Picture supply: Getty Pictures

After a tricky 12 months for oil costs, Shell and BP appear like fascinating passive earnings alternatives. However I’m trying outdoors the FTSE 100 in relation to power shares.

Chord Power’s (NASDAQ:CHRD) the biggest unbiased oil producer within the Williston Basin. And it has a special strategy to the massive oil majors.

Investor returns

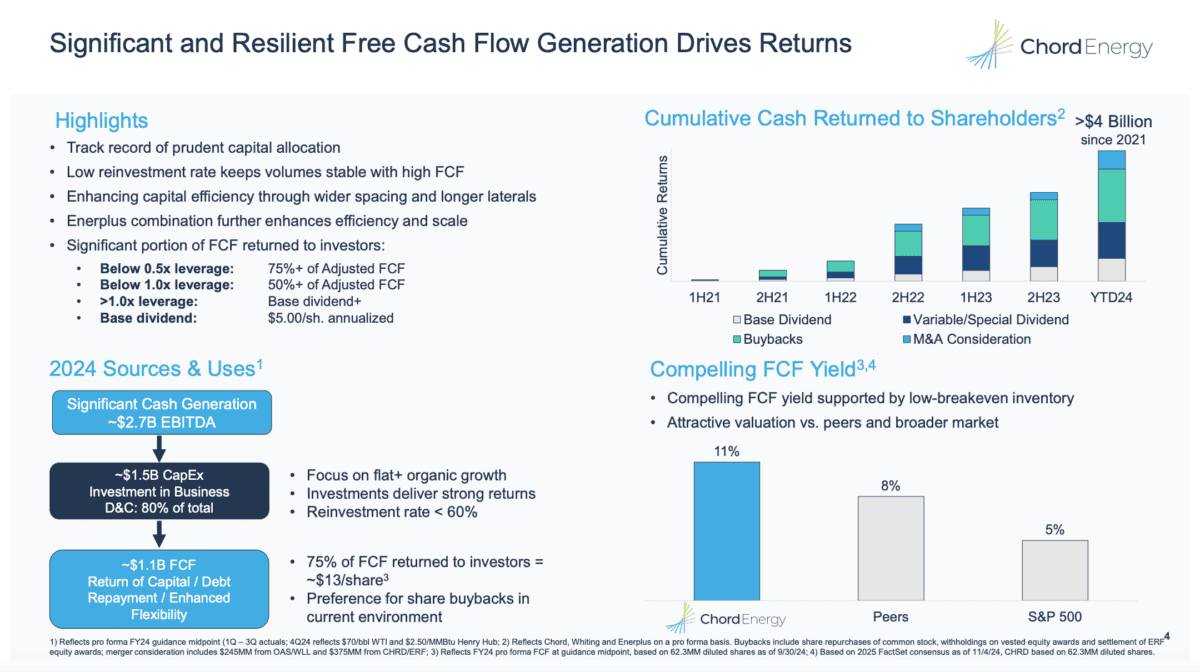

Primarily based on $70 oil costs, the corporate anticipates returning $13 per share to buyers in 2024 by way of dividends and share buybacks. With the share value at the moment at $119, that’s a return of just about 11%.

Supply: Chord Power Q3 Investor Presentation

Traders ought to observe a few dangers although. An identical final result in 2025 is totally not assured – decrease taxes within the US may properly enhance oil provide and this might ship costs decrease.

On high of this, Chord doesn’t specify the break-even value of its belongings in its investor supplies. This makes it tough for buyers to evaluate what the impact of decrease oil costs may be.

This makes it a riskier funding than I normally go in for. However I feel the chance may be distinctive and it’s a threat I’m prepared to take as a part of a diversified portfolio.

What makes Chord completely different?

What makes Chord – doubtlessly – distinctive is it doesn’t make investments closely in exploration initiatives. Not like the likes of ExxonMobil and Chevron, it focuses on returning earnings to shareholders.

The apparent limitation to this technique is that oil wells don’t final endlessly. And after they run out, the corporate wants to search out methods to switch them, in any other case its earnings will dry up.

Moderately than funding speculative initiatives, Chord prefers to do that by buying different companies with established belongings. The newest instance is its $4bn buy of Enerplus in Could.

Rising like this could put the agency’s stability sheet in danger. However the firm’s truly in a really sturdy place, with a leverage ratio round a 3rd of the extent of its friends and a fifth of the S&P 500 common.

UK oil

Each Shell (4.5%) and BP (6.1%) have engaging dividend yields for the time being. And as a UK investor, I’m set to pay a 15% withholding tax on distributions I obtain from Chord.

On high of this, I strongly suspect each the UK oil firms have decrease manufacturing prices. And this provides them a transparent benefit over the agency I’ve been shopping for shares in.

Regardless of this, I feel the upper windfall taxes BP and Shell are going to should cope with subsequent 12 months – and past – is more likely to offset this. These obtained more durable within the Price range and look fairly sturdy to me.

Against this, Chord’s (together with different US firms) more likely to face decrease taxes in 2025. And this could imply its manufacturing prices – no matter they’re – come down.

I’m shopping for

I see Chord as one of many riskiest investments in my Shares and Shares ISA, however I’m nonetheless shopping for step by step. What occurs if oil costs fall is unclear.

From a passive earnings perspective although, I feel the potential reward means the chance’s price it. If oil costs simply keep above $70, that is an funding that would end up extraordinarily properly for me.