Regardless of commanding 41.5% of the home market and accounting for 43% of the nation’s automotive exports, Maruti is struggling to take care of its market dominance. Strategic missteps and altering client preferences have put its place in danger.

The corporate was late to capitalize on the electic car (EV) megatrend and the rising premiumization wave pushed by utility autos. It additionally exited the fast-growing diesel phase. Whereas Maruti nonetheless instructions over 70% share within the small automotive phase, the general pie has shrunk, with volumes falling by 60% between FY18 and FY24.

Learn this | At Maruti Suzuki, small vehicles are again within the driver’s seat

Outcome? It has ceded floor, with its market-share eroding considerably from 52% in 2019 to only about 41% now.

Over the previous 5 years, Maruti’s inventory has grown at a CAGR of 18%, properly beneath the sector’s 32%. The corporate has seen its home budget-car gross sales undercut by sluggish city demand, rising commodity costs, and an sudden ₹2,966 crore IT evaluation order, compounding its woes.

However regardless of these hurdles, Maruti Suzuki is refocusing its technique on premiumization and sustainable mobility. The query is whether or not this pivot will allow it to reclaim misplaced floor.

Let’s discover.

Sluggish city demand hurts Maruti

In FY25, sluggish city demand resulted in muted home gross sales of vehicles. Maruti offered 2.2 million vehicles through the yr, an uptick of simply 4.6% over the earlier fiscal. Value hikes and enhancing product combine led to barely higher income progress at 7.5%.

FY25 noticed buoyant export-growth of 17.5% over FY24. However since exports contribute solely about 15% to Maruti’s volumes, total progress for the yr remained mellow.

Finances vehicles have bludgeoned progress

A bulk of Maruti’s gross sales come from funds vehicles. This primarily includes the mini phase with fashions akin to Alto and S-Presso, and the compact phase which incorporates vehicles like Baleno and WagonR. Collectively, they constituted nearly half of Maruti’s gross sales in FY25.

Pressured actual wage-growth amongst city plenty led to slower upgrades from two-wheelers to small vehicles, a problem compounded by regulatory pressures and commodity costs which saved the price of possession excessive. The mini phase noticed 11% decrease gross sales in FY25, whereas the compact phase noticed 7% de-growth.

After all, utility autos akin to Brezza and Ertiga, noticed 12% greater gross sales in FY25 and supported progress. The administration insisted that SUV progress is in step with the long-term pattern, and it’s funds vehicles which have struggled underneath persistent stress on the decrease finish of the consumption pyramid.

Learn this | Chopping taxes on small vehicles is a fast repair that ignores the elephant within the room

It has despatched out a call-to-action to the regulators, drawing their consideration in the direction of the necessity for preferential rules to assist funds vehicles.

Margins underneath stress

Muted quantity progress has hampered Maruti’s working leverage, shrinking margins. As well as, sluggish demand has pressured the corporate to extend reductions and promoting spend.

At its greenfield plant in Kharkhoda, rising depreciation and overhead prices have added additional pressure. Key enter prices, together with aluminum, zinc, and rubber, additionally surged in FY25.

Maruti has additionally ventured into the EV market with the e-Vitara, anticipated to start gross sales in H2 FY26. The corporate plans to provide 70,000 models of the EV this yr, although the phase will probably stay margin-dilutive amid competitors till it features scale, regardless of authorities subsidies.

The auto business has responded to rising prices by passing on a number of the ache to customers by means of worth hikes early this yr. Maruti was no exception. However, greater materials and worker prices led to shrinking margins over the yr. Working Ebit for the newest quarter noticed a 14% decline, whereas revenue slipped by greater than 4% to ₹3,711 crore.

A combined outlook for close to to medium time period

Society of Indian Car Producers (SIAM) has penciled in even slower progress of home automotive gross sales at 1-2% in FY26. After all, Maruti is aiming for 20% progress in exports to counterbalance the muted home demand.

As for margins, commodity costs have eased just lately amid the brewing trade-war between the US and China. Whereas this could have helped take the strain off margins for auto makers, the pattern stands to reverse as the 2 largest economies transfer in the direction of a truce. The influence could possibly be negated to an extent by means of an enhancing product-mix and price-hikes. Earlier this month, Maruti introduced the third spherical of price-hikes this yr, amounting to as a lot as 4%.

The opposite facet of the coin is {that a} truce would stop additional hits to world financial progress, which bodes properly for the automotive maker. Furthermore, on condition that Maruti’s export-destinations are concentrated in Latin America, Africa, and Southeast Asia, which wouldn’t have in-house vehicle manufacturing capability, the administration has indicated low threat from tariffs.

Lengthy-term outlook promising

Maruti Suzuki has huge plans for the long run.

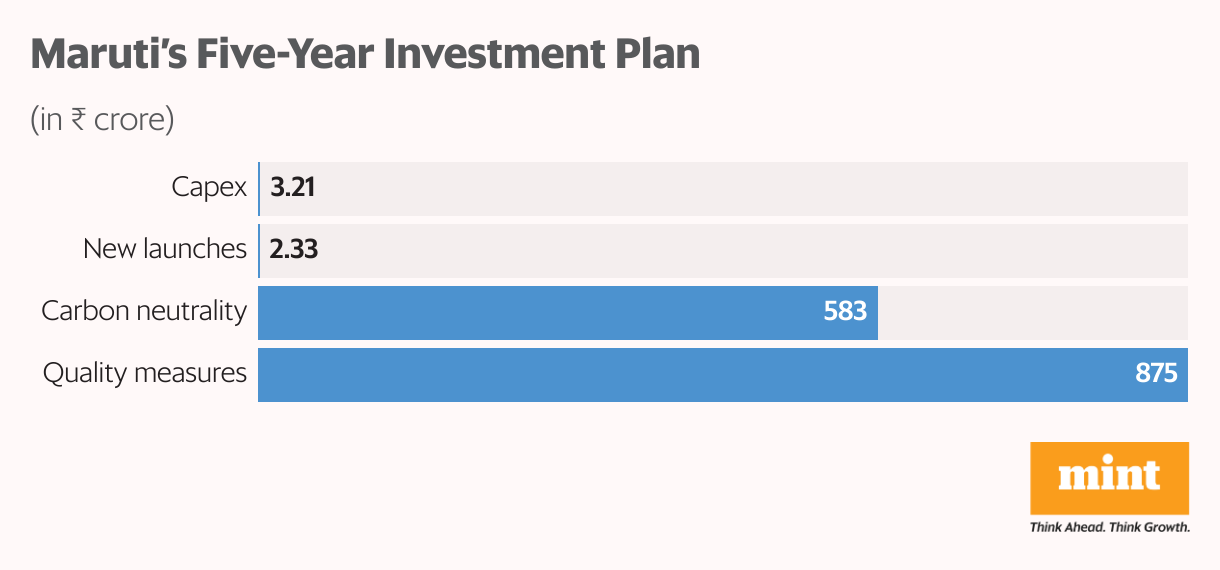

By FY30, it plans to take a position ₹7,000 crore in the direction of aggressive capex and new mannequin launches, together with within the new and glossy EV and hybrid areas. It has manufacturing services in Gurugram and Manesar with a mixed annual capability of 1.5 million models. That is anticipated to be ramped as much as 4 million models by FY30. 2 new ICE SUVs are slated for launch this fiscal, and the brand new e-Vitara electrical SUV can also be set to hit the markets within the second half.

The administration goals to reclaim 50% market-share by focusing on gross sales of two.5 million models by FY30, indicating 12% CAGR progress through the interval. Notably, it plans to launch six new electrical vehicles, and 75% of the gross sales in FY30 are anticipated to return from EVs, hybrids, and CNG autos.

Maruti’s EVs are constructed on a high-spec platform designed particularly for electrical use, not like retrofitted ICE fashions launched by some opponents. This permits for higher specs, which together with the affordable worth proposition, place Maruti’s EVs at a aggressive benefit over world EVs. The group is focusing on the inexpensive EV phase in Europe, and Maruti Suzuki is anticipated to emerge as the worldwide EV export hub.

Additionally learn | Backed by giants, bleeding money—is Ather Power prepared for IPO?

Whereas sustainable mobility can dilute margin over the medium-term, authorities incentives akin to home tax-relief for small hybrid vehicles and import-duties on Chinese language vehicles and parts, ought to supply assist. The shifting product-mix in the direction of utility autos, CNG autos, and exports can also be anticipated to be margin-accretive. Finances vehicles also needs to see a turnaround from the subsequent fiscal, driving volume-growth and working leverage.

Maruti inventory technicals

The automotive maker’s inventory has remained rangebound for greater than a yr now, swinging between Rs10,750 and ₹13,000 apiece. Barring a short-lived spurt seen in February, the inventory has confronted stiff resistance at Rs11,900. That is additionally the extent from which the counter backtracked by 2% after the newest earnings have been introduced.

If the sentiment weakens additional hereon, the inventory might discover assist at round ₹11,325 and once more at ₹10,750.

For extra such analyses, learn Revenue Pulse.

However the long-term elementary outlook guarantees potential, and the inventory is buying and selling at 25.4 occasions its earnings – a big low cost to its long-term common. Analysts peg the inventory’s goal worth at Rs14,000 apiece, reflecting 20% upside from present ranges.

Ananya Roy is the founding father of Credibull Capital, a SEBI-registered funding adviser. X: @ananyaroycfa

Disclosure: The creator holds shares of the businesses mentioned right here. The views expressed are for informational functions solely and shouldn’t be thought-about funding recommendation. Readers are inspired to conduct their very own analysis and seek the advice of a monetary skilled earlier than making any funding selections.