Picture supply: Getty Photos

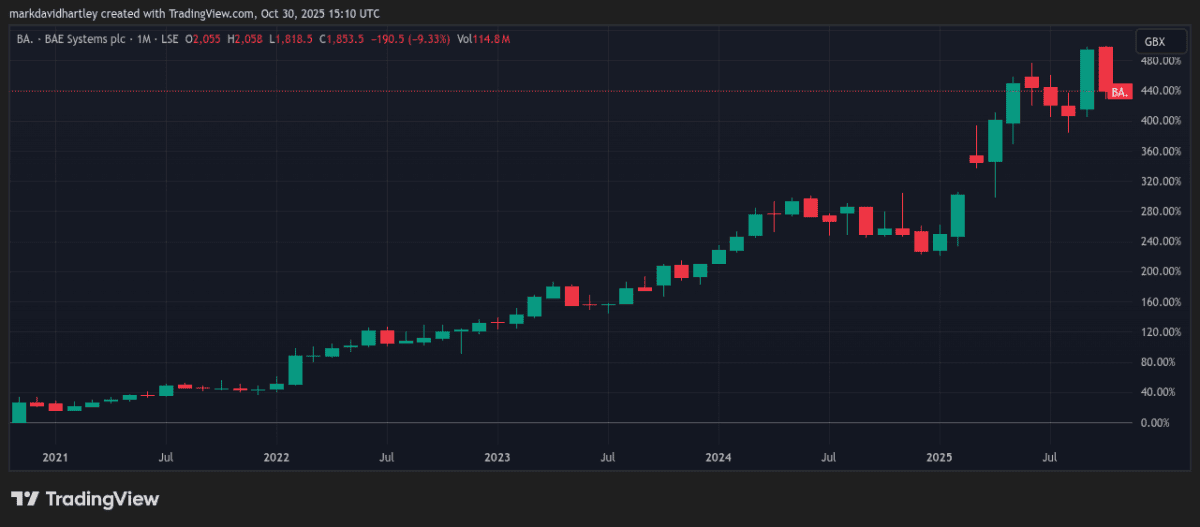

BAE (LSE:BA) shares have rocketed an unimaginable 440% since November 2020, making the defence large one of many FTSE 100’s most exceptional restoration tales. After the pandemic struck, the inventory sank to only 341p in late October 2020, as international markets panicked and traders fled something cyclical.

Quick ahead six years, and the shares now commerce above 1,800p — close to all-time highs.

An investor daring sufficient to place £5,000 into BAE shares at their low level could be sitting on roughly £27,000 right this moment, together with dividends. That’s the form of long-term efficiency many dream of.

However the query now’s whether or not the beneficial properties are all gone, or does the inventory nonetheless deserve a spot on an investor’s radar? Let’s take a better look.

Document-breaking contracts

BAE’s been a transparent beneficiary of rising defence budgets throughout Europe following the battle in Ukraine. The corporate not too long ago confirmed report order books and has raised its full-year steering twice, citing robust demand for fight techniques, submarines and munitions.

Simply weeks in the past, the group secured a £4.6bn UK-brokered contract to ship 20 Eurofighter Hurricane jets to Türkiye. That’s one of many largest export offers for British aerospace in years, supporting 1000’s of home jobs and making certain regular money inflows for years to return.

In the meantime, Norway’s chosen BAE’s Sort 26 frigate design for its next-generation naval fleet – one other vital export and manufacturing win. It’s the identical platform adopted by the UK, Australia and Canada, serving to BAE set up itself as a cornerstone of allied naval functionality.

For traders, these contracts counsel long-term visibility of earnings, and I feel that’s one thing price weighing up when assessing the corporate’s valuation right this moment.

A reputational threat

Nonetheless, it’s not all plain crusing. The corporate not too long ago confronted an uncomfortable story within the press after ending assist for its Superior Turbo-Prop (ATP) plane, which has grounded planes used to ship meals help throughout Africa. Kenyan operator EnComm claims BAE misled it over the plane’s future and is now pursuing authorized motion.

Whereas the dispute might not have materials monetary penalties, the reputational harm may show extra vital. For a corporation more and more judged on its environmental, social and governance (ESG) requirements, this type of controversy provides a threat issue traders ought to take into consideration rigorously.

Financially, BAE stays in wonderful well being. The group generates robust money move from long-term authorities contracts and has continued to lift its dividend, at the moment yielding round 2.6%. Steering has been upgraded twice this 12 months due to resilient demand for its digital techniques and submarine programmes.

In an unpredictable international financial system, I feel it’s nonetheless an organization with a promising future – one with dependable earnings, stable progress prospects and a shareholder-friendly dividend coverage.

Ultimate ideas

There’s little doubt that BAE has robust business momentum, however reputational and authorized dangers imply traders ought to weigh up how sustainable this progress actually is. As scrutiny intensifies over the human penalties of defence contracts, the corporate’s hardest battles is probably not fought within the skies – however within the courtroom of public opinion.

Nonetheless, demand for its experience is simply rising, so in my opinion, it stays one of many FTSE 100’s high defensive shares to contemplate for long-term progress and revenue.