Photo voltaic Industries India Ltd. – Energy to Propel the Future

Photo voltaic Industries India Restricted, integrated in 1995 and headquartered in Nagpur, Maharashtra, is an explosives and defence ammunition producer working throughout industrial and defence explosives, serving end-markets in mining, infrastructure, building, and nationwide safety. Its product portfolio spans packaged and bulk explosives, detonators, initiating techniques, excessive power supplies, propellants, superior ammunition, loitering munitions, and space-sector energetics. Photo voltaic has a business presence in 90+ nations with manufacturing operations throughout 40+ amenities in 9 nations. The corporate ranks among the many prime 5 international explosives producers and employs 2,403 everlasting staff on a standalone foundation as of FY2025. As of Q3FY26, the order ebook stood at ~Rs.21,000 crore.

Merchandise and Companies

The corporate’s product portfolio contains packaged explosives, high-energy supplies, detonators, solid boosters, detonating cords and twine relays, together with defence merchandise comparable to loitering munitions, ammunition, rocket integration techniques, next-generation mines, missiles, UAV pyrotechnics and fuzes, propellants and warheads, counter-drone techniques, and space-related functions.

Subsidiaries – As of FY25, the corporate has 36 subsidiaries and three affiliate firms.

Funding Rationale

- Defence Enterprise Rising because the Key Progress Driver – The corporate is more and more transitioning from a standard industrial explosives producer to a defence-focused manufacturing firm, which is predicted to drive the subsequent leg of progress. The defence phase recorded a 72% YoY progress, supported by rising home procurement and export alternatives. The corporate at the moment has its highest-ever order ebook of ~Rs.21,000 crore, of which ~Rs.18,000 crore is from defence, offering robust medium-term income visibility. Administration has guided for ~Rs.3,000 crore income from defence, supported by capability additions and new product introductions. Key progress triggers embody the business manufacturing of 155 mm calibre ammunition anticipated from This autumn and ramp-up in provides for the Pinaka Multi Barrel Rocket Launcher programme (anticipated from This autumn). The inauguration of the medium calibre shell manufacturing facility additional strengthens its ammunition capabilities. With growing participation in rockets, ammunition, and defence explosives, Photo voltaic is steadily transferring up the defence worth chain, which might assist increased margins and stronger earnings visibility over the medium time period.

- Rising Export Contribution and World Capability Enlargement – Photo voltaic’s worldwide enterprise continues to scale up, with abroad income crossing Rs.1,000 crore, reflecting rising demand for explosives and defence merchandise in international markets. The corporate is increasing its international footprint by ramping up operations in present worldwide amenities, which has helped convert sure beforehand loss-making items into worthwhile operations. Administration can be evaluating alternatives to enter new markets comparable to Australia, Kazakhstan and Saudi Arabia, which might additional strengthen export contribution. Domestically, the corporate is enterprise important capability enlargement by new amenities in Dhule (Maharashtra) and Dholpur (Rajasthan), supported by ~Rs.2,500 crore capex deliberate for FY26, most of which has already been deployed. As well as, the Rs.12,700 crore MoU with the Authorities of Maharashtra displays long-term plans to scale defence and aerospace manufacturing capability. Whereas it is a long-term funding slightly than fast income addition, it highlights the corporate’s technique to construct large-scale manufacturing capabilities to assist defence exports and international demand, strengthening its long-term progress outlook.

- Q3FY26 – Through the quarter, the corporate reported income of Rs.2,548 crore, up 29% YoY from Rs.1,973 crore in Q3FY25, pushed by robust progress in defence (up 72% YoY) and worldwide segments. EBITDA grew 37% YoY to Rs.733 crore, with EBITDA margin increasing 160bps YoY to twenty-eight.8%. Internet revenue stood at Rs.467 crore, up 38% YoY from Rs.338 crore in Q3FY25, with PAT margin enhancing 120bps to 18.3%.

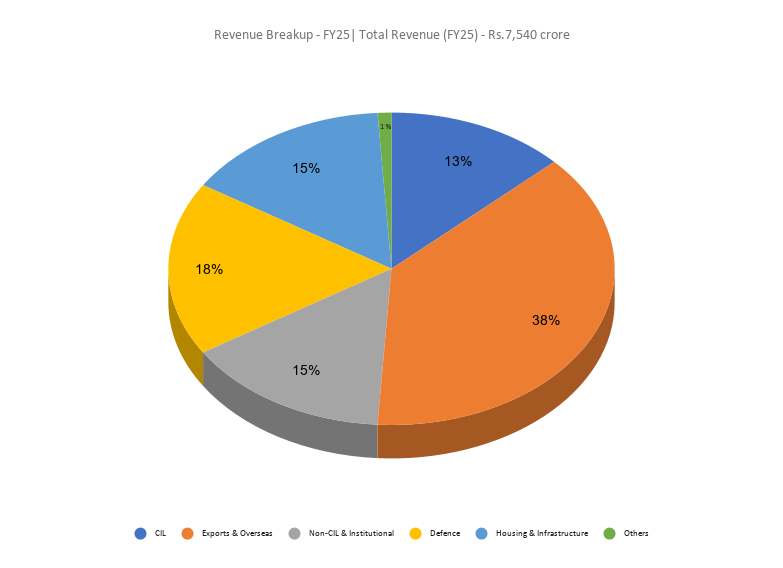

- FY25 – Throughout FY25, the corporate reported consolidated income of Rs.7,540 crore, representing a ~24% YoY enhance from Rs.6,070 crore in FY24. EBITDA grew 44% YoY to Rs.2,031 crore. Revenue after tax stood at Rs.1,288 crore, up 47% YoY from Rs.875 crore in FY24.

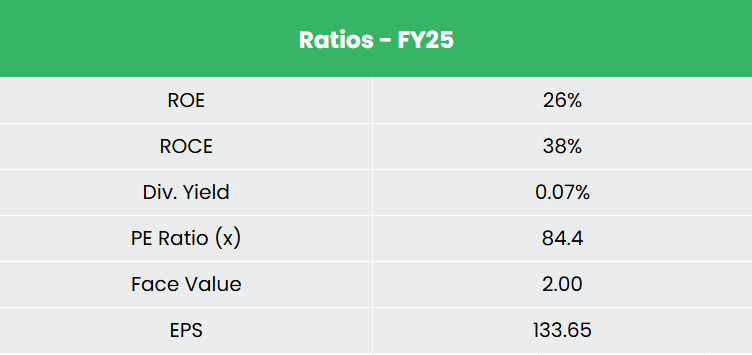

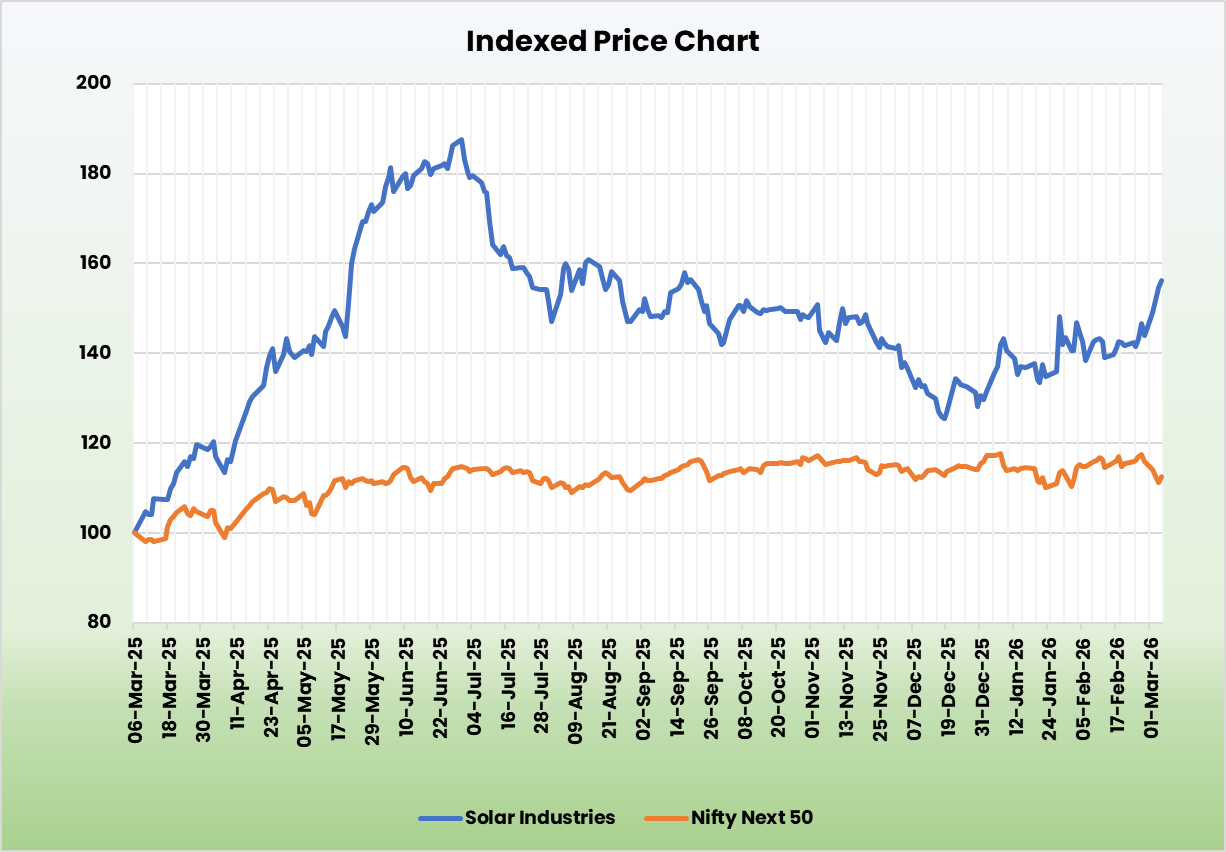

- Monetary Efficiency – The three-year income and web revenue CAGR stand at 24% and 42% respectively between FY23-25. The corporate has a debt-to-equity ratio of 0.17x, and the 3-year common ROE and ROCE are round 33% and 36% for FY23-25 interval.

Business

The Indian explosives market is structurally underpinned by mining and infrastructure exercise, with coal manufacturing reaching 1,047.69 MT in FY25, iron ore manufacturing hitting a document 289 MMT in FY25, and the development market projected to broaden from Rs. 63,41,060 crore (US$ 740 billion) in 2025 to Rs. 88,26,070 crore (US$ 1.03 trillion) by 2030, all of that are direct drivers of bulk and packaged explosive demand. On the defence aspect, India’s home manufacturing reached a document Rs. 1,50,590 crore (US$ 17.57 billion) in FY25, up 18% YoY, with the federal government focusing on Rs.3,00,000 crore (US$ 34.7 billion) in manufacturing by FY29, whereas defence exports surged from Rs.686 crore in FY14 to Rs. 23,622 crore (US$ 2.76 billion) in FY25. The federal government’s sustained push below Aatmanirbhar Bharat, encompassing Optimistic Indigenisation Lists, import embargoes on 4,666 gadgets, and a mandated 75% home sourcing from the capital acquisition funds has structurally redirected procurement towards home producers.

Progress Drivers

- Indigenisation mandates – 5 Optimistic Indigenisation Lists overlaying 509 gadgets and import embargoes on 4,666 defence gadgets by December 2029, with 75% of the capital acquisition funds mandated for home procurement, structurally redirecting multi-year order movement towards indigenous ammunition and propellant producers.

- Surging defence funds and capex – MoD obtained Rs. 6,81,000 crore (US$ 78.7 billion) in FY26, up 9.5% YoY, with Rs. 1,80,000 crore earmarked for capital expenditure and the armed forces projected to spend US$ 130 billion on capital procurement over 2021–26.

- Liberalised FDI enabling know-how partnerships – FDI as much as 74% permitted below the automated route in defence manufacturing (up from 49%) and 100% in mining and minerals processing.

Peer Evaluation

Opponents – Premier Explosives Ltd, and so forth.

In comparison with its friends, Photo voltaic demonstrates trade main return ratios, with a ROCE of ~38% and ROE of ~33% towards the peer median of ~21% and ~19% respectively. The corporate’s valuation metrics mirror a big premium to friends, justified by its superior earnings high quality, profitability and a diversified income combine throughout industrial explosives, defence, and worldwide markets.

Outlook

The outlook for Photo voltaic Industries stays constructive, supported by enhancing demand circumstances and its ongoing strategic transition towards increased value-added defence manufacturing. Whereas efficiency in H1FY26 was impacted by an prolonged monsoon that quickly affected mining exercise and explosives demand, administration expects a restoration within the second half as mining operations normalise, supporting double-digit progress within the home market and enabling the corporate to fulfill its annual steering. Over the medium time period, growing contribution from defence merchandise and exports might improve the income combine and assist margin enlargement.

Valuations

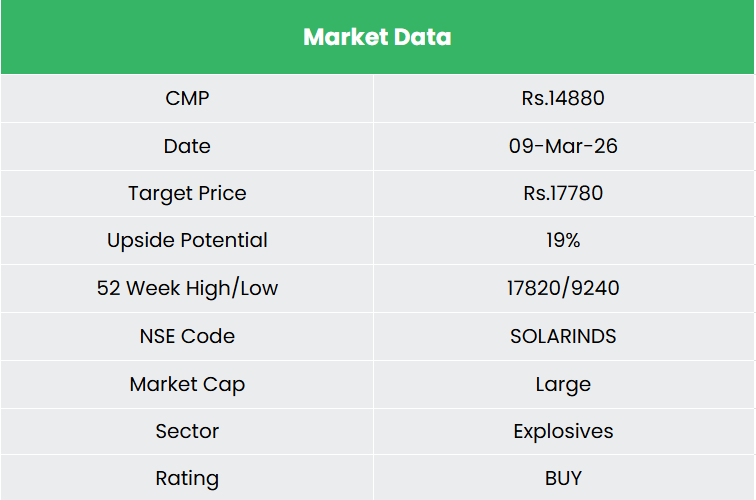

We consider the excessive margin defence pipeline and targeted capex plans will assist maintain the expansion momentum for Photo voltaic Industries. We suggest a BUY ranking within the inventory with the goal worth (TP) of Rs.17,780, 84x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully.

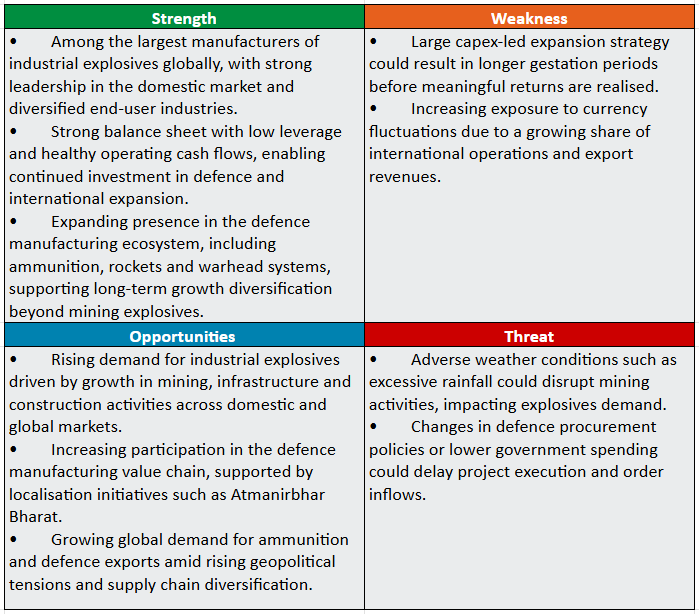

SWOT Evaluation

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

1,700

{kind=link}