No matter you consider Tesla (NASDAQ: TSLA), this can be a inventory about which there appears to be no scarcity of opinions.

Simply trying on the share value chart already provides a sign of the wild swings in sentiment we have now seen about Tesla within the inventory market at completely different factors.

It’s down 36% for the reason that begin of the 12 months. That could be a massive fall for any firm, not to mention one which – even after the autumn – instructions a market capitalisation of over $800bn.

Regardless of that, the share remains to be up by over 50% previously 12 months alone. Over 5 years, issues look even higher: shareholders over that interval at the moment are sitting on a 437% acquire.

Tesla appears to confuse many traders

So, what’s going on right here?

A few of the motion displays Tesla’s nearly meme-like qualities for a corporation of its dimension, with numerous traders taking a robust view primarily based on elements like their opinion of its chief govt.

However most meme shares have a market capitalisation of some billion {dollars} at most. I feel there’s something very completely different happening on the subject of Tesla inventory: even many subtle traders are genuinely confused about the right way to worth it.

Is it a automobile maker with enticing revenue margins in recent times, now seeing gross sales volumes degree out?

In that case, even including in some further worth for its fast-growing energy era enterprise, the present market capitalisation appears crazy to me. It’s 20 occasions the market cap of Ford, for instance.

Or, is Tesla actually an funding case a couple of confirmed capacity to innovate and disrupt large industries, because it has already achieved with vehicles and will but do with taxis and robotics? In that case, I see an argument for Tesla doubtlessly being a long-term discount on the present value.

Investing on information, not hope

Tesla has achieved a really spectacular job on the subject of enterprise progress. Income has soared in recent times. Damaged down right into a quarterly income quantity, although, and because the chart beneath exhibits, there’s clear trigger for concern for Tesla traders proper now.

Created utilizing TradingView

This week, the corporate introduced a woeful first quarter as the corporate fights fires on a number of fronts. Not solely has it seen falling gross sales, however earnings slumped too. The primary quarter noticed revenues fall by a fifth in comparison with the identical interval final 12 months.

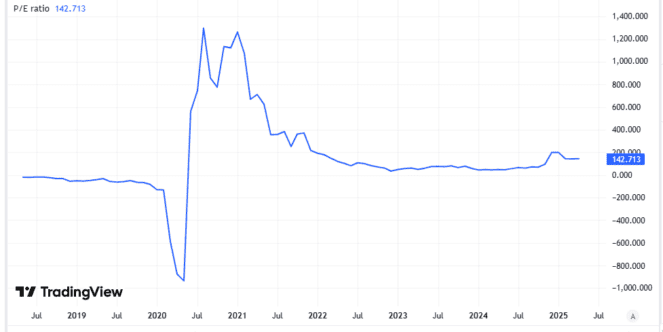

In the meantime, earnings per share (on a Usually Accepted Accounting Ideas foundation) fell 71% in comparison with the identical quarter final 12 months. Already, Tesla’s price-to-earnings (P/E) ratio of 143 appears far too excessive for me to contemplate investing. But when earnings fall, the valuation will look even much less enticing.

Created utilizing TradingView

I do see hope for the non-automotive enterprise. Vitality era and storage income surged 67% 12 months on 12 months within the first quarter. But it surely nonetheless represents solely round 15% of whole income.

For now, at the least, energy era and pipeline tasks like automated taxis look too unproven to justify the present Tesla valuation. With rising competitors, the car enterprise additionally appears overvalued to me.

Taken collectively, primarily based on present information not future hopes, I see Tesla inventory as overvalued and won’t be investing.