Each on occasion, a well-established however presently struggling company big is deemed too huge to fail. However historical past exhibits there isn’t any such factor. A number of corporations that had entrenched themselves deeply of their industries and had deep pockets and larger-than-life reputations are nowhere to be discovered now.

This Revenue Pulse article zooms in on three enterprise giants which have devolved into near-oblivion, and the cautionary tales they provide for traders.

Dewan Housing Finance Company Ltd: A home of playing cards

DHFL’s former chairman and promoter Kapil Wadhawan was not too long ago declared bankrupt after he didn’t honour private ensures for loans taken for the housing finance firm. Wadhawan and his brother Dheeraj Wadhawan, ex-director of DHFL, are additionally barred from the securities markets for 5 years and have been fined greater than ₹100 crore in penalty, together with others. What went fallacious?

DHFL was India’s third-largest housing finance firm. With a mortgage e book of ₹1 trillion, it was a drive to reckon with. However when Infrastructure Leasing and Monetary Companies Ltd (IL&FS) collapsed in 2018, lending to non-banks dried out. DHFL was no exception.

After all, what was occurring at DHFL was extra sinister than the industry-wide stress.

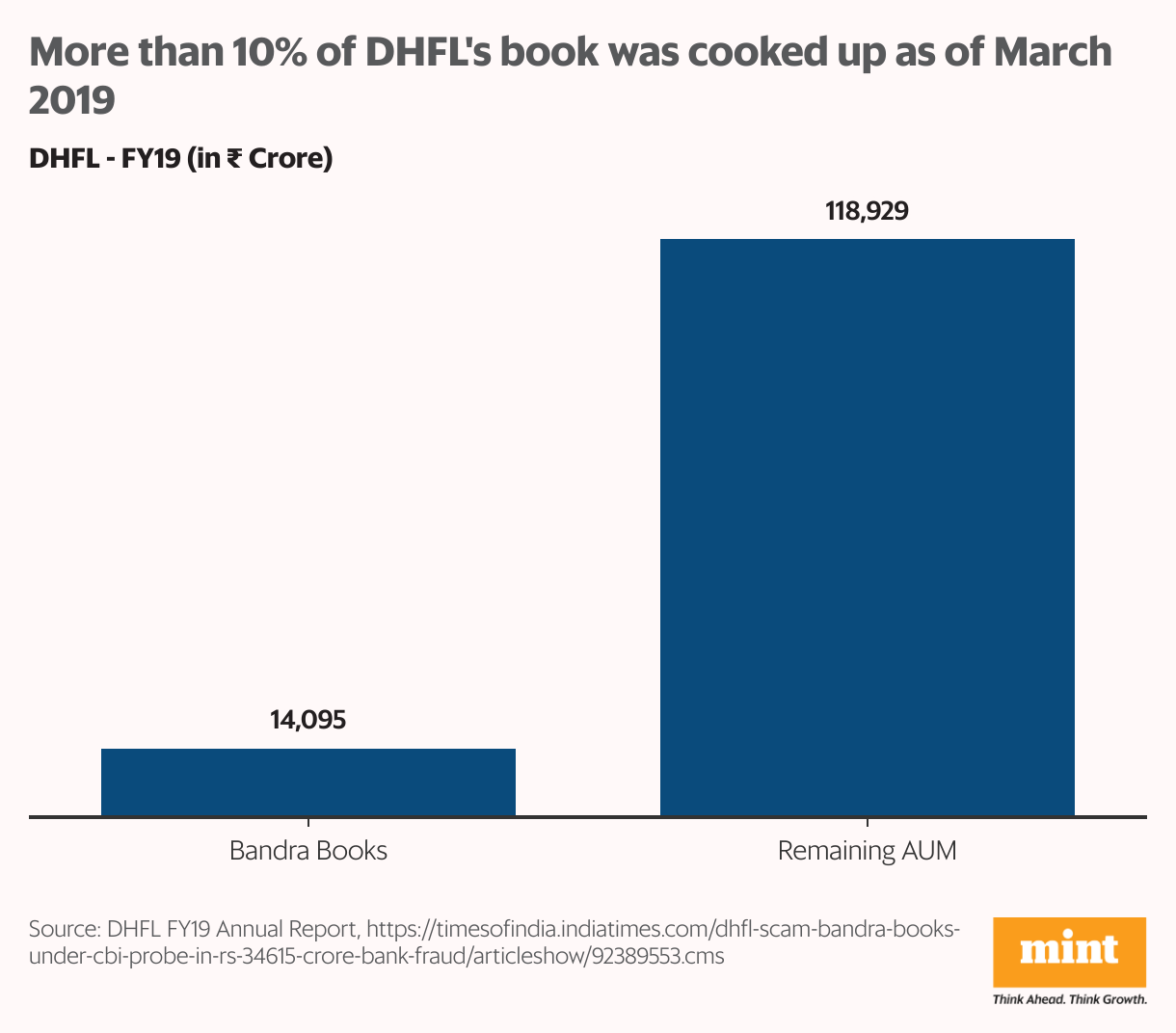

As banks and regulators grew to become extra vigilant, DHFL’s legacy turned out to be a pack of playing cards. A faux department in Bandra housed ₹14,000 crore of its e book as of March 2019, a whole lot of it cooked up. Reasonably priced housing loans disbursed by way of this department had been rerouted to greater than 80 shell corporations linked to the Wadhawans. Subsidies have been claimed below the federal government’s affordable-housing scheme, Pradhan Mantri Awas Yojana, and repayments have been recorded the place there have been none.

A mirage of monetary well being was maintained whilst greater than 10% of its e book was simply sizzling air. DHFL saved borrowing extra till banks, its lenders, began asking questions. Seventeen banks alleged fraud amounting to ₹34,615 crore.

A federal investigation ensued, and the Reserve Financial institution of India took DHFL off the promoters’ fingers. Almost ₹30,000 crore in losses adopted. Because the DHFL inventory corrected from ₹680 to lower than ₹20 per share in nearly a 12 months, greater than 95% of investor wealth was worn out.

DHFL was ultimately merged with Piramal Capital and Housing Finance Ltd in 2021, and now operates as an unlisted non-banking monetary firm.

Bhushan Energy and Metal Ltd: Insolvency deja vu

Bhushan Energy and Metal Ltd would be the solely firm to have been dragged to chapter courts thrice. BPSL itself was born out of the chapter of Jawahar Metals in 1987. It grew right into a formidable metal producer however crumbled below bold enlargement plans, piling debt, and alleged fraud, exacerbated by the crash in metal costs following the worldwide monetary disaster in 2007-09.

Bhushan Metal, an affiliated firm, suffered an identical destiny and was ultimately acquired by Tata Metal Ltd.

BPSL knocked on the doorways of India’s chapter court docket in 2017 with ₹47,000 crore in dues to banks and ₹4,000 crore in alleged fraud. So dire was its downside that RBI ranked BPSL on the prime of its ‘Soiled dozen’ checklist of defaulters, which accounted for a fourth of India’s unhealthy loans on the time.

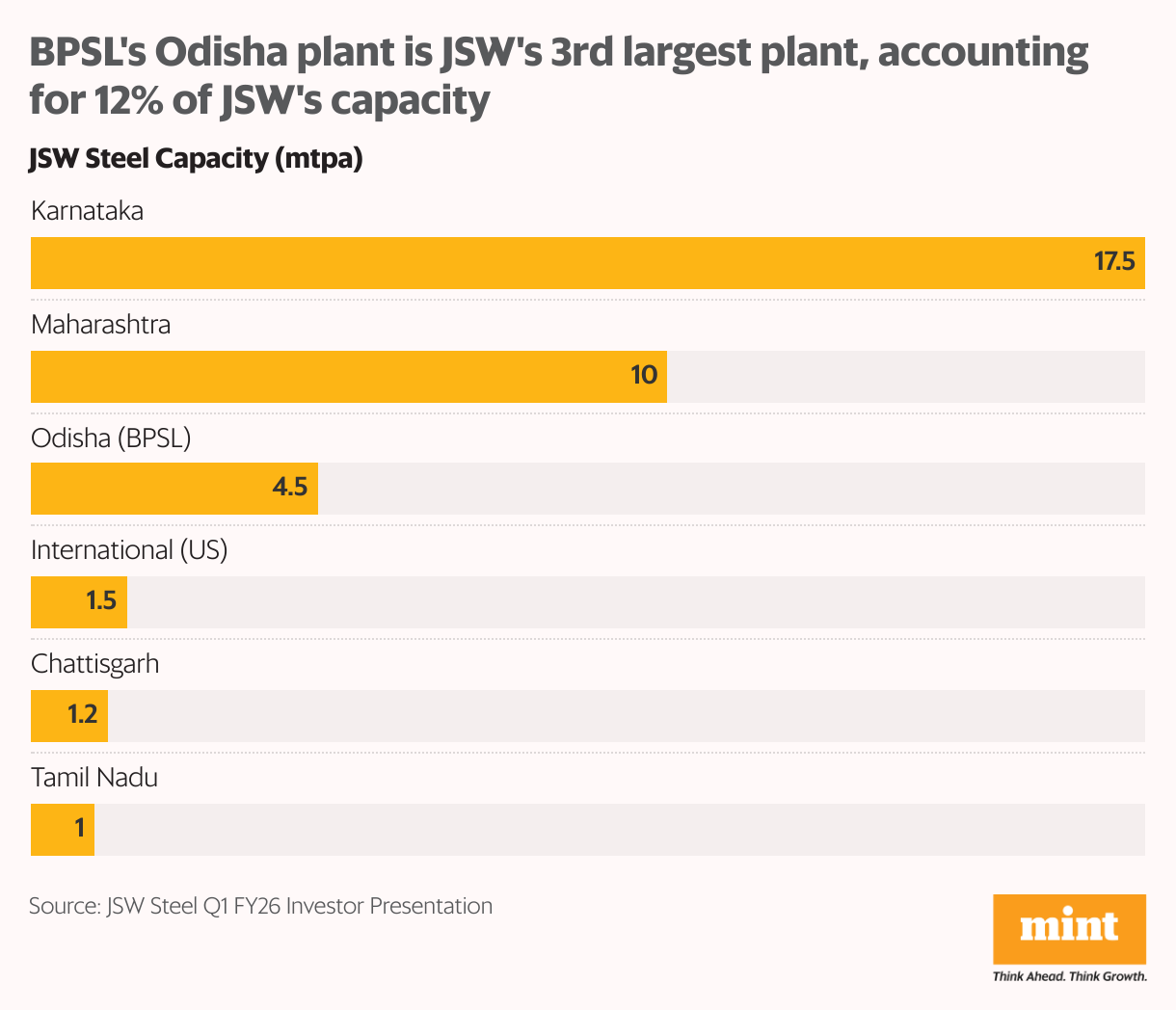

JSW Metal Ltd acquired BPSL for almost ₹20,000 crore in 2021 and expanded its steelmaking capability. BPSL now accounts for about 15% of JSW Metal’s whole capability and about 10% of its earnings earlier than curiosity, taxes, depreciation and amortization. JSW Metal plans to increase BPSL’s capability from 4.5 million tonnes every year (mtpa) now to five mtpa by September 2027.

However an surprising twist within the story arrived just a few months in the past when the Supreme Courtroom determined to annul the acquisition. Why? Through the insolvency proceedings, the Enforcement Directorate had tried to connect BPSL’s property amid allegations of cash laundering in opposition to the promoters. However this, the Nationwide Firm Regulation Tribunal (NCLT) had gone forward with the proceedings.

The apex court docket cited this alleged overreach by NCLT and operational collectors being handed the shorter finish of the persist with scrap the insolvency decision and order BPSL’s liquidation. The Supreme Courtroom recalled its order final month, permitting JSW Metal’s and BPSL’s monetary collectors to breathe a sigh of reduction.

Jet Airways: Nosedived after a miscalculated acquisition

Established as one of many first personal airways when India opened up its aviation sector within the Nineties, Jet Airways had a dream run for greater than 20 years. In a sector then dominated by the federal government, Jet Airways managed to carve a distinct segment for itself by providing superior service and timeliness.

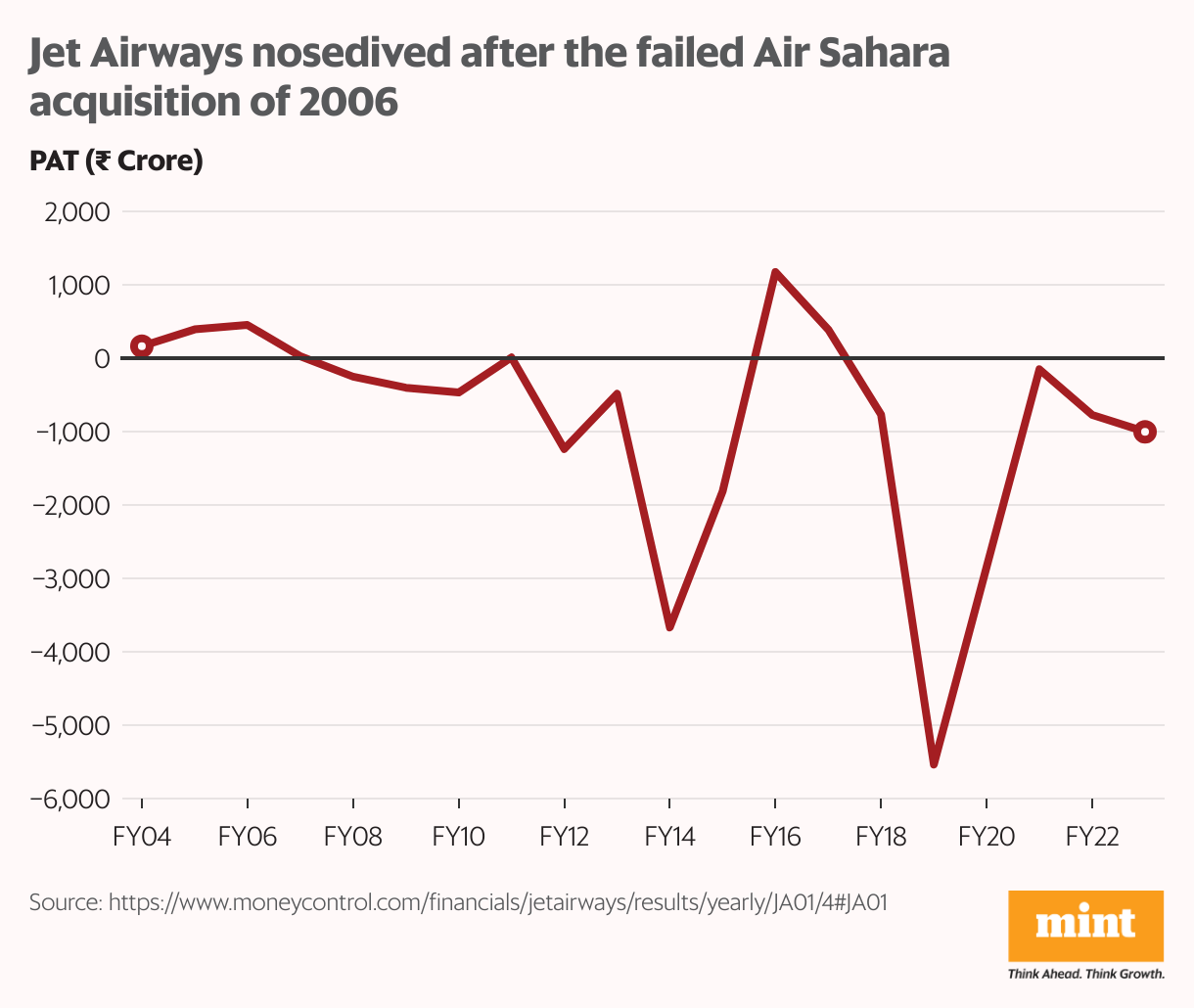

Issues took a flip for the more serious when the airline firm overstretched its assets by buying Air Sahara in 2006. Jet Airways piled up ₹6,500 crore in losses and in 2015 wrote off its ₹1,800 crore funding in Air Sahara. There was extra to return.

Jet Airways had partnered with the United Arab Emirates’ Etihad Airways and Air France, however the partnerships turned bitter whereas losses and debt continued to pile up. Cash-laundering allegations additionally surfaced. Jet Airways ended up accumulating greater than ₹8,500 crore in debt to lenders, ₹16,500 crore to staff and operational collectors, and ₹3,500 crore to fliers.

Jet Airways ultimately referred to as it quits in 2019. But, retail traders saved accumulating stake within the firm in anticipation of a profitable insolvency decision. However late final 12 months, the Supreme Courtroom ordered the liquidation of Jet Airways. Tens of hundreds of jobs and crores of rupees in retail investor funds have been misplaced within the ether.

The right way to keep away from such falling giants?

India’s company historical past is affected by many such examples of falling giants—Videocon, Amtek Auto, Alok Industries, Essar Metal, Kingfisher, and GoAir, to call just a few. However each such case of chapter was preceded by a number of alternatives for traders to chop their losses and exit.

When an organization’s losses mount and debt piles up, it’s a telltale signal of stress. Heavy promoter pledge is one other pink flag—it pins an organization’s destiny on fickle inventory costs.

Pending litigation, particularly with considerations round cash laundering, must also be taken critically. Significantly when seen at the side of different qualitative considerations similar to auditors’ opinions, complicated associated celebration transactions, and frequent churn in administration, board, and auditors. These ought to make traders sit up and take discover.

Lastly, when a enterprise doesn’t appear kosher, worry mustn’t maintain one again from reserving losses. Equally, greed mustn’t push one to build up positions in shares that look like a worth decide.

Regardless of taking all these preventive measures, an investor should still find yourself with just a few such shares of their portfolio. That’s when portfolio diversification can come to the rescue.

Key Takeaways

- Rising losses and mounting debt are early warning indicators of monetary stress—don’t ignore them.

- Excessive promoter pledges generally is a pink flag, as they tie an organization’s destiny to unstable inventory costs.

- Litigation, particularly round fraud or cash laundering, have to be handled critically.

- Auditor warnings, frequent churn in administration/board, and related-party dealings can sign deeper issues.

- Don’t let worry cease you from chopping losses when fundamentals deteriorate.

- Keep away from shopping for “worth picks” in troubled corporations pushed by greed or hypothesis.

- Portfolio diversification is important. Some failures are unavoidable regardless of due diligence.

Ananya Roy is the founding father of Credibull Capital, a Sebi-registered funding adviser. X: @ananyaroycfa

Disclosure: The creator doesn’t maintain shares of the businesses mentioned. The views expressed are for informational functions solely and shouldn’t be thought of funding recommendation. Readers are inspired to conduct their very own analysis and seek the advice of a monetary skilled earlier than making any funding selections.