AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $140.68 (+2.5%)

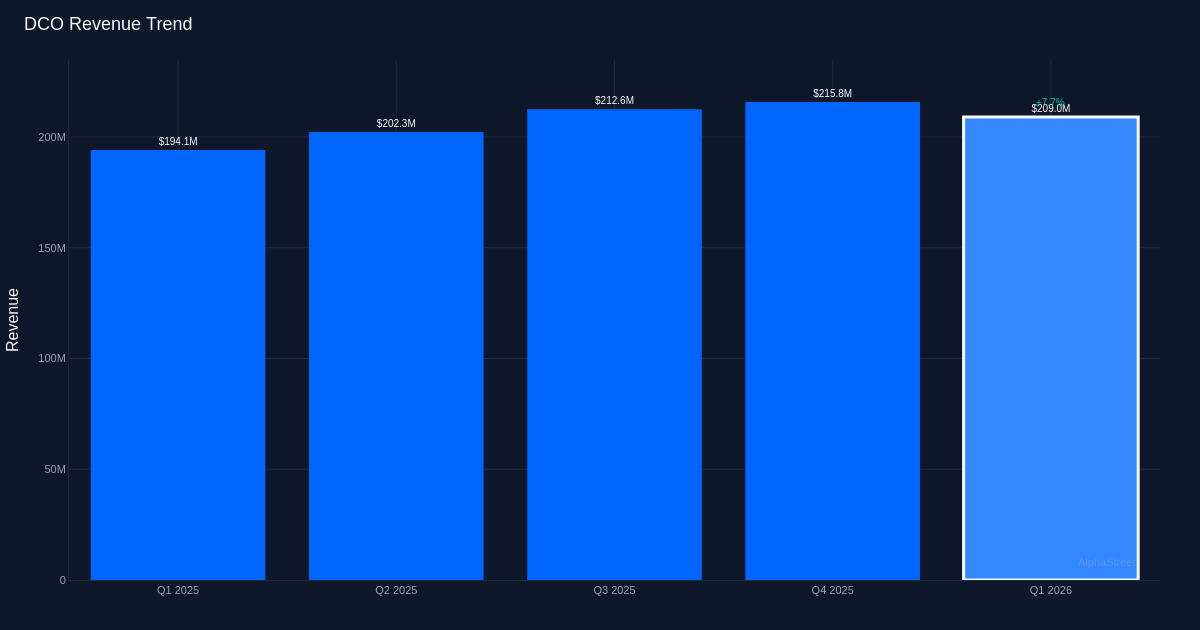

Earnings Miss. Ducommun Integrated (NYSE: DCO) reported Q1 2026 adjusted diluted EPS of $0.75 per share, falling in need of the $0.79 consensus estimate by 5.1%. The aerospace and protection producer generated $209.0M in income for the quarter, representing 9.0% progress from $192.5M in Q1 2025. Adjusted internet earnings reached $11.7M for the quarter, whereas the corporate maintained an adjusted EBITDA margin of 16.9%. Regardless of the bottom-line shortfall, shares traded up 2.5% to $140.68, suggesting buyers discovered encouragement within the top-line momentum and operational efficiency.

Income-Pushed Progress. The earnings miss seems much less regarding when examined by means of the lens of high quality—this was a revenue-driven quarter with strong year-over-year enlargement slightly than a margin compression story. The 9.0% top-line progress demonstrates wholesome underlying demand throughout Ducommun’s aerospace and protection portfolio, a essential distinction for buyers evaluating the sustainability of the enterprise trajectory. The corporate’s adjusted EBITDA margin of 16.9% displays operational self-discipline in a interval of continued funding, notably noteworthy given the difficult aerospace provide chain atmosphere that has pressured friends all through the sector.

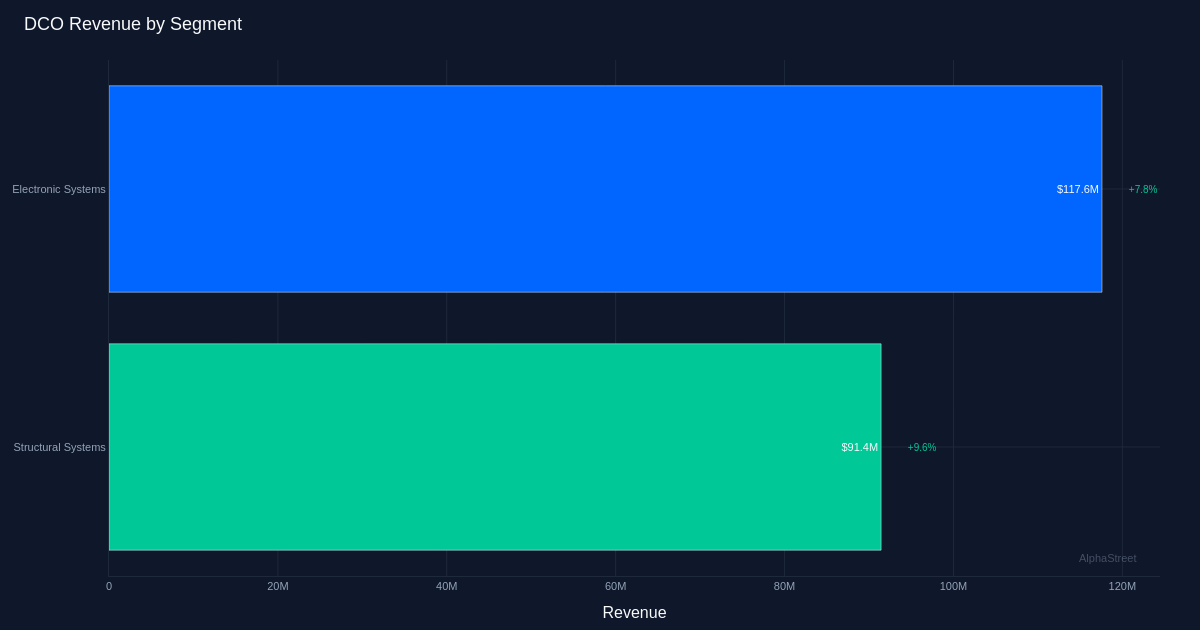

Digital Programs Energy. Digital Programs led efficiency with $117.6M in income, up 7.8% year-over-year, underscoring the phase’s position as the corporate’s progress engine. This division’s resilience speaks to Ducommun’s publicity to high-value digital and structural techniques throughout each business aerospace and protection platforms. The phase’s efficiency is especially related given ongoing protection modernization packages and the continued restoration in business aviation manufacturing charges, each of which ought to present multi-year tailwinds for specialised suppliers like Ducommun.

Backlog Visibility. The corporate maintained $1.07 billion remaining efficiency obligations on a consolidated foundation at quarter-end, offering substantial income visibility as administration works by means of its order e book. This backlog determine serves as a key indicator of near-to-medium time period income potential and displays the long-cycle nature of aerospace and protection contracting. For institutional buyers, this metric provides confidence within the sturdiness of Ducommun’s progress trajectory unbiased of near-term macroeconomic volatility.

Analyst Sentiment. Wall Road maintains a constructive view with consensus scores of 6 purchase, 1 maintain, and 0 promote, suggesting the Road sees by means of the modest earnings miss to deal with the corporate’s strategic positioning and progress prospects. The constructive inventory response following outcomes signifies the market shares this evaluation, viewing the quarter as a validation of operational momentum slightly than a elementary concern.

What to Watch: Monitor how Ducommun converts its substantial backlog into income and margin enlargement by means of the rest of 2026. The corporate’s capacity to execute on its Digital Programs pipeline whereas sustaining EBITDA margins above the mid-teens threshold will decide whether or not the present valuation a number of expands alongside the aerospace sector’s broader restoration.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market info. Human editors confirm content material.