Firm Overview

CMPDI is a mining consultancy agency included in 1975 and a subsidiary of Coal India Restricted, recognised as one of many largest consultancy service suppliers within the coal and mineral sector in India. The corporate presents end-to-end consultancy spanning 4 enterprise verticals:

1) Geological Exploration and Useful resource Analysis (45.8% of 9MFY26 income) – Geological mapping, drilling, and useful resource analysis.

2) Mine Planning and Design Providers (19.7%) – Feasibility research, mine design, and infrastructure engineering.

3) Environmental Planning and Monitoring Providers (17.8%) – EIA/EMP preparation, mine closure planning, and air pollution management;

4) Geomatics, Distant Sensing and Survey Providers (16.7%) – Drone-based surveys, GIS mapping, and overburden volumetric measurement.

The corporate operates by seven regional institutes throughout main coalfield areas, supported by eight laboratories and one of many largest exploratory drill fleets for coal and minerals in India as of March 31, 2025 serving a consumer base of 76 shoppers as of December 31, 2025, spanning authorities our bodies, public sector undertakings, and personal sector entities.

Objects of the provide

The corporate is finishing up a 100% book-built Supply for Sale aggregating as much as Rs. 1,842.12 crore. The corporate is not going to obtain any proceeds from the Supply.

The objects of the Supply are:

- To hold out the Supply for Sale of as much as 10,71,00,000 Fairness Shares by the Promoter Promoting Shareholder.

- To realize the advantages of itemizing the Fairness Shares on the Inventory Exchanges.

Funding Rationale

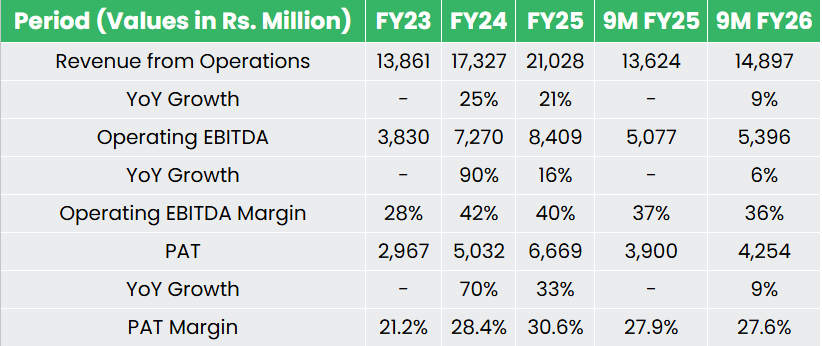

- Dominant Market place with structural demand visibility – CMPDI held roughly 61% market share in Indian mining consultancy in FY2025, with income rising at a 23.2% CAGR over FY23–25 towards its friends – RITES (-8.1%) and EIL (-3.7%) over the identical interval. The structural demand anchor is Coal India’s deliberate capability enhancement of roughly 787 MT by the opening and enlargement of fifty mines by FY2030, every requiring CMPDI’s full-service spectrum earlier than a single tonne of coal may be extracted. NMEDT (Nationwide Mineral Exploration and Improvement Belief) expenditure, a main supply of exploration task circulate, has grown from ₹831 million in FY2021 to ₹11,140 million in FY2025, with CMPDI among the many principal beneficiaries because the nodal exploration company beneath the Ministry of Coal. CMPDI’s income visibility is successfully policy-mandated, making it one of many few consultancies the place the demand pipeline is a perform of presidency targets fairly than market cycles.

- Non-CIL consumer base diversification – Income from non-CIL shoppers has grown 2.9x from ₹2,400 million in FY2023 to ₹6,921 million in FY2025, with exterior consumer share increasing from 17.3% to 32.9%, and the lively consumer base increasing from 38 shoppers as of March 31, 2023 to 76 shoppers as of December 31, 2025.Two coverage developments underpin the sustainability of this development – 1) MMDR Modification Act 2020, opening industrial coal mining to personal gamers, leading to 136 blocks auctioned up to now, representing a pipeline of assignments for accredited businesses equivalent to CMPDI; 2) Nationwide Essential Mineral Mission (NCMM), with an outlay of ₹163 billion aimed toward bettering self-reliance within the mining sector, making a probably new addressable marketplace for CMPDI’s present skillset.

- Asset-light mannequin, high-margin operations and powerful steadiness sheet – CMPDI operates an asset gentle enterprise mannequin with a excessive diploma of working leverage, evidenced by an annual capex of round ₹419 million in FY25, towards FY25 income of ₹21,028 million, which suggests a capex depth of beneath 2%. Worker value, the dominant fastened value, has declined in absolute phrases from ₹6,919 million in FY2023 to ₹6,085 million in FY2025, compressing worker value as a proportion of income from 49.9% to twenty-eight.9% and driving EBITDA margin enlargement from 27.6% to 40%. Notably, the corporate demonstrates sturdy financial earnings, ROCE stood at 48.6% in FY2025, implying a price unfold of ~35–36 proportion factors (towards an estimated weighted common value of capital of 13%).

- Operational Efficiency – In FY2025, CMPDI undertook 10.12 lakh meters of exploratory drilling, rising from 6.85 lakh meters in FY23, and delivered 437.9 line kilometres of 2D seismic surveys, marking 87% year-on-year progress. Mine planning challenge experiences submitted declined from 40 in FY2024 to 33 in FY2025 and 5 in 9M FY2026, at the same time as total income continued to develop, suggesting rising contribution from exploration and geomatics verticals.

Working money circulate transformed at roughly 100.6% of PAT in FY2025 and 99.6% in 9M FY2026, reflecting sturdy earnings high quality. Money and financial institution balances stood at ₹12,148 million as of December 31, 2025, the corporate carries no long-term debt, with nearly 0 finance prices, leaving the steadiness sheet solely unburdened.

Key Dangers

- OFS-Threat – The IPO is solely an Supply for Sale, implying no main capital infusion into the enterprise and a partial monetization of promoter shareholding.

- Purchaser Dependency and Elevated Receivable Days – Coal India Restricted and its subsidiaries accounted for 66.0% of income in 9M FY2026, reflecting a excessive diploma of purchaser dependency. Commerce receivables stood at ₹9,246 million as of December 31, 2025 (~168 receivable days), and the auditor flagged overdue balances from CIL subsidiaries exceeding one yr in every of the final three fiscal years, implying a recurring concern.

- Power Transition Threat – If the power transition from coal accelerates, CIL’s enlargement plans may very well be curtailed, instantly compressing CMPDI’s addressable market.

Outlook

CMPDI occupies a dominant place in India’s mining consultancy. Whereas income dependence on a single authorities group limits pricing autonomy and the long-term trajectory of coal demand introduces uncertainty past the medium time period, the corporate stays structurally poised for progress, with an asset-light, zero-debt mannequin, demonstrating constant margin enlargement, with PAT margins widening from 21.2% in FY23 to 30.6% in FY25.

In accordance with the RHP, the corporate’s listed friends are Engineering India Ltd (EIL) and RITES ltd (RITES). The peer group is buying and selling at a median P/E of twenty-two.6x, with the very best being 25.2x, and the bottom being 19.9x. On the higher value band, the itemizing market capitalization of CMPDI will probably be ₹12,280.8 crore, and the corporate is demanding a P/E of ~18.41x, based mostly on the put up problem market capitalization and FY25 diluted EPS. When in comparison with its friends, the problem appears to be pretty valued. Primarily based on the above views, we offer a ‘Subscribe’ score for this IPO.

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Put up Views:

1,167

")

{kind=link}