Insights")

Lloyds Metals & Vitality Ltd – Empowering India’s Infrastructure

Integrated in 1977 and headquartered in Mumbai, Lloyds Metals & Vitality Ltd (LMEL) is a key participant within the metals and mining business engaged in mining of iron ore, manufacturing of sponge iron and producing energy. The corporate is current throughout the worth chain of metal manufacturing, from iron ore mining to Direct Lowered Iron (DRI) manufacturing and is additional ahead integrating into metal manufacturing. The corporate has strategically positioned iron ore at Surjagarh in Gadchiroli district of Maharashtra which has a ten MMTPA iron ore capability. It has manufacturing amenities in Ghughus in Chandrapur district and in Konsari in Gadchiroli district of Maharashtra, with a mixed manufacturing capability of 0.34 MMT and 34 MWh of energy era.

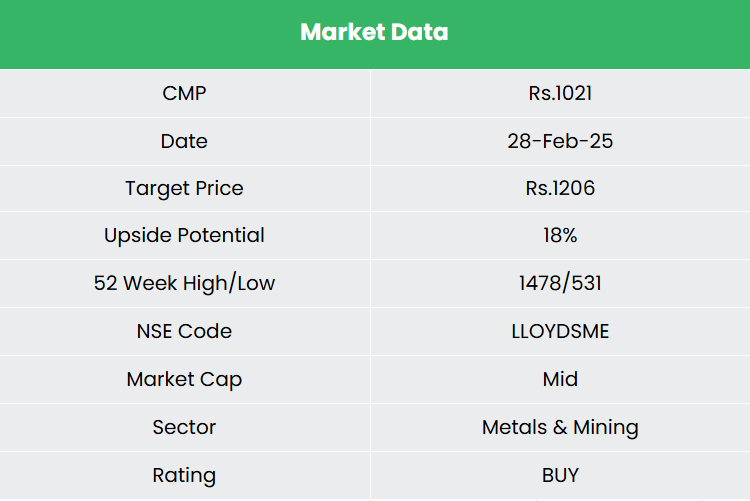

Lloyds Metals & Vitality Ltd (LMEL), with a focused upside potential of 18% is likely one of the few metal firms which have development and enlargement plans on nearly no debt leverage.

Merchandise and Companies

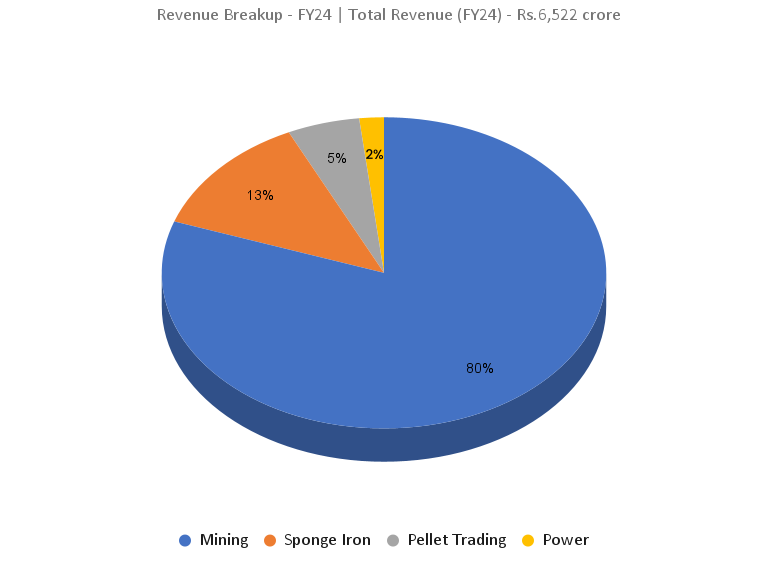

The corporate’s key enterprise segments embrace iron ore mining, DRI, captive energy and pellet buying and selling.

Subsidiaries: As of FY24, the corporate has 3 subsidiaries and no affiliate firms/joint ventures.

Funding Rationale

- Progress methods – The corporate has set a strategic purpose to develop into a sustained value-added metal producer, with plans to realize a wire-rod manufacturing capability of 1.2 million tonnes and an HR coils manufacturing capability of three million tonnes every year, all with out counting on debt leverage. This method is predicted to reinforce the corporate’s resilience, even throughout cyclical slowdowns. With focused investments in metal property, the corporate is on observe to develop into India’s most cost-efficient metal producer. Moreover, the corporate has acquired roughly an 83% stake in Thriveni Earthmovers Non-public Ltd, certainly one of India’s largest mining improvement operators (MDO), for a transaction worth of Rs.70 crore. This acquisition is predicted to ship per tonne financial savings of Rs.400-500 on iron ore, on a consolidated foundation.

- Enlargement plans – The corporate is setting up India’s longest slurry pipelines, with a 85 km pipeline to the Konsari plant and a 190 km pipeline to the Chandrapur plant from its mines. These pipelines are anticipated to cut back freight prices by Rs.500-600 per tonne for the 85 km pipeline and Rs.800-1,000 per tonne for the 190 km pipeline. LMEL can be establishing a mineral-based metal plant at Konsari, Gadchiroli district, with a capability of 72,000 MTPA for DRI manufacturing. Moreover, the corporate is establishing a 12 MNT pellet plant, a 1.2 MNT Wire Rod Mill (WRM) facility, and a 3 MNT built-in metal plant. To make sure captive logistics, the corporate can be investing in a fleet of vehicles, transferring away from reliance on third-party logistics.

- Q3FY25 – Throughout Q3FY25, the corporate reported income of Rs.1,693 crore, a de-growth of 12% as in comparison with the Rs.1,924 crore of Q3FY24. EBITDA elevated by 20% from Rs.461 crore of Q3FY24 to Rs.555 crore of the present quarter. Internet revenue elevated from Rs.332 crore of Q3FY24 to Rs.389 crore of Q3FY25, a development of 17% YoY. EBITDA margin improved from 24% to 33% and internet revenue margin elevated from 17% to 23% YoY.

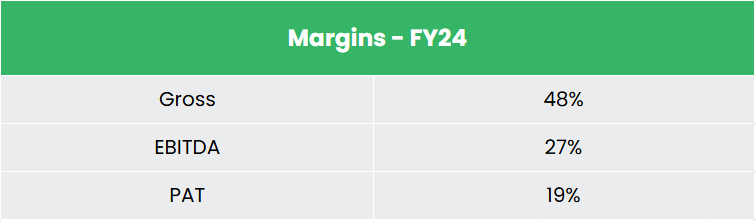

- FY24 – Supported by larger iron ore volumes, the corporate generated income of Rs.6,522 crore, a rise of 92% in comparison with FY23 income. Working revenue is at Rs.1,781 crore, up by 101% YoY. The corporate posted internet revenue of Rs.1,243 crore, towards loss reported in FY23.

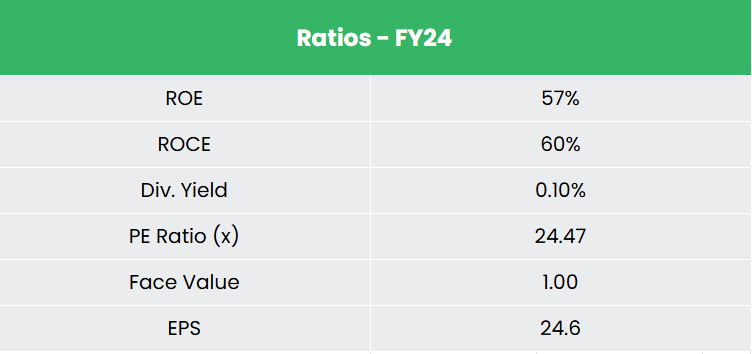

- Monetary Efficiency – The corporate has generated income and internet revenue CAGR of 196% and 2014% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 65% every for FY21-24 interval. The corporate has a debt-to-equity ratio of 0.01.

Trade

The mining business has the potential to considerably enhance GDP development, international change earnings, and supply a aggressive benefit to end-use industries resembling building, infrastructure, automotive, and energy by securing key uncooked supplies at aggressive costs. As the federal government’s emphasis on infrastructure improvement intensifies, the demand for iron and metal is predicted to rise, pushed by the rising building of roads, railways, airports, and extra. India is the world’s second-largest producer of crude metal and the fourth-largest producer of iron ore, in addition to the most important producer of sponge iron (DRI). These elements are anticipated to drive future demand for each metal and iron ore.

Progress Drivers

- 100% FDI by way of computerized route within the mining sector.

- Minerals are valuable pure assets that function important uncooked supplies for basic industries, so the expansion of the mining business is important for the general industrial improvement of a nation.

- Indian authorities’s initiatives and schemes resembling Gati Shakti Grasp Plan, Make in India, Pradhan Mantri Awas Yojna – Housing for all, City Infrastructure improvement scheme for small and medium cities is predicted to foster the expansion of Metals and Mining sector in India within the subsequent few years.

Peer Evaluation

Opponents: NMDC Ltd, Gujarat Mineral Improvement Company Ltd (GMDC), and many others.

In comparison with its rivals, the corporate has larger profitability ratios and higher income & revenue development, indicating the corporate’s monetary stability and its effectivity in producing revenue and returns from the invested capital.

Outlook

The Surjagarh Iron Ore Mine is strategically located within the coronary heart of India, making it centrally positioned and equidistant from most metal crops throughout the nation. The partnership with Thriveni is predicted to reinforce operational capabilities, cut back prices, develop the corporate’s presence in key mining areas, and strengthen its order guide. Mining output from the location is projected to develop from 10 MMTPA to 25 MMTPA. That is anticipated to generate important income and revenue for the corporate, with projected cumulative revenues of roughly Rs.27,000 crore and an EBITDA of Rs.9,000 crore over the subsequent three years (FY26-28). The corporate is planning a Rs.33,000 crore capital expenditure for its enlargement initiatives.

Valuation

We consider LMEL’s enterprise plans are set to scale operations and obtain operational excellence, positioning the corporate as a low-cost, high-efficiency key participant within the metal and mining industries. We suggest a BUY score within the inventory with the goal worth (TP) of Rs.1,206, 27x FY26E EPS.

Threat

- ESG threat – The corporate is topic to the inherent ESG threat the mining sector is uncovered to. The administration should be cautious of any threat that will have an effect on their means to boost capital, acquire permits, work with communities & regulators.

- Focus threat – The corporate has coal mine solely at a single location exposing it to larger volatility and potential losses if something negatively impacts the only operational location.

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM on no account assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles it’s possible you’ll like

Put up Views:

100