Home demand-driven sectors are anticipated to hold a lot of the burden in 1 / 4 marred by exterior shocks, together with US tariff threats, geopolitical tensions in West Asia, and heightened cross-border pressure following the 22 April Pahalgam terror assault and India’s subsequent Operation Sindoor in Could, which focused terrorist camps in Pakistan and Pakistan-occupied Kashmir.

“Charge delicate sectors like banks, NBFCs (non-banking monetary corporations), choose auto [companies] and realty are prone to profit,” mentioned VK Vijayakumar, chief funding strategist at Geojit Investments. “Aviation, telecom and resorts will proceed to do properly, whereas IT will stay a drag on earnings.”

Jay Kothari, lead market strategist at DSP Mutual Fund, finds oil advertising and marketing corporations (OMCs) and gasoline distributors tactically engaging. “Decrease vitality prices ought to enhance [OMCs’] advertising and marketing margins in Q1, whereas export-linked sectors like IT, pharma and textiles could face near-term earnings headwinds,” he mentioned.

Even so, analysts count on beneficial properties to stay concentrated in pockets, with some sectors persevering with to lag and wealthy valuations limiting market-wide upside.

Earnings progress faces structural constraints

India’s post-pandemic bull run has but to coalesce round a defining macro theme. In contrast to the capex-led cycle of the 2000s or the consumption surge of the 2010s, latest beneficial properties have been pushed extra by margin growth than sturdy demand progress.

“I’m cautiously optimistic that the earnings cycle has type of bottomed out and we might be 12–14% [Nifty] earnings progress in FY26,” mentioned Manish Jain, head of fund administration at Centrum Broking. “However I don’t count on any dramatic modifications in Q1 in comparison with This fall.”

In Q4FY25, company India’s earnings per share (EPS) rose 10-12%, however full-year earnings progress got here in beneath 5%. Furthermore, earnings downgrades continued to outpace upgrades, indicating that analysts are tempering their expectations heading into the brand new fiscal 12 months.

A latest report from Nuvama Institutional Equities notes that the margin growth story could also be nearing its limits. Company restructuring has largely run its course, and premiumization traits are starting to normalize throughout sectors.

This has led India Inc.’s revenue progress to sluggish and align extra carefully with income progress, which remained sluggish in FY25. Actually, India’s income progress has trailed different rising markets (EMs) post-Covid, averaging beneath 10% for eight consecutive quarters, based on Nuvama.

As India’s earnings differential narrows with different EMs, the danger of overseas institutional outflows will increase, the report warned.

Regardless of this, the market nonetheless expects mid-teens EPS progress over the following two years, forecasting continued growth in each margins and topline. If these expectations aren’t met, the hole between precise and projected earnings may result in extra sustained earnings downgrades, based on the report.

Home consumption: A swing issue

Whereas India’s financial system has demonstrated resilience to exterior shocks in latest quarters, high-frequency indicators recommend {that a} secular pickup in consumption stays out of attain.

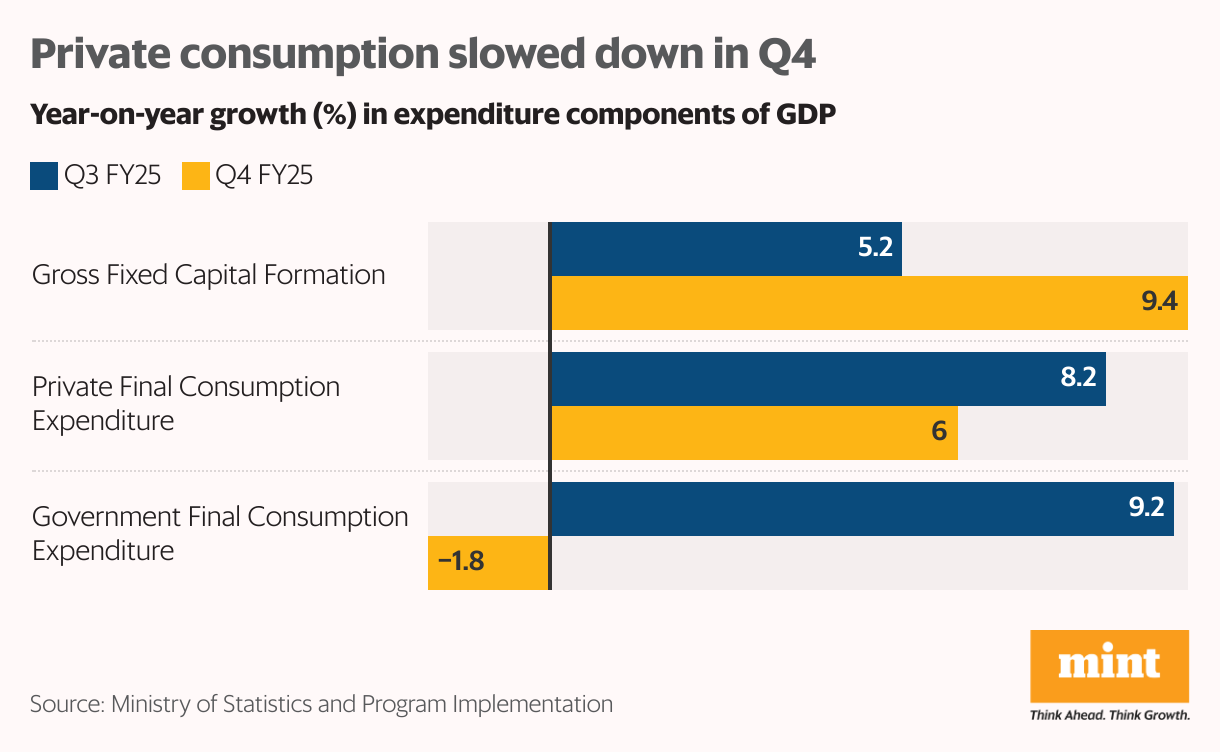

Economists count on GDP progress to average to six.5% in Q1FY26, down from 7.4% in This fall FY25. That soar in This fall was partly supported by a pointy 41% on-year drop in authorities subsidy payouts, which helped carry the headline GDP. Gross worth added (GVA), a cleaner measure of underlying exercise, rose 6.8%, revealing weaker momentum.

Personal consumption, which made up 56.5% of GDP in FY25 based on CMIE knowledge, continued to lag. City demand stays inconsistent, with family consumption slowing in This fall from Q3. A lot of the hope for a broader uptick now rests on rural demand.

Radhika Rao, senior economist and government director at DBS Financial institution, famous that falling inflation ought to enhance family funds and help non-public consumption within the coming quarters. Rural households are prone to profit extra from higher crop yields as a result of a well timed monsoon, she mentioned.

“Following a robust This fall our proxy gauge for rural demand has held up into April as properly. Quantity progress seems stronger in non-food classes,” Rao added.

Manish Jain of Centrum Broking expects shopper durables, NBFCs, and choose auto corporations to learn from the agricultural restoration theme.

Debopam Chaudhuri, chief economist at Piramal Group, additionally sees indicators of revival in budget-focused segments. “I stay optimistic a couple of broader demand revival because the 2025 festive season approaches,” he mentioned.

Valuations depart little room for error

Whilst near-term demand traits present enchancment, markets are pricing in a robust restoration. But, sector management has remained fluid, with most themes—from manufacturing to consumption to digital, having already loved their highlight post-Covid.

In response to Nuvama, five-year compound annual progress charges for all sectors now vary between 10–30%, leaving little that appears essentially low cost.

“I do not assume the flavour of the market goes to vary an entire lot from what we now have seen within the final 5 years,” mentioned Jain. “One needs to be very sharp and nimble to maintain tempo with the sector rotations in giant caps. With small and mid-caps, it’s at all times a growth-driven bottom-up strategy.”