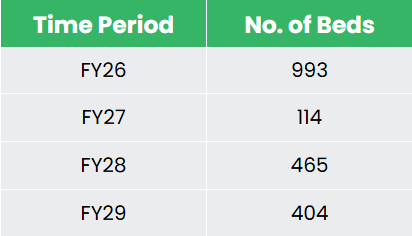

- Growth plans – Fortis has set out aggressive growth technique, aiming so as to add roughly 2,000 beds between FY26 and FY29 via a mixture of acquisitions, brownfield developments, and greenfield tasks. The corporate has acquired complete operations (underlying hospital and adjoining land) of Shrimann Superspecialty Hospital, Jalandhar, one of many main multi-specialty hospitals within the area, which reported income of Rs.138 crore in FY24. This acquisition has added 228 beds to the corporate’s portfolio, with potential to additional develop capability by over 180 beds via the event of a brand new facility on the adjoining land. Throughout FY25, Fortis commissioned its newly constructed 350-bed hospital in Manesar, beginning operations with an preliminary capability of 90 beds. The power, at the moment working at 40% occupancy, has achieved an ARPOB of Rs.2.67 crore. The corporate plans so as to add one other 120 beds and targets an occupancy fee of fifty% by FY26. Inside its diagnostics arm, it’s upgrading its infrastructure via the commissioning of superior medical gear. A brand new genomics lab has been launched in Gurgaon, alongside a transplant immunology lab in Bangalore, additional strengthening its capabilities in specialised diagnostics The under desk offers further capability growth plans at the moment introduced by the corporate:

- Operational Efficiency – The corporate delivered sturdy operational efficiency in FY25, underpinned by improved hospital metrics, rising procedural volumes, and development throughout key specialties and geographies. General hospital occupancy improved to 69% from 65% YoY, reflecting increased affected person volumes and improved capability utilization. The Common Income Per Occupied Mattress (ARPOB) elevated to Rs.2.42 crore p.a. from Rs.2.22 crore p.a., pushed by increased case complexity and elevated contribution from high-yield specialties. Key scientific segments – together with oncology, neurosciences, cardiac sciences, gastroenterology, orthopaedics, and renal sciences – grew by 16% YoY, collectively contributing 62% to the whole hospital income. The Common Size of Keep (ALOS) improved from 4.28 days to 4.19 days, indicating operational effectivity and higher case administration. Income from digital channels registered a strong development of 35% and worldwide affected person revenues rose 13% YoY to Rs.539 crore. When it comes to procedural volumes, the corporate reported a major 72% YoY development in robotic surgical procedures and a 17% improve in neuro and backbone procedures, highlighting rising demand for superior surgical care.

- Q4FY25 – Throughout the quarter, the corporate generated income of Rs.2,007 crore, reaching a rise of 12% as in comparison with the Rs.1,786 crore of Q4FY24. EBITDA improved by 14% YoY, from Rs.435 crore to Rs.380 crore. Web revenue stood at Rs.188 crore, a de-growth of seven% from Rs.203 crore of Q4FY24.

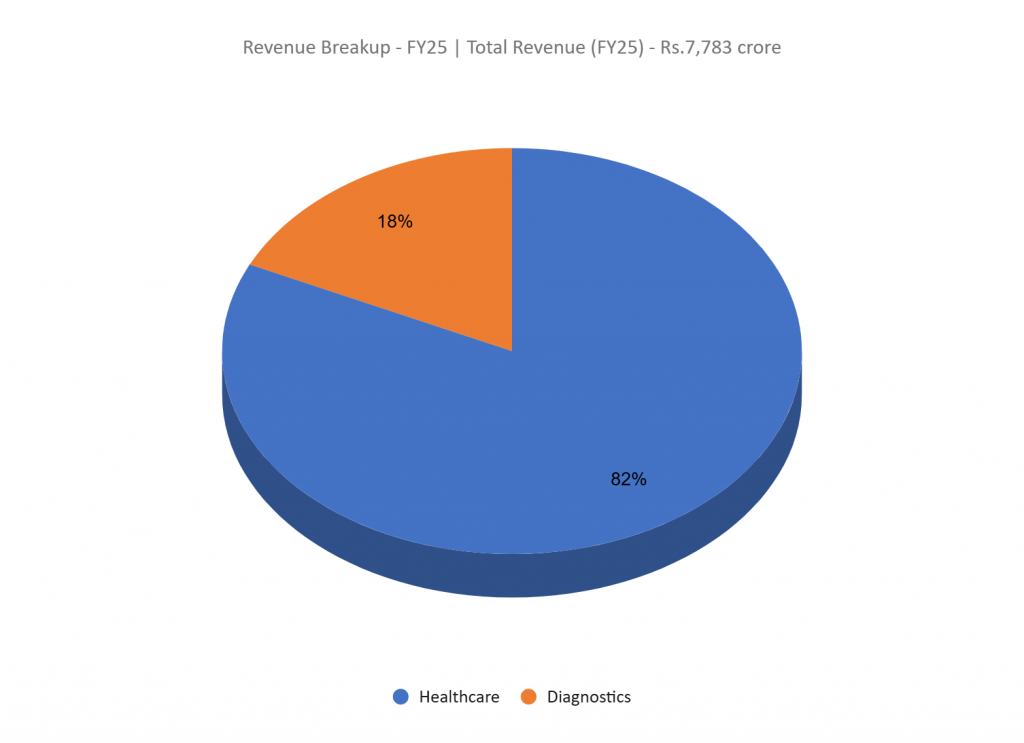

- FY25 – The corporate generated income of Rs.7,783 crore, a rise of 13% in comparison with FY24 income. The expansion was primarily pushed by ~15% development in hospital enterprise income which contributes 84% to the corporate’s income. EBITDA is at Rs.1,655 crore, up by 27% YoY. The corporate posted a web revenue of Rs.809 crore, a development of 25% YoY. EBITDA margin has improved from 19% to 21% and web revenue margin improved from 9% to 10%. Hospital enterprise has improved its EBITDA margin from 19% to 21% and diagnostics arm EBITDA margin from 17% to twenty%.

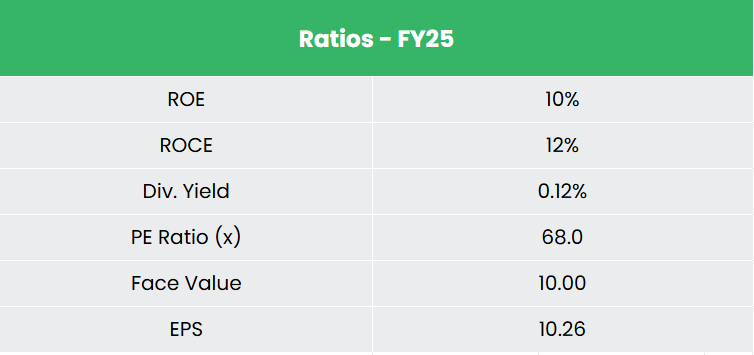

- Monetary Efficiency – The income and web revenue CAGR of the corporate for the previous 3 years is round 11% and 31% between FY23-FY25. The three-year common ROE and ROCE for the corporate is round 9% and 11% for the previous 3 years. The corporate has a wholesome capital construction with a debt-to-equity ratio of 0.28.

Business

India’s healthcare sector has emerged as one of many nation’s largest industries, each by way of income era and employment. In 2023, the hospital market was valued at US$ 98.98 billion and is anticipated to develop at a compound annual development fee (CAGR) of 8.0% from 2024 to 2032, reaching roughly US$ 193.59 billion by 2032. The nation has additionally positioned itself as a number one hub for superior diagnostic companies, supported by vital capital investments. India can also be a cheap possibility in comparison with different international locations in Asia and the West, making it a pretty vacation spot for worldwide sufferers and contributing to the rise of medical tourism.

Development Drivers

- Authorities allocation of Rs.99,858 crore (US$ 11.50 billion) to the healthcare sector within the Union Finances 2025-26, a 9.78% improve in comparison with the earlier 12 months.

- 100% FDI allowed below computerized route within the hospital sector.

- Rising revenue ranges, ageing inhabitants, rising well being consciousness and larger penetration of medical insurance.

Peer Evaluation

Opponents: Aster DM Healthcare Ltd, International Well being Ltd and so forth.

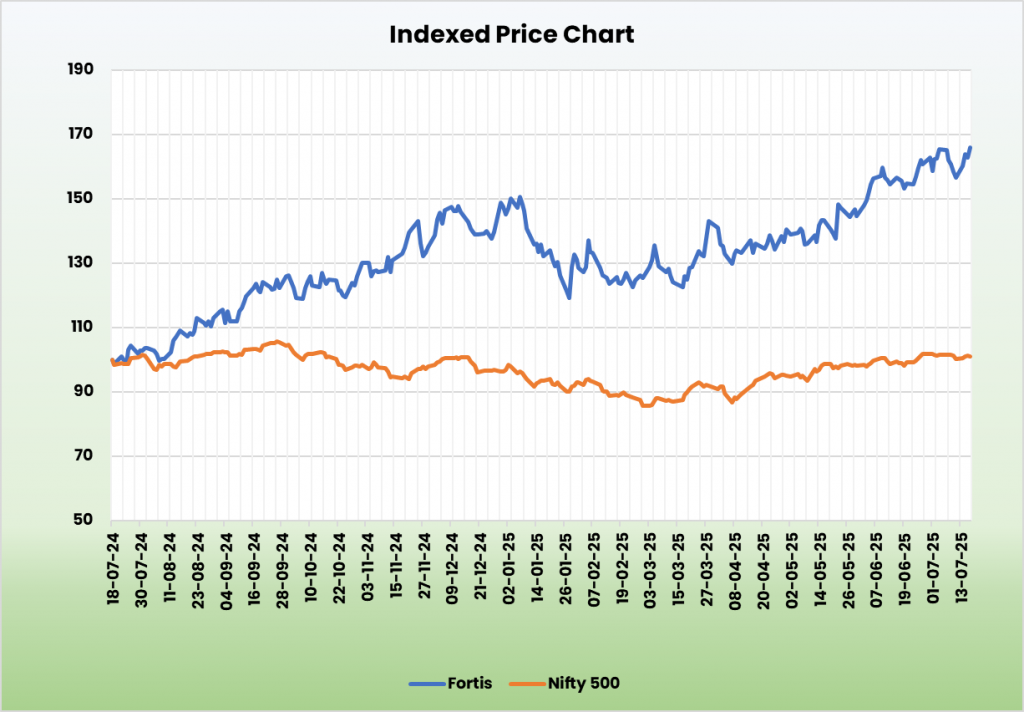

We consider the corporate is pretty valued relative to its friends, supported by sturdy fundamentals, strong income development, constant returns on invested capital, and steady working margins that replicate disciplined price administration and operational effectivity.

Outlook

For FY26, the corporate has offered income development steerage of 14–15%, with 5–6% anticipated to come back from increased ARPOB, and the rest pushed by elevated affected person volumes. The hospital enterprise is anticipated to realize an EBITDA margin of 20.5%, whereas the diagnostics phase is guided to ship margins within the vary of 21% to 22%. Over the medium time period, the corporate is focusing on EBITDA margins of 25%. On the growth entrance, Fortis continues to scale via brownfield tasks. In Punjab, the corporate plans to double its present mattress capability from roughly 800 to 1,600 beds within the subsequent 2–3 years, supported by ongoing and deliberate brownfield developments in key cities akin to Amritsar and Mohali.

Valuation

We consider the corporate is nicely positioned to capitalise on the rising healthcare demand, supported by constant mattress additions and operational efficiencies. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.948, 64x FY27E EPS.

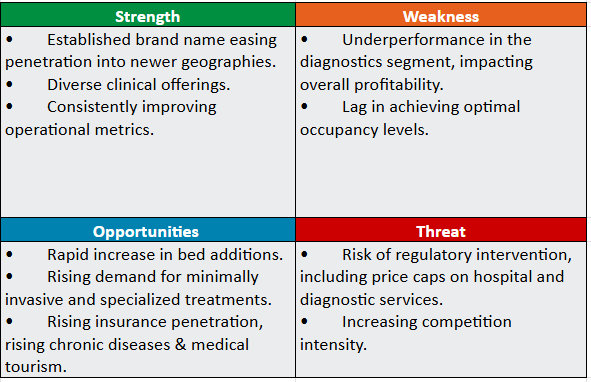

SWOT Evaluation

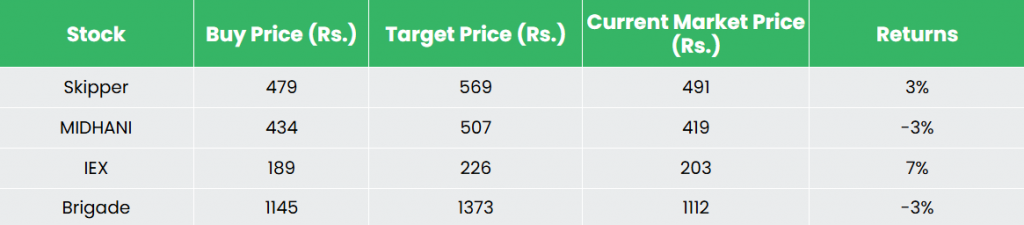

Recap of our earlier suggestions (As on 18 July 2025)

Skipper Ltd

Mishra Dhatu Nigam Ltd

Indian Vitality Alternate Ltd

Brigade Enterprises Ltd

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you could like

Publish Views:

49

")