Picture supply: Getty Photos

The Self-Invested Private Pension (SIPP) is a strong weapon in constructing long-term passive earnings. Just like the Shares and Shares ISA, people don’t need to pay a penny in capital good points or dividend tax on their funding returns, giving them extra monetary firepower to develop their wealth.

However that’s not all. With considered one of these merchandise, traders get pleasure from tax aid of between 20% and 45%, relying on their private earnings tax bracket. This may be particularly helpful for individuals who don’t have massive lump sums to speculate, or who can’t make substantial common contributions.

Please observe that tax remedy is determined by the person circumstances of every consumer and could also be topic to alter in future. The content material on this article is offered for data functions solely. It’s not supposed to be, neither does it represent, any type of tax recommendation. Readers are answerable for finishing up their very own due diligence and for acquiring skilled recommendation earlier than making any funding choices.

With on a regular basis residing bills rising, and social care prices rising much more sharply, these monetary merchandise have gotten ever extra necessary. However how a lot passive earnings would somebody want from their private pension to retire comfortably?

£2,661 a month

The reply to this query is determined by every of our particular person circumstances and plans for retirement. However utilizing the UK common laid down by Pensions UK (previously the Pensions and Lifetime Financial savings Affiliation) is an efficient place to start out.

It believes the common single individual wants a complete earnings of £43,900 every year for a snug retirement. That quantities to only beneath £3,659 a month.

With the present State Pension set at £11,973 per 12 months — or £998 a month — that leaves a shortfall of £31,927 that must be made up by a SIPP or different private financial savings or investing product. That’s simply over £2,661 a month.

Producing a pension earnings

There’s a number of methods to make use of a pension to make a second earnings in retirement. These embrace common drawdown, buying an annuity, and shopping for dividend-paying shares.

My very own plan is to purchase high-yield dividend shares. It’s a method that might present me an earnings for all times, in contrast to utilizing a set-percentage drawdown from my retirement pot. And would additionally go away scope for additional portfolio progress over time.

If I purchased 6%-yielding earnings shares right now, I’d want £533,000 in my SIPP to provide me that month-to-month earnings of £2,661.

That’s not small change. However by committing to often investing, over time this aim may be very achievable.

Smashing the goal

One fast and easy manner is by shopping for an exchange-traded fund (ETF) just like the iShares FTSE 250 (LSE:MIDD) product. Holding this specific fund leverages the distinctive progress potential of UK mid-cap progress shares. And with holdings in tons of of various shares spanning a number of industries, it does so in a low-risk manner.

Main holdings right here embrace recovering luxurious good retailer Burberry and monetary providers supplier Aberdeen.

There have been bumps alongside the best way, as — like different equity-based funds — it might probably fall in worth throughout broader inventory market downturns. However the glorious long-term returns communicate for themselves.

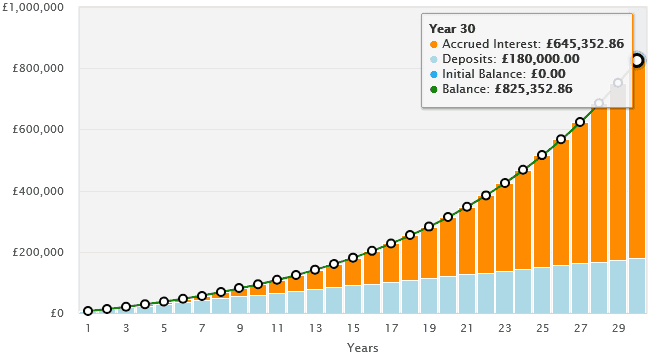

Since its creation in 2004, this FTSE 250 tracker’s offered a mean annual return of 8.5%. If this continues, somebody who invested £500 every month right here in a SIPP (by means of a comination of private contributions and tax aid) would have £825,353 of their pension pot after 30 years.

That’s nicely above our £533,000 goal, and would give loads of flexibility for rising residing and social care prices three a long time from now.

Previous efficiency isn’t any assure of future returns. However historical past exhibits {that a} diversified pension together with funds like this actually can ship a snug retirement.