The digitally targeted non-bank lender, which caters to retail debtors, small companies and corporates, is anticipated to achieve from the quicker tempo of credit score development amongst non-banking monetary firms (NBFCs).

But, traders should weigh the corporate’s scale, model energy, and AAA credit standing towards near-term considerations round profitability and asset high quality.

IPO highlights

The ₹15,511-crore preliminary public providing (IPO), the fourth-largest in India, opens on Monday and can stay open for subscription till Wednesday. The corporate has priced the supply at ₹310-326 per share, comprising a recent problem of ₹6,846 crore and a proposal on the market value ₹8,666 crore.

The NBFC will channel the proceeds to strengthen the corporate’s tier-I capital or threat buffer for future lending.

Progress story

Based in 2007, Tata Capital has grown into one among India’s largest NBFCs. As of June, it had served 7.3 million prospects, providing merchandise throughout retail, small and medium enterprises (SME), company, and entrepreneur segments.

Retail loans rose to 61.3% of its portfolio in Q1FY26, up from 56.7% in FY23. SME lending, in distinction, declined from 32.6% in FY23 to 26.2% in FY25, whereas company lending climbed modestly to 12.5%.

The mortgage ebook expanded to ₹2.33 trillion by March, clocking 37.3% compounded annual development price (CAGR) over FY23–FY25—the quickest amongst massive NBFCs.

Department enlargement was much more aggressive, with the community rising 3x since March 2023, forward of Bajaj Finance Ltd, Cholamandalam Funding and Finance Co., L&T Finance Ltd, and HDB Monetary Providers Ltd. The merger with Tata Motors Finance expanded its footprint.

“In case you have a look at our development numbers, the headline price appears increased due to the merger with Tata Motors Finance,” Rajiv Sabharwal, managing director and chief government officer at Tata Capital, advised Mint. “On paper, it seems like we’re rising at about 38%. However in case you strip away the merger influence, our natural development is nearer to twenty-eight.5%—which, even by itself, could be very sturdy.”

Digital push

Know-how and the Tata model are the dual engines of Tata Capital’s technique. Over 98% of consumers are digitally onboarded, and 99% of collections occur on-line. Cross-selling inside the Tata ecosystem, from Croma’s retail shops to Tata Motors’ dealerships, offers the corporate a prepared pipeline of consumers.

“Tata Capital, although a late entrant in high-margin segments, has gained floor by leveraging the Tata group ecosystem—Tata Motors, Croma and Tata Housing—for cross-selling,” mentioned Prashanth Tapse, senior VP, analysis analyst at Mehta Equities. “This, together with fast department enlargement in Tier 2 and Tier 3 cities, has constructed a powerful captive base, positioning the corporate to maintain sturdy mortgage development into H2FY26.”

The corporate’s community has expanded fourfold in recent times. “With greater than 25 merchandise in our portfolio, we basically have a number of engines of development. Product depth coupled with attain is driving momentum,” Sabharwal mentioned.

In accordance with Ratiraj Tibrewal, director at Selection Capital, development for Tata Capital has come from sturdy retail and SME demand, digital distribution, and department enlargement, with housing finance a key driver. “Supported by threat controls and product range, Tata Capital now goals to deepen Tier 2/3 penetration and scale digital origination.”

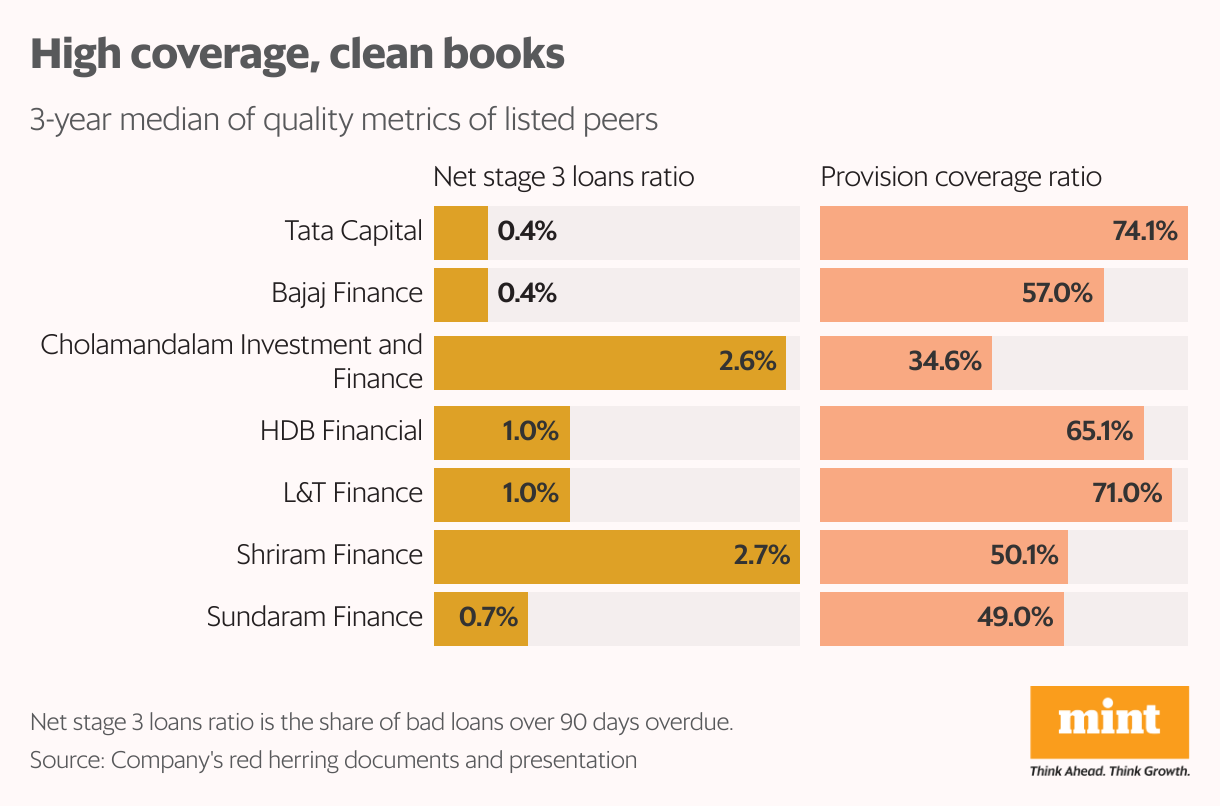

High quality watch

A key consolation issue is asset high quality. Between FY23 and FY25, Tata Capital maintained a median internet Stage 3 mortgage ratio (share of dangerous loans over 90 days overdue) of 0.4%, in keeping with Bajaj Finance, and posted the best provision protection ratio amongst friends at 74%. This implies it’s well-shielded from credit score shocks.

“Our philosophy is to maintain credit score prices beneath 1%. Each enterprise determination is taken by a risk-management lens,” Sabharwal mentioned. “The mortgage ebook stays largely secured, with solely 12% publicity to unsecured retail loans.”

But dangers stay. The merger with Tata Motors Finance dragged on high quality, with gross Stage 3 loans spiking to 7.1% in FY25 and triggering a ₹181-crore loss. Web Stage 3 ranges stayed underneath management, and Tata Capital’s prudent underwriting and threat administration have stored asset high quality wholesome, mentioned Tapse. “But, sustaining sub-1% internet Stage 3 loans amid fast development could also be difficult within the coming quarters, warranting warning.”

In accordance with Tibrewal of Selection Capital, the mortgage combine supplies resilience, with over three-fourths of the ebook secured by collateral. “Going ahead, the corporate’s technique ought to be to prioritize high quality development over quantity, guaranteeing that asset high quality stays secure even because the ebook expands.”

Tata Capital’s contingent liabilities are one other metric to observe. They at present stand at ₹6,793 crore or 18.5% of its FY25 revenue, although down from 26.4% in FY23. Chief monetary officer Rakesh Bhatia advised Mint that these had been largely tax-related and traditionally resolved within the firm’s favour.

Analysts, too, view the danger as restricted. “At 3-4.5% of fairness, it’s a manageable threat, although value monitoring if it rises year-on-year,” mentioned Tapse. Tibrewal calls the liabilities small relative to the corporate’s sturdy internet value.

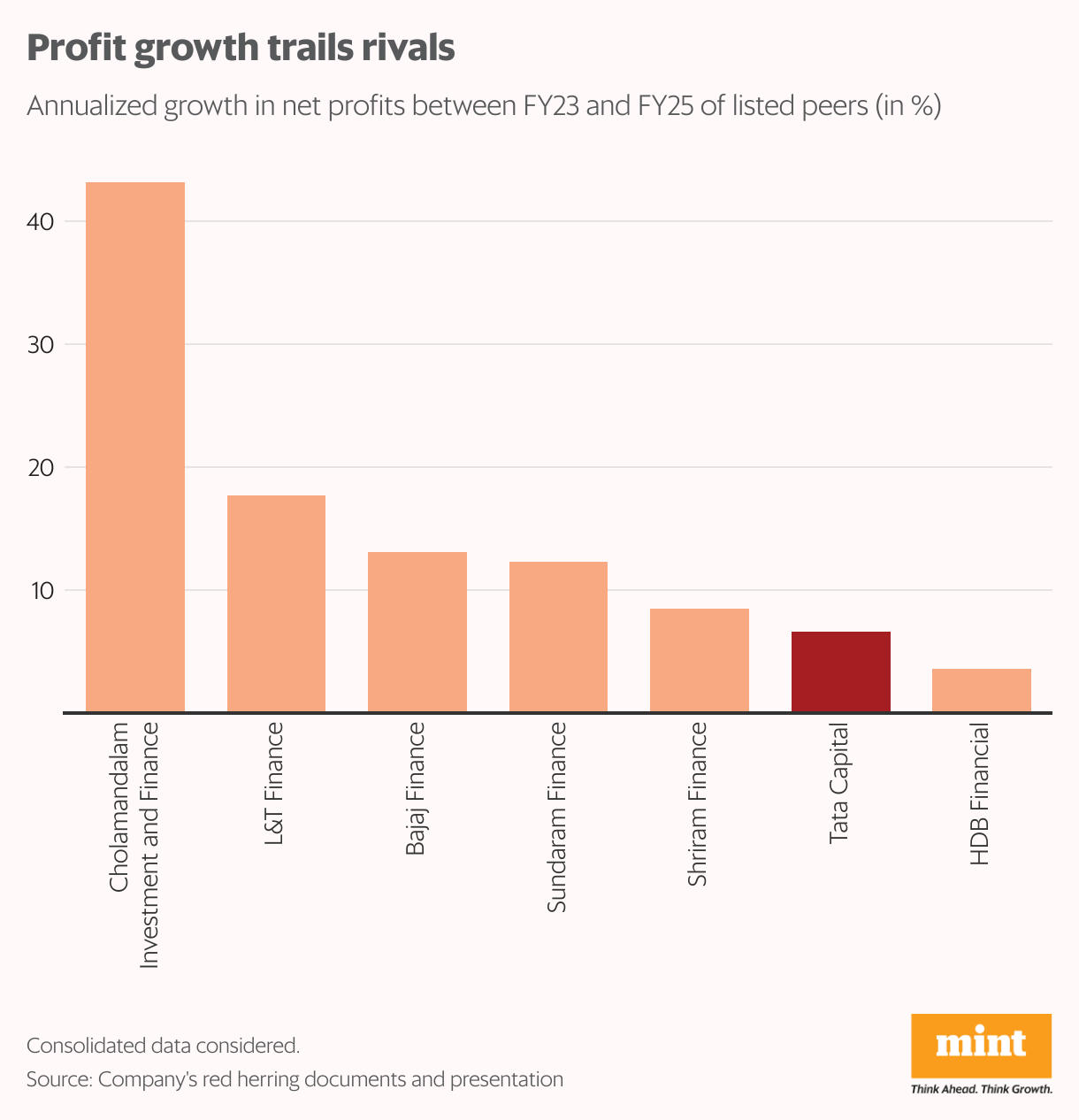

Profitability lag

Tata Capital’s development has not translated into peer-level profitability. Web revenue rose from ₹2,945.7 crore in FY23 to ₹3,655 crore in FY25, posting a modest CAGR of 6.6%. In distinction, Cholamandalam posted 43% CAGR, Bajaj Finance 13%, and L&T Finance 17.6%. Rising borrowing prices have damage margins, with the price of funds climbing from 6.6% in FY23 to 7.8% in FY25.

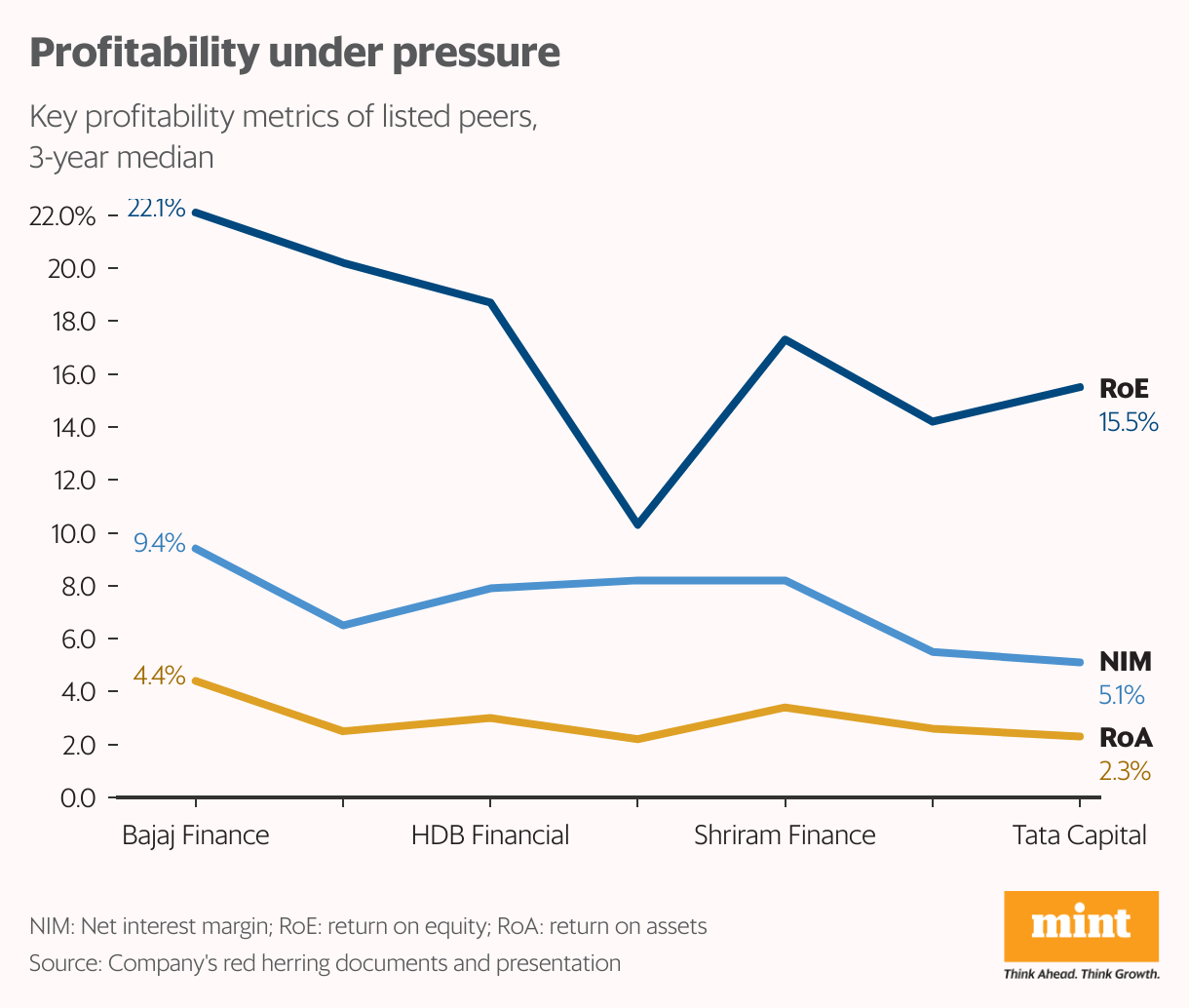

The stress is most evident in profitability ratios. Tata Capital’s internet curiosity margin is barely 5.1%, the bottom amongst massive NBFCs, in comparison with 9.37% for Bajaj Finance, 8.24% for Shriram Finance, and eight.21% for L&T Finance. Its return on fairness has slipped to fifteen.5%, nicely beneath Bajaj Finance and Cholamandalam (each above 20%), whereas return on belongings at 2.3% trails Bajaj Finance’s 4.44%.

The NBFC’s administration attributes this to aggressive development and the merger. “The merger has had an influence, however enchancment will begin exhibiting from this 12 months itself,” mentioned Sabharwal.

“The decline in RoE is primarily resulting from capital infusion to assist fast stability sheet development and department enlargement. With scale and working leverage, RoE ought to get well above 15% within the subsequent 12-18 months,” mentioned Tibrewal.

Tapse, too, famous that falling RoE displays the high-growth part needing fairness infusion. Tata Capital should enhance profitability and capital effectivity. With branch-led working leverage, higher price efficiencies and deal with RoE-accretive segments, RoE may return to excessive teenagers by FY26-27, he mentioned.

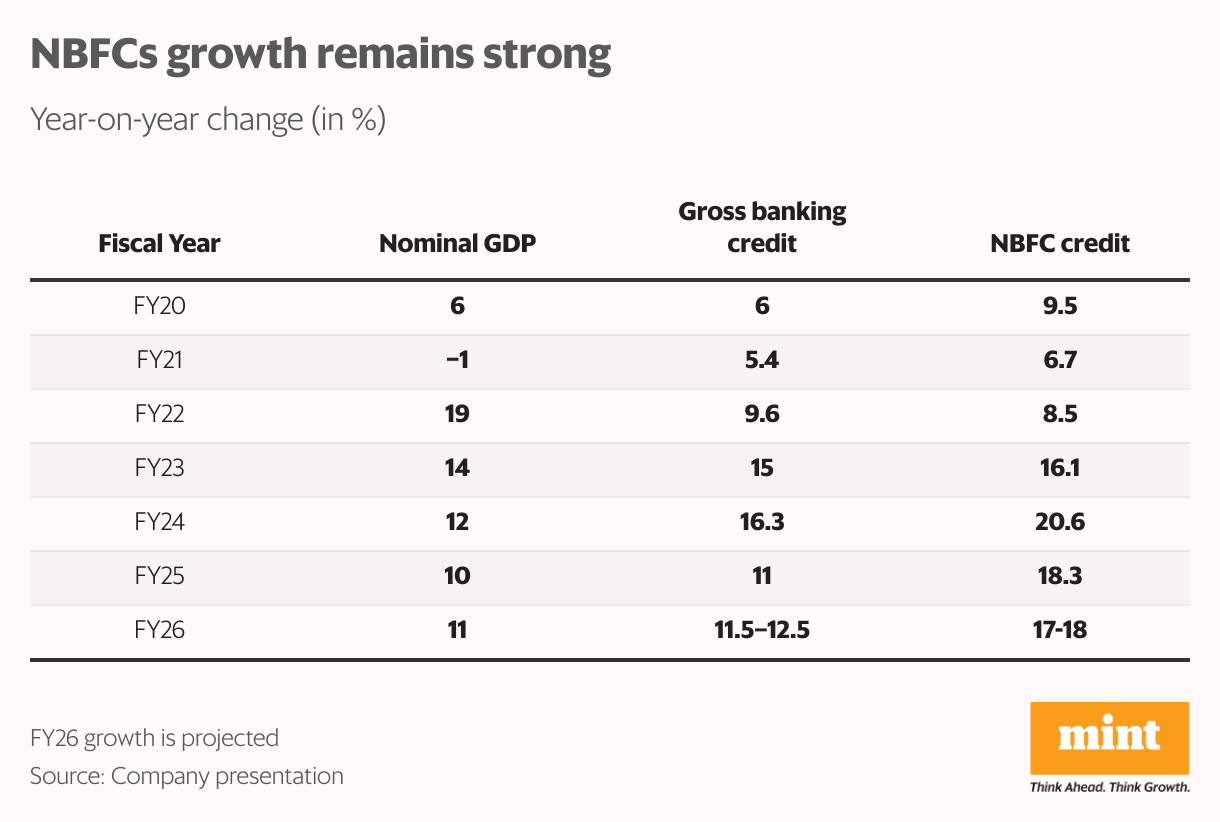

NBFC momentum

The broader NBFC cycle is a silver lining.

In FY25, NBFC credit score grew 18.3%, almost double India’s nominal GDP development and much forward of financial institution credit score at 11%. Analysts anticipate 17-18% development to maintain in FY26.

This secular development helps massive NBFCs like Tata Capital, that are well-placed to seize demand for retail and SME credit score.

")