In truth, conviction in Patanjali’s inventory has been rising for a number of quarters now. Since June 2023 institutional traders, each home and overseas, have constantly elevated their stakes within the firm, whereas promoters have offloaded shares.

Because the broader FMCG sector recovers amid a revival of rural demand, ought to traders take particular notice of Patanjali Meals?

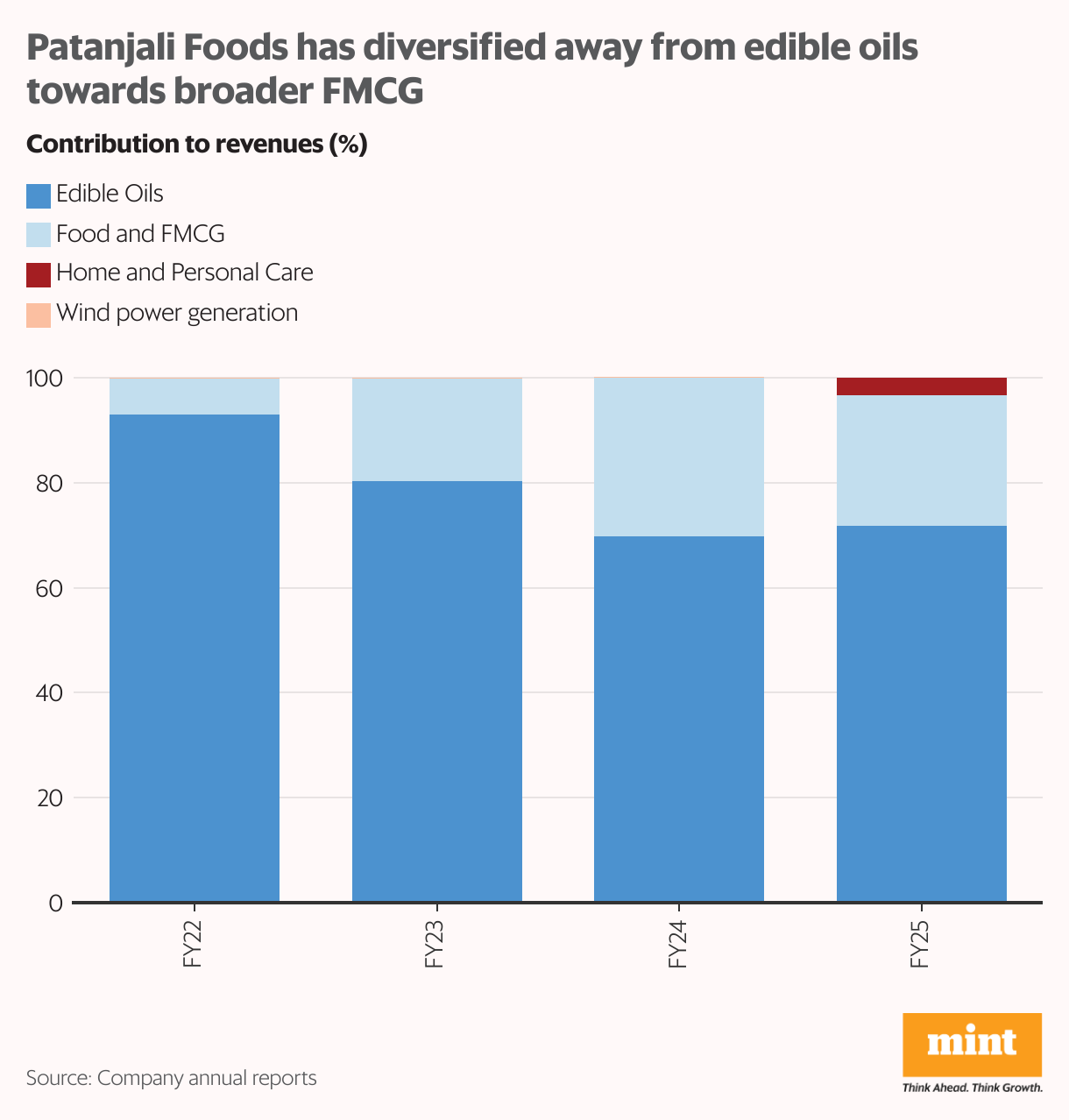

From oil to FMCG

Integrated in 1986, and previously often called Ruchi Soya, Patanjali Meals has positioned itself as a ‘pure’ different to traditional processed meals. It leads the market in palm oil and trails solely Adani Wilmar in soyabean oil. In FY22, 93% of its income got here from edible oils.

Additionally learn: This Murugappa Group inventory is down 38% from its peak. However why are traders turning bullish once more?

However through the years it has strategically diversified into high-margin segments akin to meals and residential & private care (HPC). It acquired the biscuits enterprise in 2021, and the meals line from its guardian Patanjali Ayurved in 2022. Since then, new product launches have helped increase the phase from 6.8% of income in FY22 to 24.8% in FY25.

In the meantime, HPC diversification has been supported by its acquisition of the road from its guardian in July 2024. Edible oils now contribute solely about 70% of income.

Diversification excites traders

Dependence on edible oil had saved the corporate’s high and backside traces weak to fluctuations in oil costs. As an illustration, the corporate’s revenues remained flat in FY24 owing to a drop in oil costs. Provided that India imports greater than 80% of its requirement for crude edible oil, the phase is uncovered to supply-chain shocks from geopolitical conflicts.

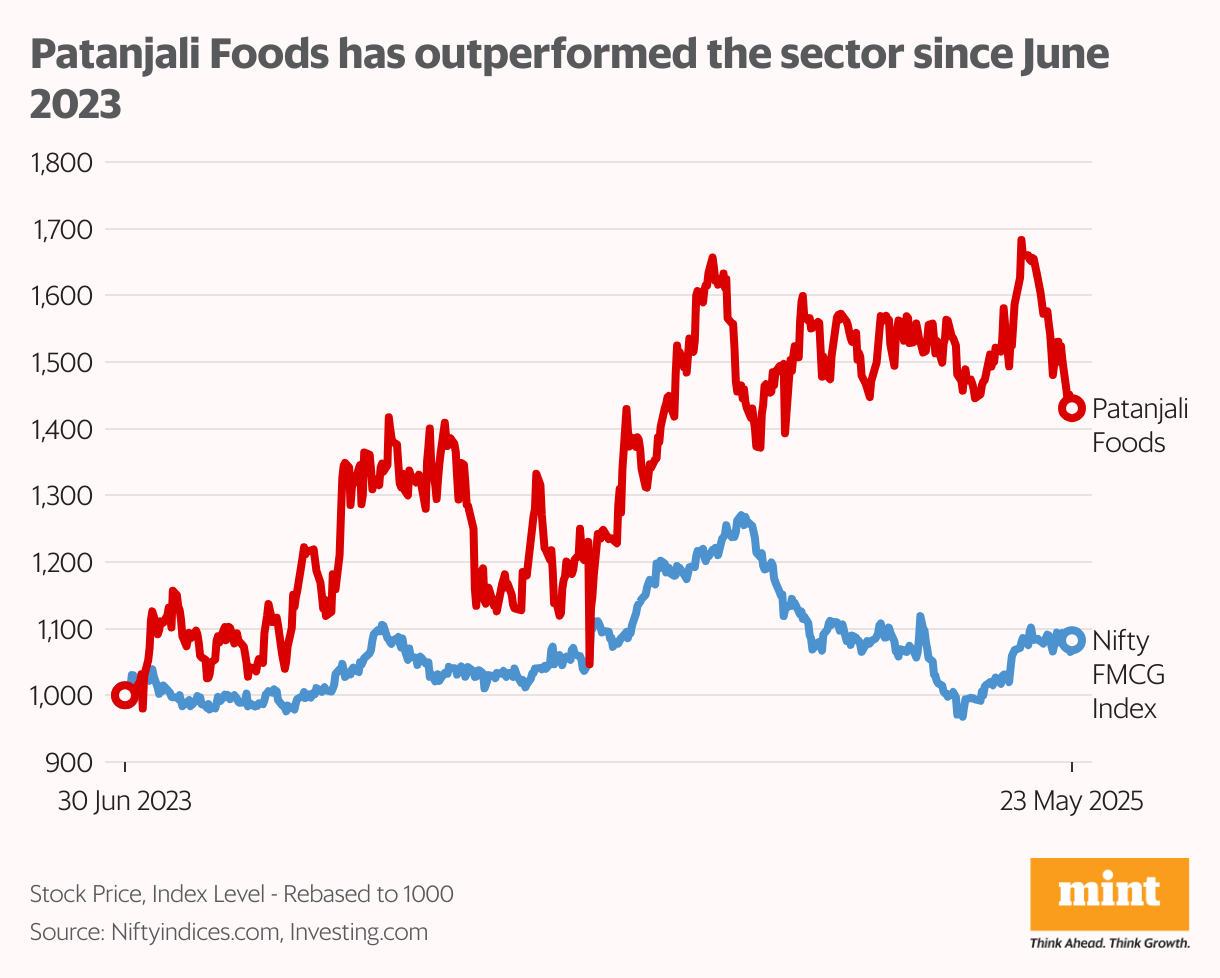

The strategic diversification into the broader FMCG market has thus enthused traders. The inventory has rallied by 20% since June 2023, outperforming the sector’s 4% return through the interval.

Margins had left traders wanting

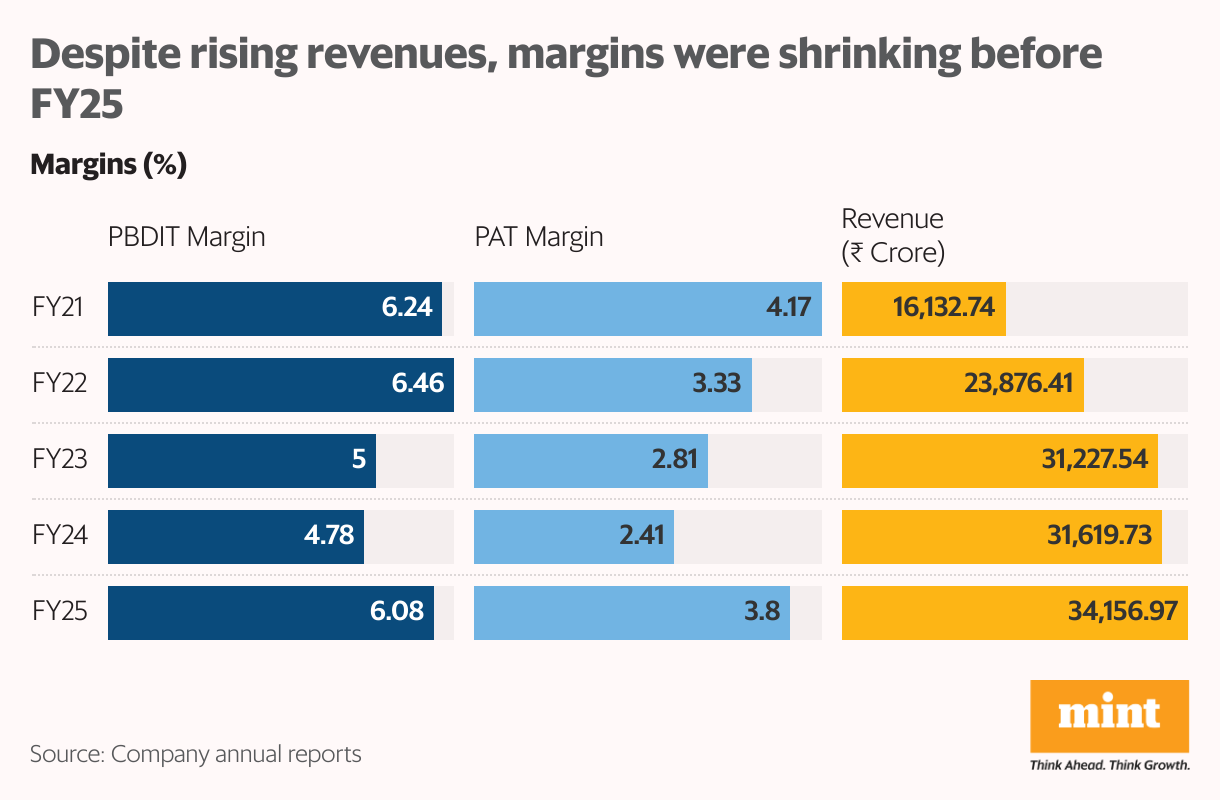

For the reason that firm acquired Ruchi Soya in FY21, its revenues have greater than doubled to nearly ₹35,000 crore. Patanjali Meals is now the nation’s third-largest FMCG participant by income.

The corporate has mass attraction because of its affiliation with yoga guru Baba Ramdev. Its attain has been enhanced additional via its direct distribution channels, comprising greater than one million shops, Patanjali Chikitsalayas and Divya pharmacies. It additionally has about 400 fashionable shops, all whereas sustaining aggressive pricing to cater to the plenty.

The flip facet of this mass attraction is that the corporate’s margins are miniscule – below 5%. Smaller friends akin to Colgate Palmolive boast of margins as excessive as 35%, whereas Patanjali doesn’t even characteristic within the high 5. In truth, its margins have shrunk through the years – from greater than 4% in FY21 to 2.4% in FY24.

Margins improved in FY25

In FY25 the corporate reported 8% development in income, led by 11% development in its mainstay, edible oils. This, together with income from the brand new HPC phase, helped negate the 11% degrowth in meals and FMCG.

The corporate reported phenomenal 70% development in revenue after tax (PAT) through the yr, once more supported by oil. However greater rural demand, the Ebitda margin in meals and FMCG shrank from 12.8% in FY24 to 7.9% in FY25 owing to greater raw-material costs. Ebitda for the phase fell by ₹557 crore – from ₹1,230 crore in FY24 to ₹673 crore in FY25.

However the edible oil and HPC segments supported general profitability. As FY24’s slowdown in edible oil costs gave solution to power in FY25, the phase turned worthwhile. From an Ebitda lack of ₹76 crore in FY24, FY25 noticed a turnaround to revenue of ₹978 crore. The high-margin HPC phase additionally contributed ₹152 crore to working revenue through the yr.

Additionally learn: This multibagger inventory delivered 160x returns in 5 years. What drove the surge?

Patanjali has additionally been slashing its debt. Debt-to-equity shrank from 0.10 to 0.07 in FY25. This helped scale back finance prices by ₹105.5 crore through the yr, additional supporting the underside line.

Margin outlook is promising

The newly acquired HPC line is margin-accretive, because of synergies led to by Patanjali Ayurved’s model fairness together with cost-efficiencies and working leverage. Its full advantages are anticipated to circulate in from FY26.

The phase is concentrated in north and west India, which leaves ample scope for growth within the south, the place the corporate’s distribution community is already robust. In FY26, HPC is predicted to contribute 18% to the corporate’s Ebitda.

Patanjali has additionally been including premium merchandise to its portfolio. Its entry into classes akin to sports activities vitamin, dry fruits, and bathe gels is predicted to spice up margins. These initiatives ought to assist cushion a minimum of a few of the impression of subsequent will increase in uncooked materials costs.

Strategic initiatives are a blended bag

Other than the margin-accretive HPC phase, Patanjali plans to arrange a palm oil mill in Mizoram by the top of the yr. This could complement its 74,000 hectares of land below palm oil cultivation, and additional its backward-integration initiative.

The corporate has additionally entered wind energy era, however this contributes solely 0.1% of income. It has additionally invested within the building and infrastructure firm KBC International. The Patanjali Group has additionally entered common insurance coverage with Magma Common Insurance coverage. Buoyed by such strategic initiatives, the group goals to hit ₹1 trillion in income by 2028.

Model fairness dangers stay

In Could 2024, Patanjali got here below the regulator’s scanner for failing to satisfy meals security requirements. The incident pertained to samples collected in 2019 – earlier than the meals enterprise was introduced below Patanjali Meals.

However this occurred once more in January 2025, when the Meals Security and Requirements Authority of India (FSSAI) ordered the corporate to recall a batch of crimson chilli powder for exceeding the utmost allowed pesticide residue. It has additionally been embroiled in conflicts with the Supreme Court docket relating to its scientifically unverified claims about the advantages of Ayurveda.

Additionally learn: IDFC’s development hits a pace bump. Is the inventory’s bounce-back in danger?

Lastly, whereas Ramdev doesn’t maintain a stake within the firm, he’s the face of the model. Any injury to his status would thus threaten the corporate’s model fairness.

Lofty objectives amid stiff competitors

The corporate goals to faucet exports, make acquisitions, and enter new classes to develop its income to ₹50,000 crore by 2028. This interprets to 14% compound annual development.

Nevertheless, it faces intense competitors within the sector. Whereas Dabur was once the one different model that marketed its merchandise as ‘pure’, different legacy FMCG gamers are actually doing so. The rise in Patanjali’s advertising spends because it appears to be like to retain market share might hit its already slim margins.

Analysts count on the corporate’s income to develop at solely about 9% yearly. Its goal value has been pegged at ₹2,100, reflecting 24% upside from present ranges. However near-term headwinds might trigger volatility within the inventory, which may very well be exacerbated by its current inclusion below futures and choices (F&O) contracts.

For extra such evaluation, learn Revenue Pulse.

Ananya Roy is the founding father of Credibull Capital, a Sebi-registered funding adviser. X: @ananyaroycfa

Disclosure: The writer doesn’t maintain any shares of the businesses mentioned. The views expressed are for informational functions solely and shouldn’t be thought-about funding recommendation. Readers are inspired to conduct their very own analysis and seek the advice of a monetary skilled earlier than making any funding selections.