Any mortgage for which the principal or curiosity fee is overdue for no less than 90 days is known as a non-performing asset (NPA). Gross NPA refers back to the complete quantity of debt that has stopped producing earnings for the financial institution. Internet NPA accounts for provisions – funds that banks or monetary establishments put aside to cowl potential future losses from loans which are more likely to default.

Excessive NPAs are a sign of poor monetary well being as they place a major burden on a lender’s operations and threaten its stability. Listed here are 5 banks with excessive NPAs over the previous 5 years.

#1 Punjab Nationwide Financial institution

The financial institution has a five-year common gross NPA ratio of 8.86% and a internet NPA ratio of two.88%. Its mortgage guide is dominated by company debt, however micro, small and medium enterprises (MSMEs) and the agriculture sector account for almost all of NPAs.

For FY25, the gross NPA ratio was 3.95% and internet NPA ratio at 0.4%. For the June 2025 quarter, gross NPAs stood at ₹42,600 crore and internet NPAs at ₹410 crore. The financial institution has guided for a gross NPA ratio under 3% and internet NPA ratio of 0.35% for FY26.

Gross and internet NPAs have fallen persistently over the previous few years on account of enhancements in asset high quality, aggressive write-offs, and a extra stringent credit score coverage. Regardless of all this, PNB stays among the many prime banks with the best gross NPA and internet NPA ratios.

Internet curiosity earnings elevated at a compound annual development charge (CAGR) of seven% over the previous 5 years, whereas internet revenue clocked a 48.5% CAGR. Provisions decreased by greater than half throughout this era.

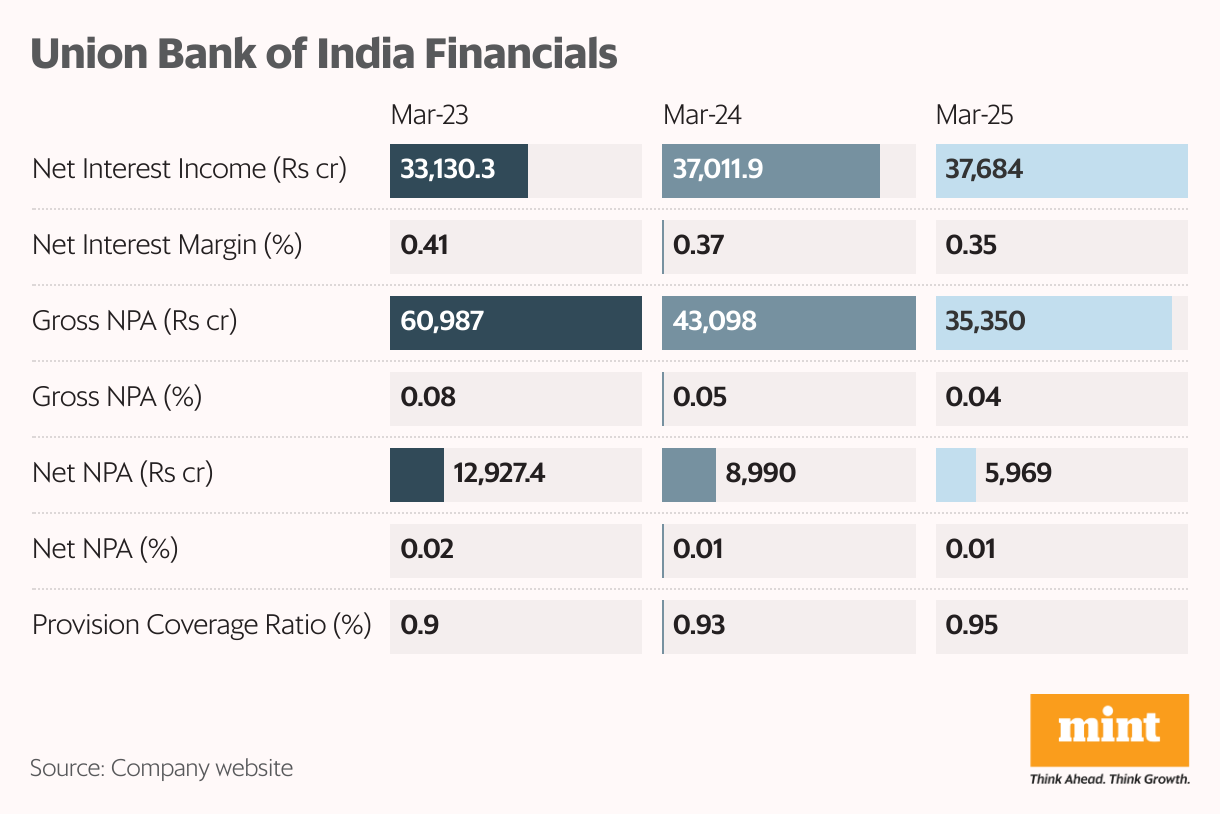

#2 Union Financial institution of India

The financial institution has a five-year common gross NPA ratio of 8.15% and a yearly common internet NPA ratio of two.33%. Union Financial institution of India’s mortgage guide is dominated by retail, agriculture and MSME loans, which comprise 54% of complete advances. Corporates are the following greatest section, with securities rated ‘A’ and above comprising 85% of the company mortgage guide.

In FY25, the financial institution’s gross NPA and internet NPA stood at 3.6% and 0.63%, respectively, their lowest ranges up to now 5 years. The first causes for this had been aggressive write-offs, recoveries of dangerous money owed, and a better provision protection ratio.

The financial institution is now consistent with gross NPA steerage of lower than 4%, and goals to enhance this additional via stringent credit score insurance policies. Nevertheless, the full internet NPAs have grown from ₹6,300 crore to ₹7,300 crore in simply 12 months, primarily because of new NPAs added through the yr. Nonetheless, the financial institution is taking measures to make sure its asset high quality stays intact. It additionally elevated its provision protection ratio by two share factors to accommodate new dangerous money owed.

Internet curiosity earnings and internet revenue elevated at a CAGR of 8.7% and 44.5%, respectively, whereas the provisions fell barely, indicating bettering asset high quality.

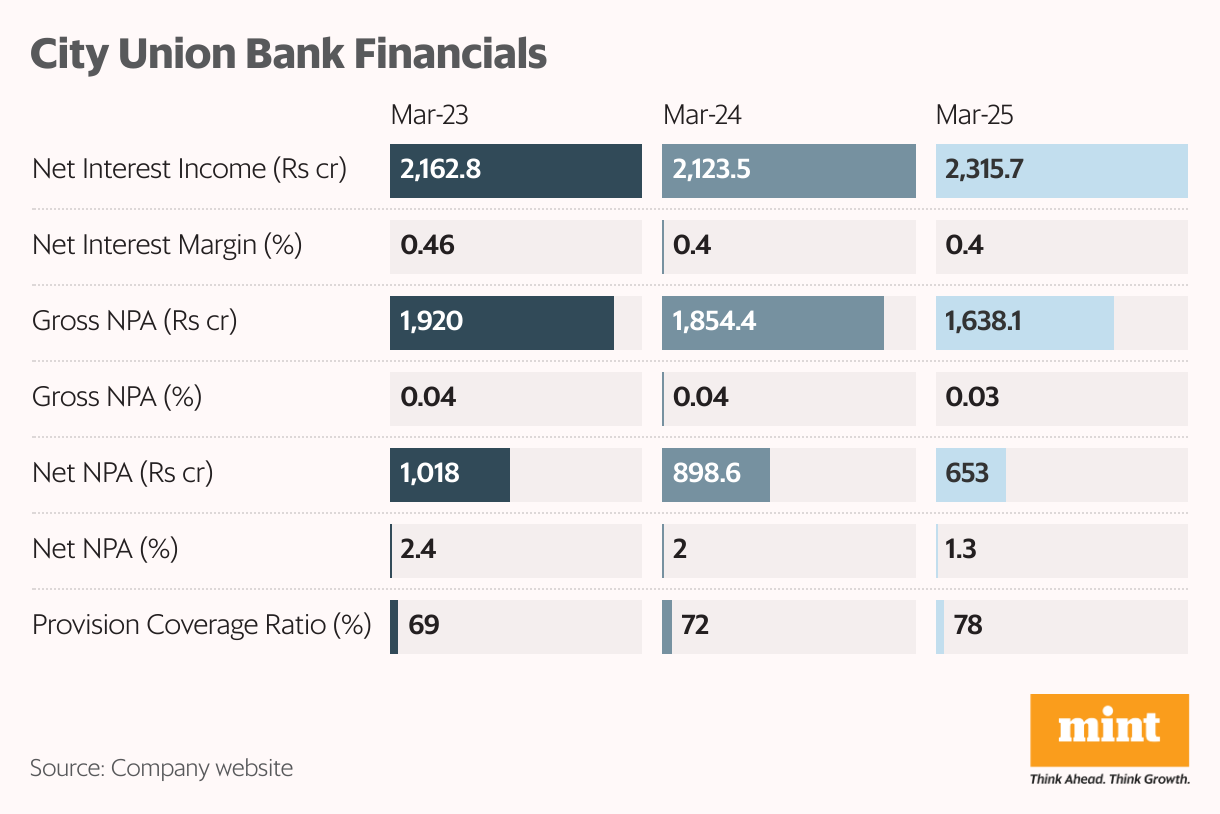

#3 Metropolis Union Financial institution

The financial institution has a five-year common gross NPA ratio of 4.25% and a yearly common internet NPA ratio of two.3%.

In FY25, the gross and internet NPA ratios stood at 3.1% and 1.2%, respectively. Gross NPAs fell significantly from ₹1,850 crore to ₹1,630 crore, whereas internet NPAs fell from ₹890 crore to ₹650 crore.

The financial institution’s mortgage guide is dominated by MSME loans, adopted by agricultural loans. Each classes have greater NPAs than others. Though the financial institution’s asset high quality has been bettering over the previous few years, it expects slippages to be round ₹700 crore in FY26. Therefore, the provisions are anticipated to extend barely for the yr.

Metropolis Union Financial institution has been taking in depth measures to enhance its asset high quality with a strict mortgage restoration coverage and credit score danger administration coverage.

This has improved its financials. Prior to now 5 years, the financial institution’s internet curiosity earnings and internet revenue elevated at a CAGR of 4.8% and 13.7%, respectively, whereas provisions fell by greater than ₹300 crore, indicating a wholesome mortgage guide.

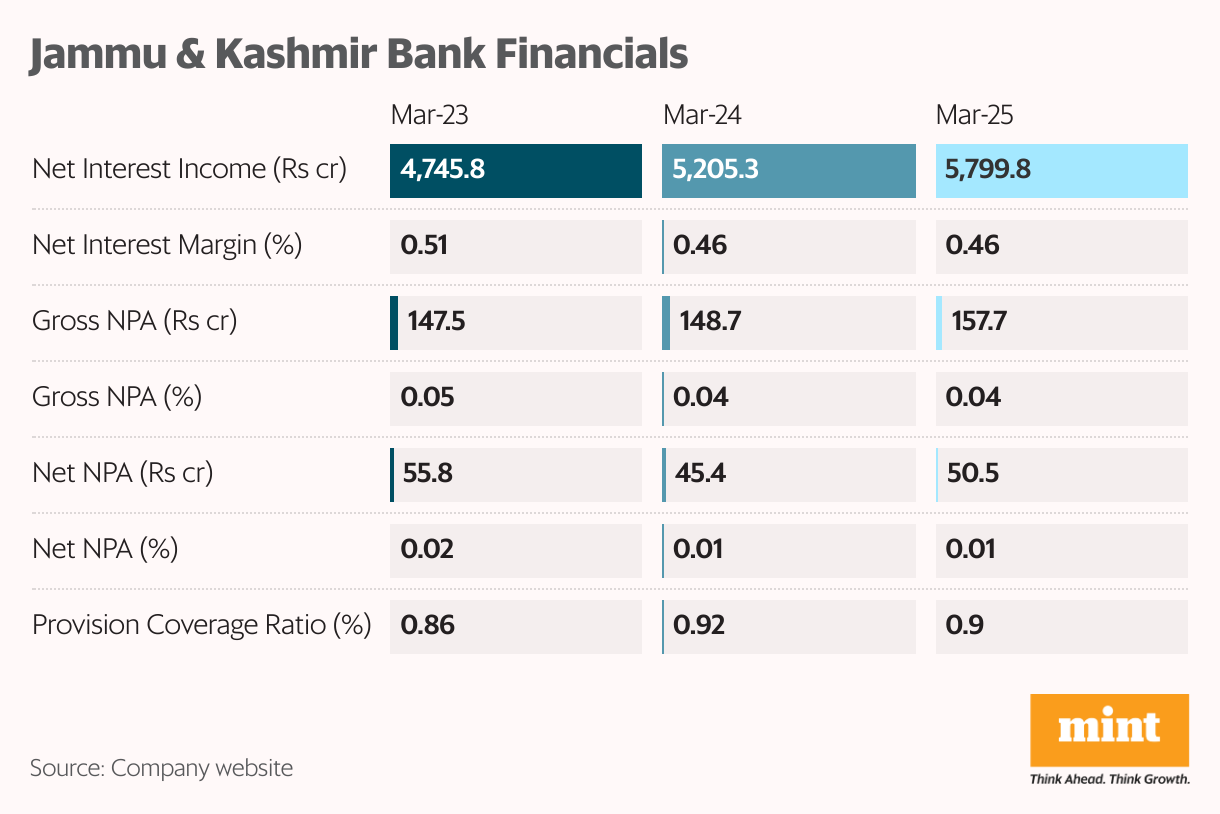

#4 Jammu & Kashmir Financial institution

The financial institution has a five-year common gross NPA ratio of 5% and a yearly common internet NPA ratio of two.15%. In FY25, the gross and internet NPA ratio stood at 3.8% and 1.25%, respectively, down from 4.1% and 1.3% in FY24.

The financial institution’s mortgage guide is dominated by retail, MSME, and agriculture advances (70%), adopted by company advances (30%). Inside the company advances, 60% of the debtors are rated AAA. Within the retail, MSME, and agriculture advances class, the vast majority of the dangerous money owed are within the agriculture and MSME classes.

The financial institution’s asset high quality has been bettering on account of mortgage recoveries, upgrades and decrease slippages. Nevertheless, within the June 2025 quarter, the slippages elevated on account of excessive dangerous money owed.

Internet curiosity earnings and internet revenue elevated at a CAGR of 9% and 37.2% up to now 5 years, whereas provisions fell barely on account of steady asset high quality.

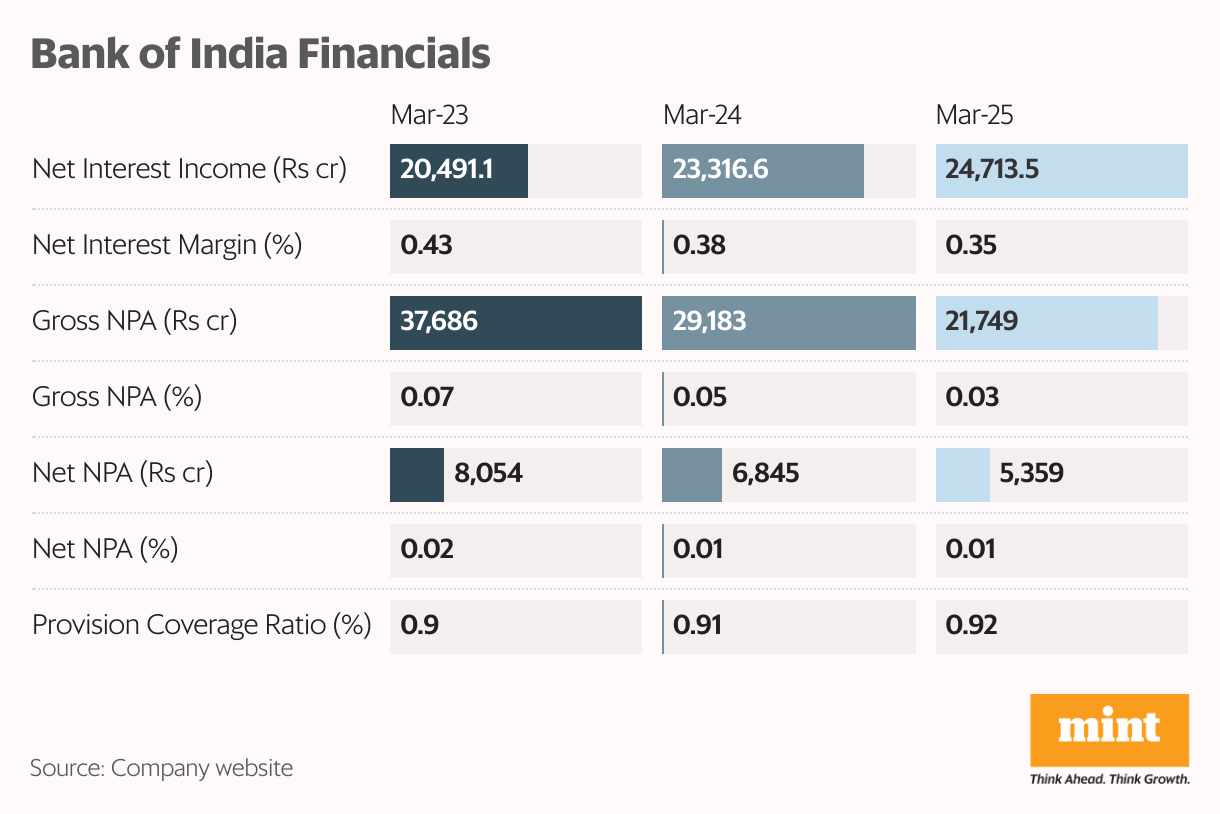

#5 Financial institution of India

The financial institution has a five-year common gross NPA ratio of 6.57% and a yearly common internet NPA ratio of 1.54%.

Financial institution of India’s mortgage guide is dominated by agriculture, MSME and retail loans. With respect to company loans, the vast majority of the score profile is dominated by AAA-rated securities (72%).

In FY25, the financial institution’s gross and internet NPA ratio stood at 3.27% and 0.82%, respectively. Slippages had been additionally excessive through the yr. Nevertheless, owing to write-offs and recoveries, gross NPA and internet NPA ratios fell barely from the earlier yr. Administration is optimistic about decreasing gross and internet NPAs ratios additional and has guided for a internet NPA ratio of 0.7% in FY26.

Internet curiosity earnings and internet revenue elevated at a CAGR of 11.4% and 35.6% up to now 5 years, whereas provisions remained steady at ₹7,800 crore.

Conclusion

Gross NPA ratios and internet NPA ratios of those banks have fallen considerably over the previous 5 years. That is primarily as a result of throughout 2015-2018, the Reserve Financial institution of India (RBI) reviewed the asset high quality of banks and found a considerable amount of dangerous loans.

With the worst already behind banks, the RBI and authorities have taken steps to cut back NPAs via capital infusion, aggressive write-offs, excessive provisions, recoveries below the Insolvency and Chapter Code, and improved lending practices.

As well as, company deleveraging and an financial restoration have pushed NPAs all the way down to multi-year lows, strengthening the Indian banking sector.

That mentioned, one have to be cautious about banks with excessive NPAs. It’s all the time higher to put money into these with persistently rising curiosity earnings, declining NPAs, and bettering internet revenue.

Pleased investing!

Disclaimer: This text is for data functions solely. It isn’t a inventory suggestion and shouldn’t be handled as such.

This text is syndicated from Equitymaster.com

delivered a robust 2Q25 amidst volatility")