Picture supply: Getty Photographs

Based mostly on payouts over the previous 12 months, Harbour Power (LSE:HBR) is likely one of the greatest dividend shares on the FTSE 250. As a result of its beneficiant yield, it sits comfortably throughout the high 10% of shares within the UK’s second tier of listed firms.

And following the acquisition of belongings beforehand owned by Wintershall Dea, it’s now the biggest oil and fuel producer within the North Sea. This transformational deal, which was accomplished in September 2024, means the group now has the monetary firepower to additional enhance its dividend.

Certainly, the corporate intends to pay $380m to legacy shareholders over the following 12 months. At present (9 January) trade charges, this equates to 21.5p (26.4 cents) a share. On the time of writing, Harbour Power’s shares are altering palms for round 265p. This suggests a yield of 8.1%, greater than twice the FTSE 250 common.

However returns to shareholders are by no means assured, notably within the oil and fuel sector. Earnings could be risky, which suggests dividends can fluctuate considerably from one interval to a different.

Nonetheless, in it’s quick existence as a listed firm, Harbour has a formidable report of steadily growing its payout (see desk beneath).

| Monetary 12 months | Dividend sort | Dividend per share ($) |

|---|---|---|

| 2021 | Closing | 0.11 |

| 2022 | Interim | 0.11 |

| 2022 | Closing | 0.12 |

| 2023 | Interim | 0.12 |

| 2023 | Closing | 0.13 |

| 2024 | Interim | 0.13 |

Extra earnings

Undoubtedly, this has been made doable by spikes in wholesale oil and fuel costs, notably in 2021 and 2022.

However it is a double-edged sword.

In response to public strain, the earlier authorities launched a ‘windfall tax’, formally generally known as the Power Income Levy (EPL). Not surprisingly, the corporate’s share worth has been steadily declining because the Could 2022 announcement.

Subsequent will increase imply the group now faces an efficient company tax fee of 78% on its earnings derived from the UK Continental Shelf.

Partially, this explains the acquisition of Wintershall Dea’s oil and fuel fields. None of those are in UK waters, subsequently the EPL doesn’t apply. And because of the deal, the group is now producing 90% greater than beforehand. This provides me some confidence that it may well proceed to develop its dividend.

Commodity costs

Present laws means the EPL will stay till 31 March 2030. However there are provisions for it to be scrapped.

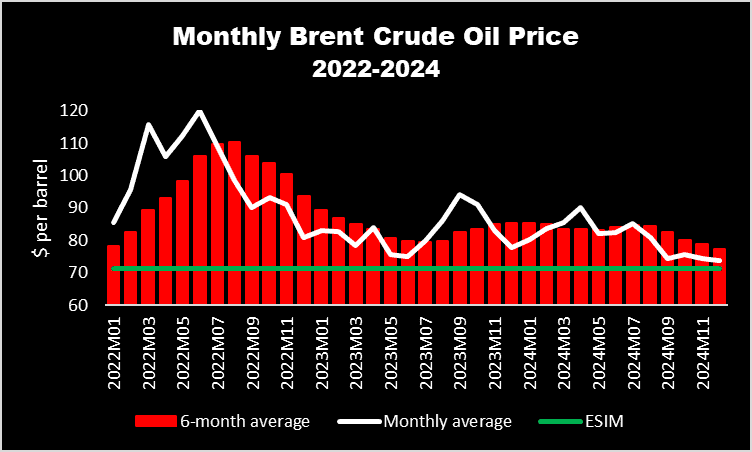

On the one hand, a falling oil and fuel worth would harm income. Nonetheless, if (for six consecutive months) the common month-to-month oil worth falls beneath $71.40 — and the fuel worth goes underneath 54p a therm — the ‘windfall tax’ shall be abolished.

However this seems unlikely to occur any time quickly.

Though Brent crude is falling, it nonetheless stays above the worth ground.

And I’m wondering if fuel costs will ever drop beneath 54p once more.

In my view, it seems to be as if the EPL is right here to remain.

My opinion

Regardless of this, I plan to maintain my Harbour Power shares.

That’s as a result of I feel diversifying away from the UK is an effective transfer.

And though it’s not possible to precisely predict future power costs, the extra earnings earned outdoors of Britain’s waters ought to assist be sure that the group is ready to — at the very least — preserve (in money phrases) its beneficiant dividend.