As soon as a darling of overseas institutional traders (FIIs), TeamLease has seen its FII possession plunge from 42% in June 2022 to simply 11% now. In the meantime, home institutional traders (DIIs) are taking a contrarian stance, elevating their stake from 16% to 48% over the identical interval.

This divergence raises a key query: Is TeamLease nonetheless a strong guess amid mounting headwinds in specialised staffing, notably IT?

Learn this | Hiring slowdown: Regulatory curbs, feeble festive season hit job development

Staffing firm, or a proxy for Indian IT?

Based in 2001, TeamLease has grown into considered one of India’s largest staffing companies, commanding a 6% market share. It has positioned over 2.3 million staff throughout 3,900 shoppers and operates in 28 states, constructing a powerful status with a various consumer base.

Learn this | In charts: Sombre temper grips India’s high IT companies amid tariff tantrums

The corporate went public in 2016 and swiftly pivoted to IT staffing by a sequence of acquisitions. It snapped up ASAP Information Techniques and Nichepro Applied sciences that 12 months, adopted by Keystone Enterprise Options and Freshers World in 2017. In 2019, it additional bolstered its IT staffing arm by buying the IT infrastructure divisions of Ecentric and IMSI. By 2021, TeamLease had positioned itself as the biggest IT staffing agency in India.

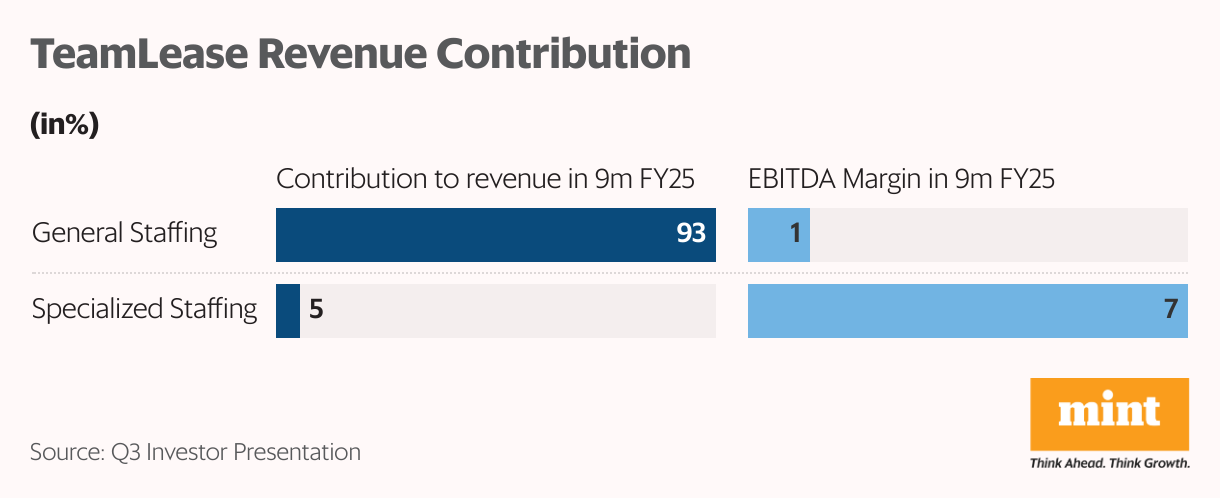

But, IT staffing is simply a small slice of its enterprise. Common staffing–protecting sectors like BFSI, FMCG, client durables, and telecom–accounts for 93% of revenues however is very aggressive and carries slim margins. The corporate’s per-associate-per-month (PAPM) margin typically staffing has slipped from ₹744 in FY18 to ₹670 as of December 2024.

In distinction, specialised staffing, which incorporates IT staffing, represents simply 5% of revenues however drives margins. Common staffing traditionally has fetched a 3% gross margin, whereas IT staffing delivers a far more healthy 16%. Within the first 9 months of FY25 (9MFY25), the Ebitda margin in specialised staffing stood at 7%, in comparison with simply 1% typically staffing.

This disparity explains why TeamLease’s inventory efficiency is so intently linked to the fortunes of the IT sector.

Specialised staffing sputters as IT, apprenticeships falter

The 2 pillars of TeamLease’s high-margin specialised staffing phase– IT staffing and Diploma Apprenticeship (DA)–are each struggling towards regulatory and business headwinds.

Learn this | Mint Primer: What IT corporations’ This autumn present means for traders

Through the post-pandemic digitization increase, the IT sector was on a hiring spree, driving a 33% income surge for TeamLease in FY22. However quickly after, inflation issues took over, and the US Federal Reserve raised charges on the most aggressive tempo seen in a long time. This spelt unhealthy information for Indian IT, which derives greater than half of its revenues from exports to the US. It additionally got here to mild that Indian IT majors had over-hired.

Quarter after quarter of layoffs adopted, and hiring at Indian IT companies stays a shadow of the post-pandemic surge. TeamLease’s DA programme additionally took successful with the discontinuation of the Nationwide Employability Enhancement Scheme (NEEM) in December 2022.

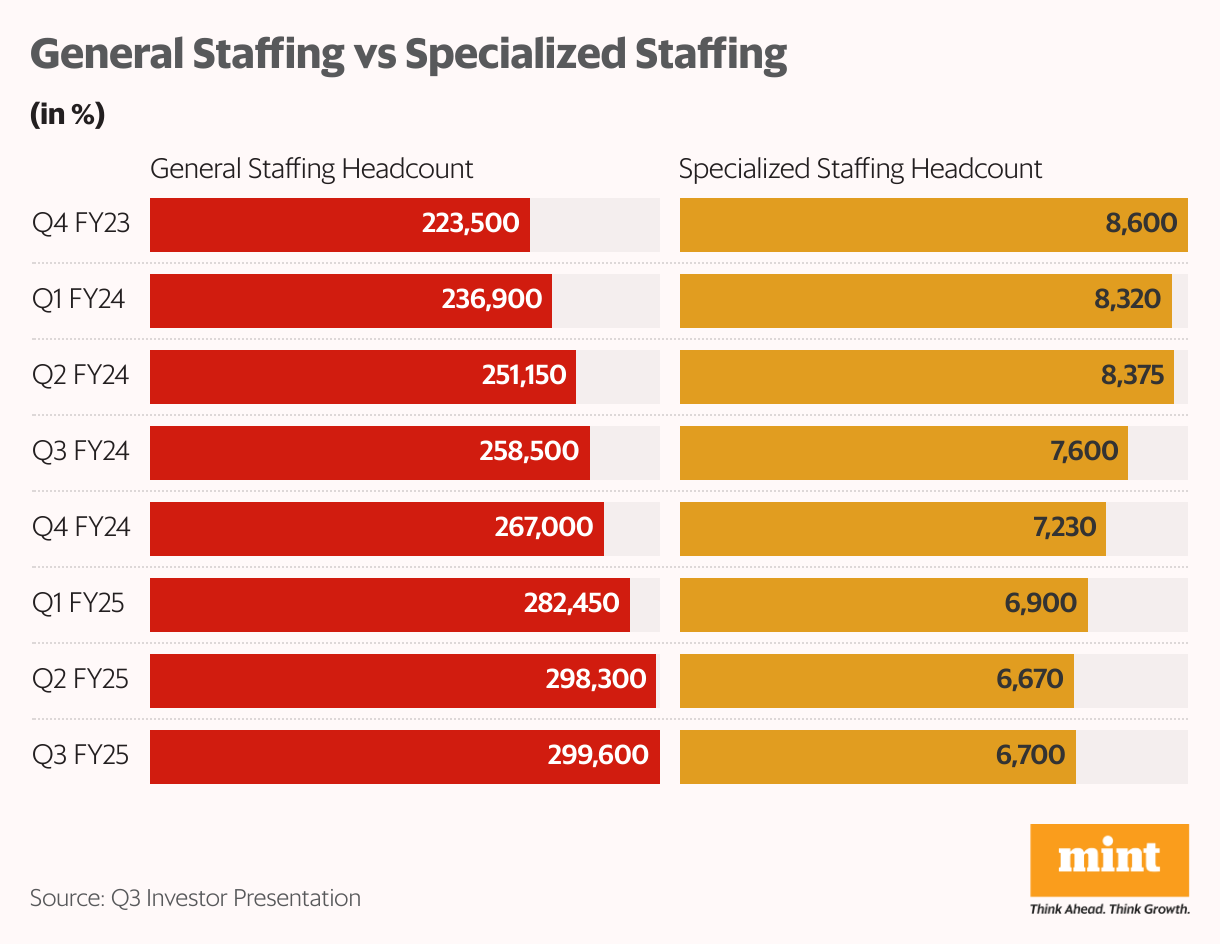

Consequently, at the same time as TeamLease’s common staffing headcount rose from 220,00 in Q4FY23 to 300,000 in Q3FY25, its specialised staffing numbers fell from 8,600 to six,700 in the course of the interval.

The primary 9 months of FY25 noticed common staffing revenues develop by 22% year-on-year, whereas income from specialised staffing declined by 2%. General income development for the corporate has slowed progressively, from 33% in FY22 to 19% in FY25 thus far. Its working margins have additionally shrunk to simply about 1%.

No cheer within the new 12 months

The inventory had briefly recovered between 2023 and 2024, buoyed by hopes of a US financial easing cycle and a possible IT sector rebound. However that optimism didn’t translate into exhausting numbers for TeamLease. The corporate’s fundamentals remained weak as hiring within the IT sector failed to select up.

Issues have solely worsened in 2025.

Tariff-led inflation and coverage uncertainty have weighed on company spending within the US, prolonging the droop in Indian IT. This has coincided with seasonal weak spot within the edtech area and appraisal cycles for its core workers. The implementation of the New Training Coverage additionally delayed admissions and billing, additional straining earnings.

Consequently, Ebitda margin for its different HR providers turned unfavorable, from 6.7% in 9MFY24 to (-)7.2% within the 9MFY25.

General Ebitda margin shrank from 1.5% to 1.2% between Q3FY24 and Q3FY25. Regardless of a 19% development in revenues to ₹2,931 crore, its working revenue declined 3% year-on-year to ₹35 crore and internet revenue noticed a 9% fall in the course of the interval.

However the highway forward holds promise

The corporate is about to announce its This autumn earnings on 21 Could.

As new shoppers are onboarded below a variable mark-up mannequin and automation and cost-cutting measures take impact, margins might even see some help. Sustained development typically staffing and growth into international functionality centres (GCCs) are additionally anticipated to mitigate ongoing IT sector stress.

Learn this | Captive issues: Why Cognizant has referred to as out the chance from GCCs

Losses on account of NEEM discontinuation have been recouped already, whereas the Nationwide Apprenticeship Promotion Scheme (NAPS) and Work Built-in Studying Program (WILP) have helped improve the headcount for its DA programme by greater than 2,000 in FY25 thus far.

Furthermore, as per TeamLease’s Apprenticeship Outlook Report for the quarter ended March 2025, internet apprenticeship outlook has elevated 8% sequentially to 76%, pushed primarily by dawn sectors resembling drones, electrical automobiles (EVs), and GCCs, a promising signal for future DA development.

Moreover, over the medium-to-long time period, stress within the IT sector could be anticipated to average, additional contributing in the direction of rising the share of specialised staffing providers on the firm.

Not too long ago, TeamLease additionally introduced acquisition of 80% stake in Ikigai Enablers Pte. This could assist it increase its specialised staffing enterprise in Singapore and Center East. It additionally bought 90% and 30% stakes respectively in TSR Darashaw HR Companies and Crystal HR, which ought to assist additional its foray into HR Tech. These acquisitions have been funded by inside accruals, thereby lending confidence to traders, particularly contemplating muted margins in recent times.

That is to say that over the long run, the outlook seems brighter as regulatory winds flip beneficial and specialised staffing picks up tempo.

For extra such analyses, learn Revenue Pulse.

For now, the main focus will stay on monitoring the share of specialised staffing, margins, and the combination of latest acquisitions. TeamLease’s robust steadiness sheet, characterised by low debt and comfy working capital, ought to present some cushion because it navigates near-term headwinds.

Ananya Roy is the founding father of Credibull Capital, a Sebi-registered funding advisor.

Disclosure: The writer doesn’t maintain shares of the businesses mentioned. The views expressed are for informational functions solely and shouldn’t be thought of funding recommendation. Readers are inspired to conduct their very own analysis and seek the advice of a monetary skilled earlier than making any funding selections.

Soars Over 40% on Earnings Beat: What’s Driving the Surge and Ought to You Care?")