Picture supply: Getty Pictures

Not too long ago, analysts from a number of banks have voiced considerations a couple of short-term inventory market correction, together with Deutsche Financial institution, Morgan Stanley and Societe Generale. Whereas expectations differ, some recommend a fall of as a lot as 15% – or extra.

No person actually is aware of what may occur however it pays to be ready. And looking out on the market, I can perceive their warning.

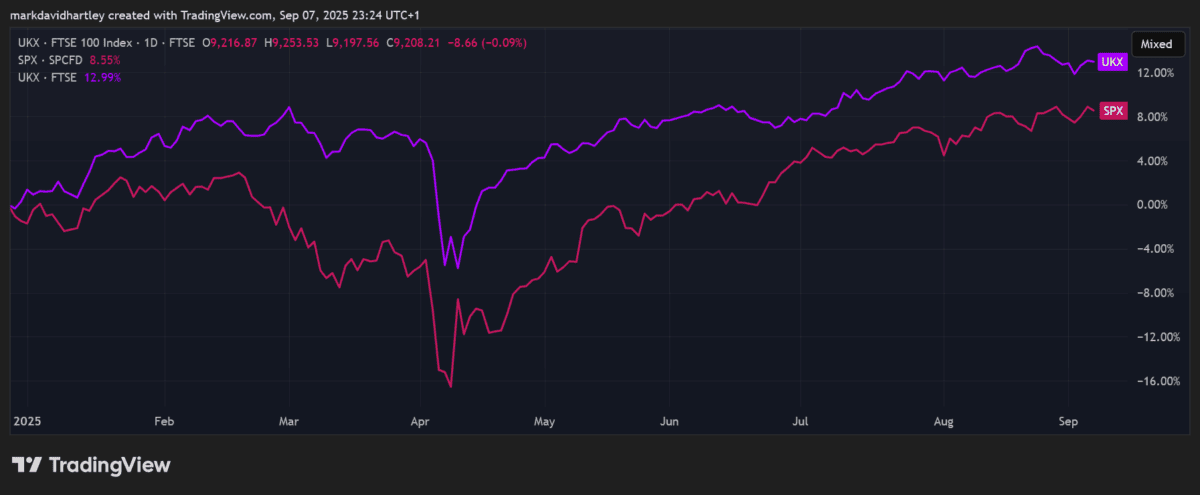

The S&P 500 hasn’t had the strongest 12 months, but valuations nonetheless look stretched following final 12 months’s rally. The index is buying and selling on a price-to-earnings (P/E) ratio of 27, far greater than its long-term historic common of 16.

The FTSE 100‘s in an identical place. It’s up 12.99% 12 months to this point, in contrast with 6.7% at this level final 12 months. The P/E ratio sits at 19.7, greater than its three-year common of 15.7.

Why are consultants anxious?

Issues vary from commerce tariffs to financial weak spot and stretched valuations. With tariff prices prone to be handed onto shoppers, the concern is that family spending will sluggish. That might drag down earnings throughout a number of industries, placing stress on fairness markets that already seem costly.

When a market correction seems potential, some buyers select to carry a money pile. The concept’s easy — look forward to the autumn after which purchase at cheaper ranges. I like this technique however I additionally suppose it’s price remembering that not all shares decline throughout downturns.

Some defensive firms, significantly in retail, prescription drugs and utilities, have a tendency to carry up higher. Tesco and Nationwide Grid are two traditional examples. Achieved appropriately, a well-balanced defensive portfolio of shares may even ship stronger returns than the common Money ISA.

One inventory I like

For my very own portfolio, AstraZeneca‘s (LSE: AZN) a core defensive holding. It’s the biggest firm on the FTSE 100 and has constructed a popularity for reliable income and earnings. Over the previous decade, it’s delivered annualised returns of 11.24% — spectacular consistency for a enterprise of its measurement.

Latest efficiency has been clouded by weaker vaccine gross sales as soon as pandemic demand fell away. Revenues dipped in late 2022 and thru 2023 because of this. Nonetheless, stripping out Covid-19 merchandise, the enterprise has continued to develop strongly. Core income rose 17% in 2022 and 15% in 2023, exhibiting its underlying power.

In fact, there are nonetheless dangers. Commerce tariffs may impression world operations and provide chain disruptions are all the time a priority for a corporation with such huge attain. Administration’s already introduced plans to take a position $50bn in US manufacturing by 2030 to assist scale back publicity, although this will probably be expensive and there’s no assure it is going to ship the specified advantages.

However from a defensive viewpoint, its valuation seems cheap, with a ahead P/E ratio of 17.8. Equally, profitability and margins are first rate for the business, with a return on fairness (ROE) of 20%.

Ultimate ideas

A possible 15% inventory market correction could sound alarming however historical past reveals they’re pretty widespread. My method is to maintain some money readily available whereas additionally guaranteeing my portfolio has adequate defensive protection.

With a strong stability sheet supported by wholesome money stream and manageable debt, AstraZeneca stays certainly one of my favourites. For buyers trying to scale back threat throughout a downturn, I believe it’s a inventory properly price contemplating.

Казино Pokerdom слот Black Booze