Picture supply: Getty Photos

Attaining monetary freedom with an ISA is a laudable purpose. Nonetheless, acquiring a yearly passive earnings of £18,000 in retirement will probably be difficult for many as a result of they don’t maximise the chance of getting their hard-earned cash to work for them.

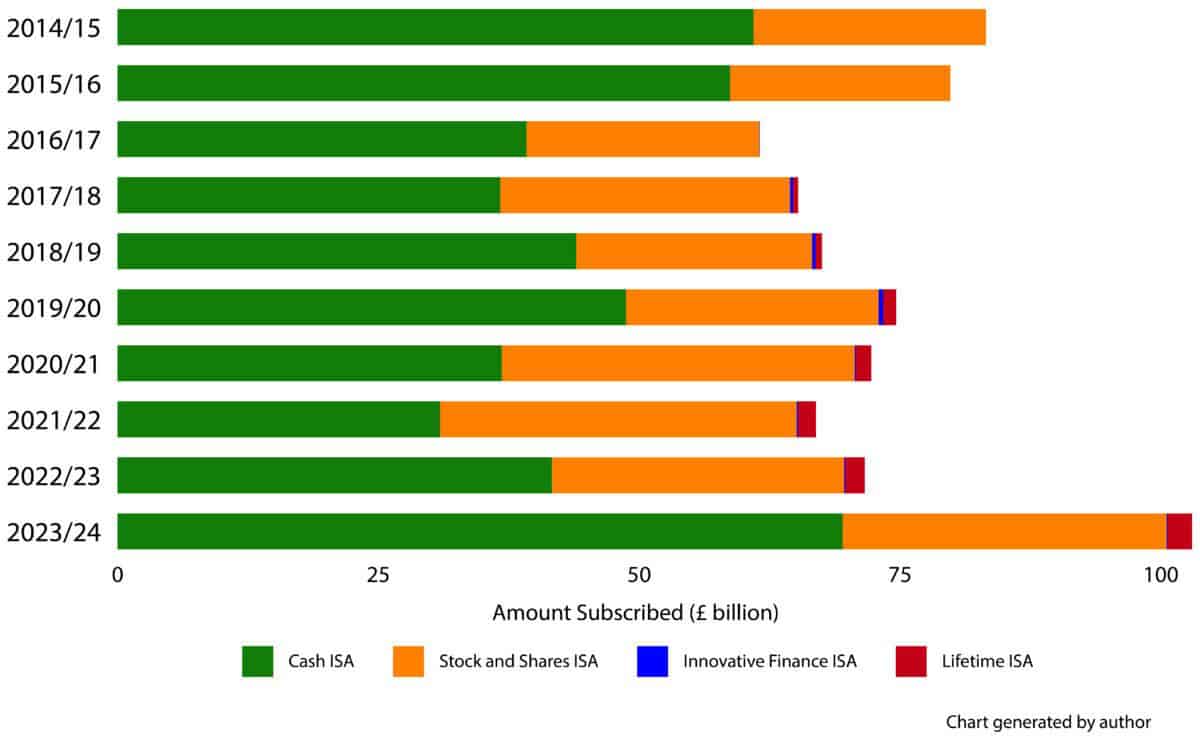

Money ISAs are king

Within the final monetary 12 months, for each new Shares and Shares ISA opened, an equal of two.42 Money ISAs was opened. Much more starkly, of a complete ISA financial savings market of £103bn, over two-thirds are stashed in Money ISAs. The complete breakdown is proven within the chart beneath.

Information supply: HMRC

For my part, this weighting is skewed incorrectly. Right this moment, the common Money ISA yields about 4%. However, over the long run, the FTSE 100 has generated common annualised returns of 6.5% and the S&P 500, 10.5%.

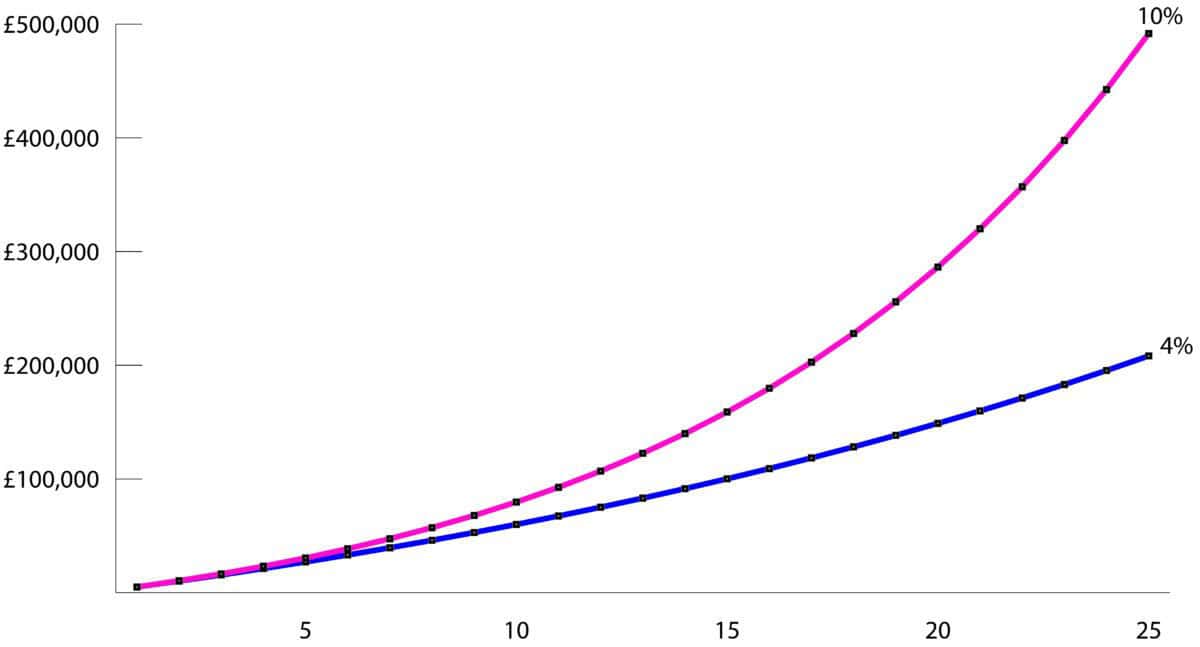

Compounding positive aspects

A person on the lookout for a second earnings of £1,500 a month at retirement might want to have accrued an ISA pot price £450,000. However due to the magic of compounding, small modifications in annual share returns add as much as large variations when measured over many years.

The next chart plots a yearly ISA contribution of £5,000 for 25 years attracting completely different annual returns. A ten% return would get comfortably to the goal. However a 4% return would take 39 years – approach past the parameters of the graph.

Chart generated by creator

Inventory choosing

Attaining a ten% return for 25 years is undoubtedly no imply feat. However for somebody prepared to put money into particular person shares, it’s a sensible goal.

For the reason that flip of the millennium, many FTSE 100 shares have been multi-baggers. These embody Unilever, Related British Meals, Diageo, Bunzl, and Rolls-Royce. As Warren Buffett as soon as mentioned: “let your winners run”. They may nearly definitely comfortably outrun your duds.

Exterior of luck, one is barely ever prone to establish a handful of such shares throughout an investing lifetime. That is the place dividend shares can actually assist supercharge a portfolio.

Dividend performs

Not all high-yielding shares are created equal. I primarily search for a strong monitor document of elevating dividends. Take pension and life insurer Phoenix (LSE: PHNX). Over the previous 10 years, the dividend has been raised by 32%. Right this moment, it yields a whopping 8.4%.

Each the sustainability of its dividend and future will increase are tied to 3 monetary metrics. Firstly, and most significantly, working capital era (OCG). At H1 2025, OCG stood at £705m. Of that quantity, £274m was paid out in dividends.

Secondly, solvency protection ratio. At the moment at 175%, this signifies a powerful stability sheet with loads of choices for capital funding. Lastly, distributable reserves of the corporate are extraordinarily wholesome at £5.5bn, up 20% on 2024.

In fact, there are dangers right here. An ongoing problem for the enterprise is sustained outflows from its varied funds, notably these regarding pension financial savings. In a extremely aggressive trade, this might put strain on future margins.

However zooming out to absorb the larger image, there’s a lot to love concerning the enterprise. On high of ageing demographics, a shift to outlined contribution office pension schemes has resulted in people taking an rising curiosity in making certain they’re saving adequately for retirement. For these looking for passive earnings, it’s definitely a inventory to contemplate.