Already weighed down by international coverage uncertainty, the Piramal Pharma counter has prolonged its correction after its earnings for the fourth quarter of 2024-25 dissatisfied buyers.

However is the correction a possibility for buyers to purchase the inventory, or a sign of extra stress to return?

From turnaround to disappointment

Piramal Pharma is certainly one of India’s main pharmaceutical firms with 17 manufacturing and improvement websites, and industrial presence in additional than 100 nations. Its spick-and-span high quality track-record speaks for itself—the corporate has efficiently cleared nearly 50 inspections of its international services by the US Meals and Drug Administrator since FY12.

Piramal Pharma’s financials had been below stress however the firm rotated its enterprise. From FY23 to FY25, its income grew at a compound annual development price of 14%, and its EBITDA margin expanded from 12% to 17%.

And from a lack of ₹186 crore in FY23, Piramal Pharma swung to a revenue of ₹91 crore in FY25. Importantly, the turnaround was accompanied by a moderation in debt—internet debt to EBITDA dropped from 5.6x to 2.7x in the course of the interval.

However Piramal Pharma’s newest fourth-quarter outcomes dissatisfied buyers. Income development was muted at 8% year-on-year and EBITDA margin was flat at 22%. Whereas revenue elevated 52%, a bulk of the expansion was because of a rights write-off undertaken within the base quarter.

Additionally learn | Defence shares are hovering once more, however can fundamentals help the rally?

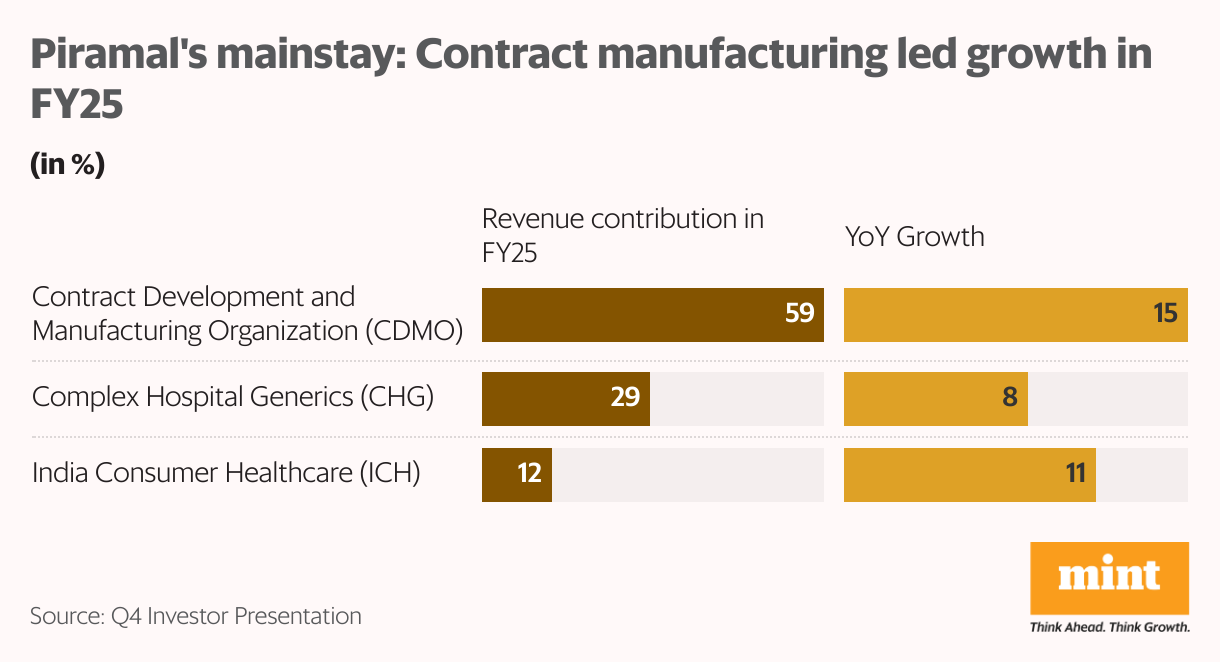

Mainstay phase led development in FY25

Piramal Pharma operates in three key segments. Its contract improvement and manufacturing group (CDMO) enterprise contributed 59% of its income in FY25 and its complicated hospital generics (CHG) enterprise, which incorporates merchandise akin to anesthesia and intrathecal remedy, accounted for 29%. The steadiness 12% contribution got here from its India shopper healthcare (ICH) enterprise, which offers in over-the-counter shopper and wellness merchandise.

Piramal Pharma’s mainstay phase, CDMO, registered a barely greater share of innovation-related work final 12 months—54% in FY25 vs 50% in FY24. It additionally scored a 54% surge in on-patent industrial manufacturing.

The end result: The corporate’s CDMO enterprise delivered 15% year-on-year development in FY25, supporting general income development of 12%. EBITDA margin for the phase additionally improved, due to improved efficiencies in procurement and operations.

The tariff uncertainty impact

Prescription drugs are presently not below the purview of the US’s reciprocal tariffs on merchandise exported to the nation. However US President Donald Trump has indicated that discussions are underway to strip the pharma sector of this exemption.

If that occurs, it might considerably harm India’s pharma sector, which counts the US as its largest marketplace for pharmaceutical merchandise manufactured in India, together with generic or off-patent medication and pricier branded merchandise.

Indian pharma firms will face steeply greater manufacturing prices if they’ve to maneuver their manufacturing to the US because of Trump’s reciprocal tariffs, which have been suspended till 9 July.

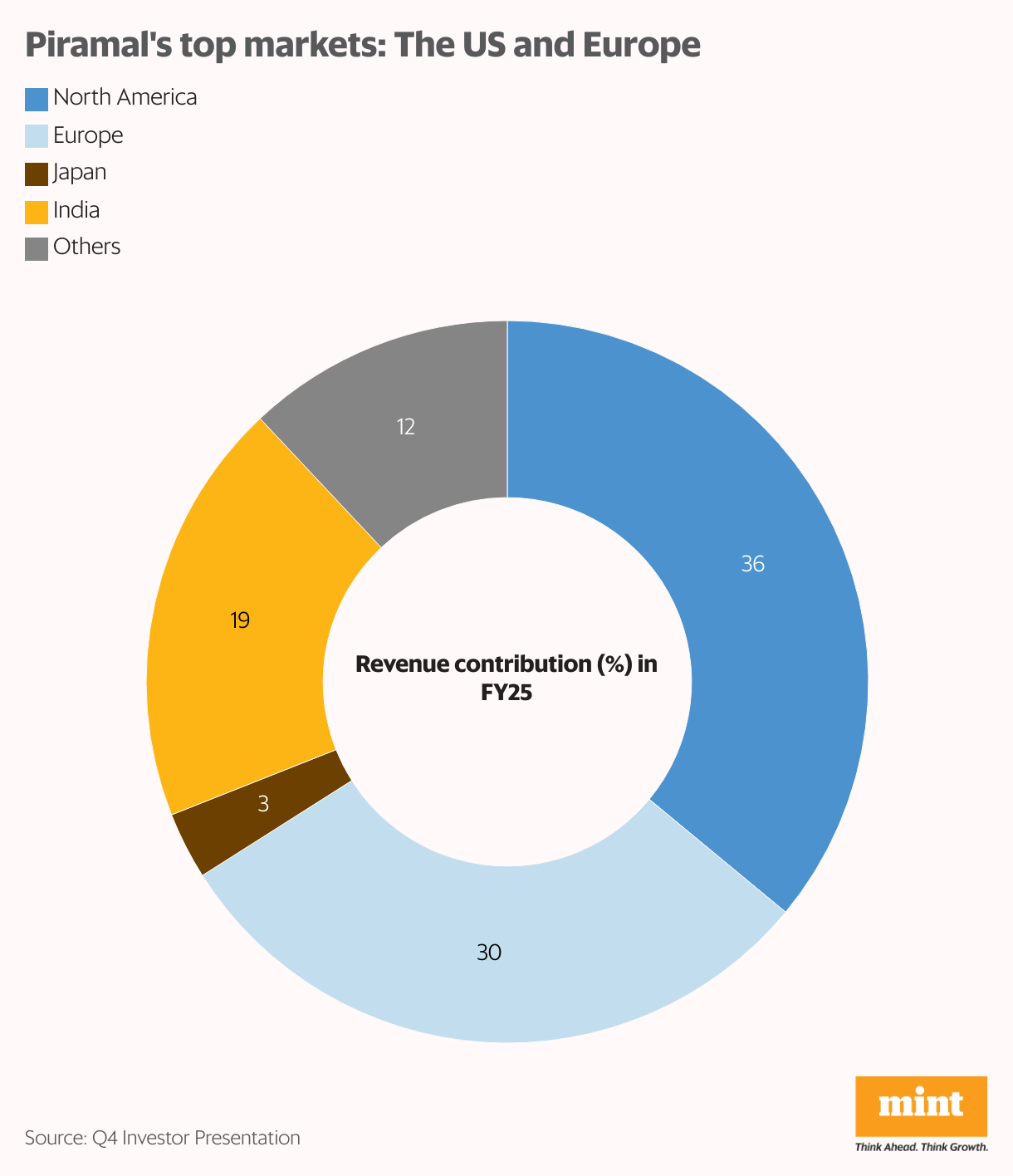

Piramal Pharma, which derives greater than a 3rd of its income from North America, has already invested $470 million in its manufacturing services within the US. Further capital expenditure of $90 million is within the works.

Additionally learn | Why Tata Teleservices is drawing institutional bets regardless of mounting losses

Making issues worse: Trump’s drug-pricing order

Regardless of greater manufacturing prices within the US, greater costs of on-patent medication available in the market might have made manufacturing such merchandise there financially possible.

However the newest twist within the story is Trump’s govt order asking pharma firms to slash the costs of on-patent medication within the US to match the most cost effective international costs.

Additionally learn | Mint Explainer: Why Indian pharma is spooked by Trump’s newest drug coverage

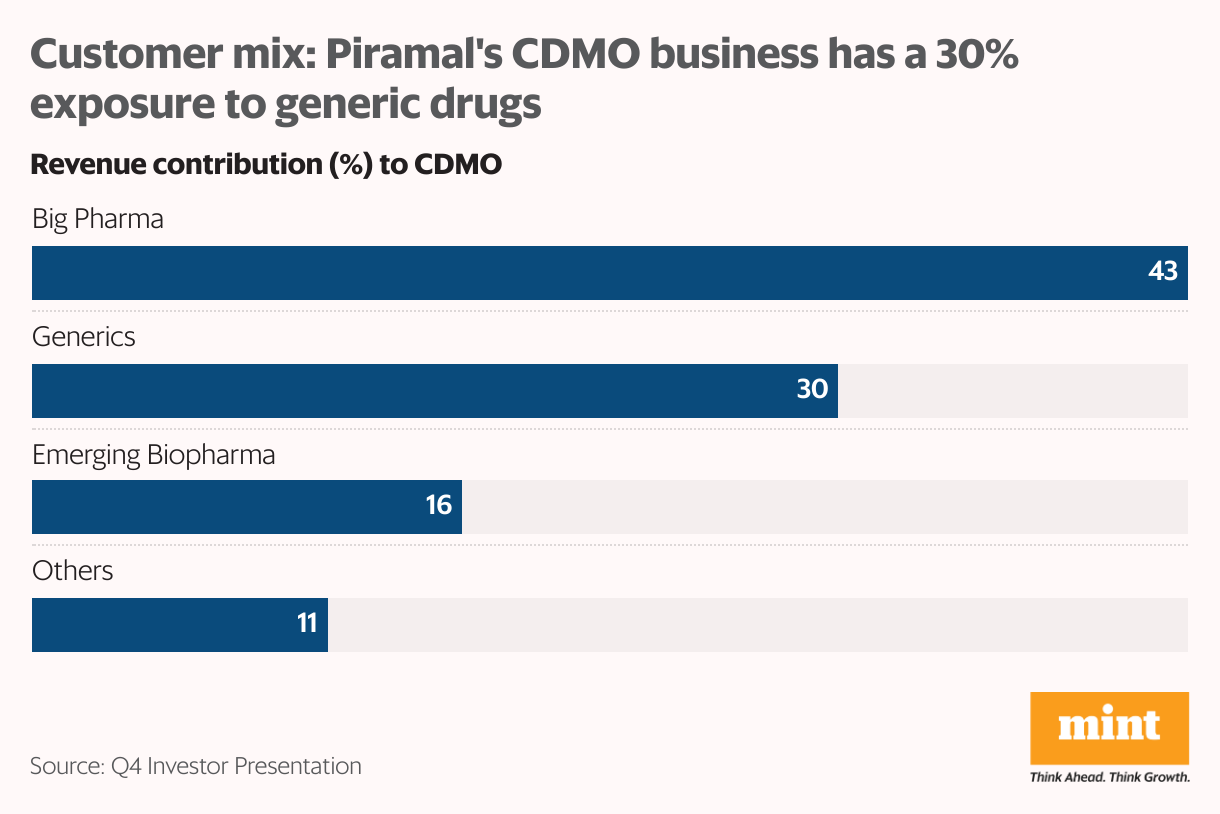

On condition that Piramal’s CDMO customer-mix is skewed in direction of massive pharma and rising biopharma, with solely 39% publicity to generics, the corporate is in danger if Trump’s drug value order goes by.

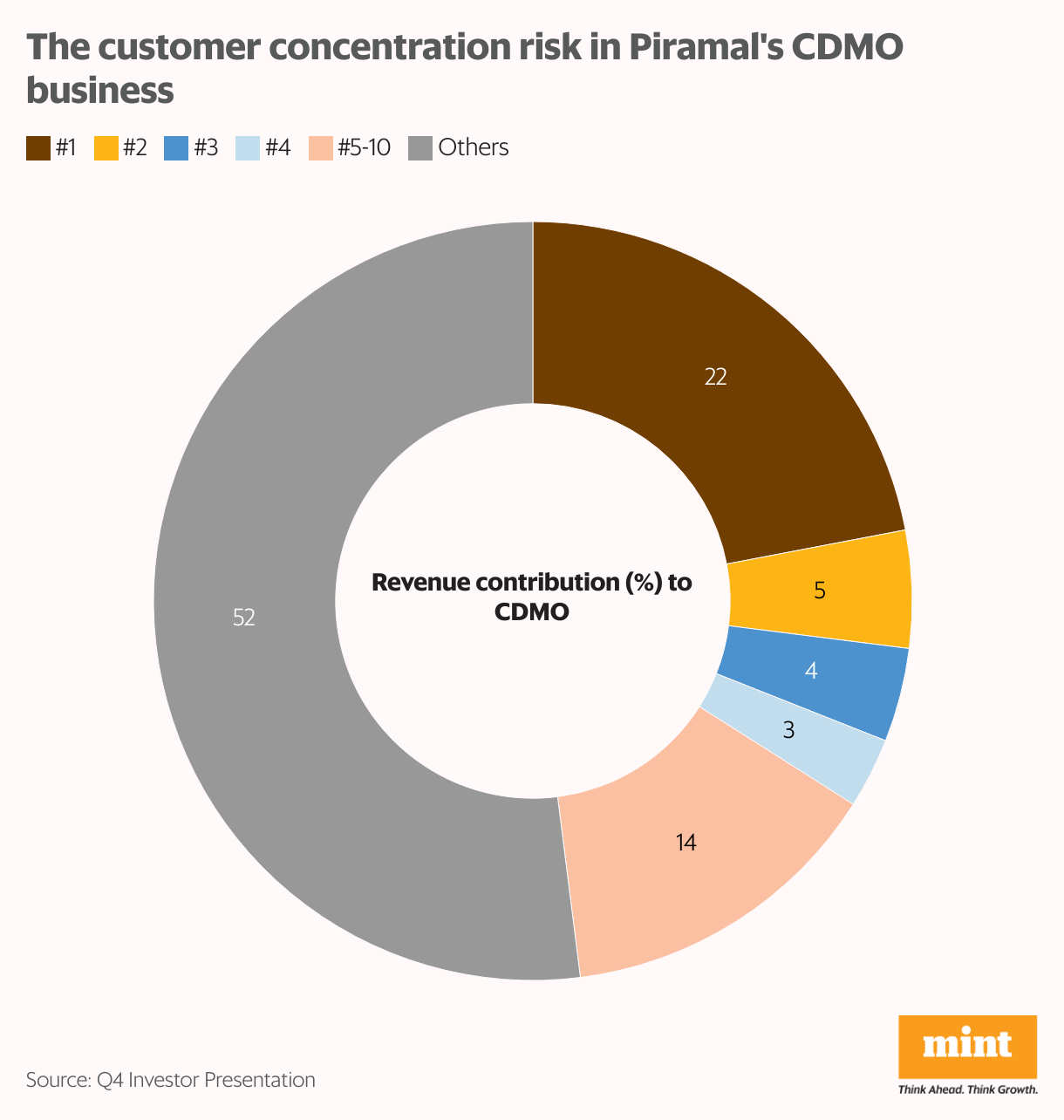

The uncertainty has frayed buyers’ nerves. Biotech funding within the US has seen uneven enchancment, resulting in selective and delayed order placement. The client focus danger at Piramal’s CDMO enterprise has exacerbated the circumstances. Whereas it has over 500 prospects, its high 10 prospects contribute nearly half of the enterprise.

Consequently, Piramal’s abroad CDMO websites are working considerably under capability. This has decreased working leverage whilst working bills rise on account of a brand new manufacturing facility. Income development in CDMO for Piramal is anticipated to be in single digits in FY26, with EBITDA margin more likely to stay careworn.

Additionally learn | Chalet Motels is gearing up for a serious enlargement. Ought to buyers test in now?

India enterprise presents consolation

Piramal Pharma’s CDMO websites in India contribute 6% to its enterprise, and have been working at wholesome utilizations.

The corporate’s India shopper healthcare (ICH) enterprise has additionally matched tempo with general development, registering an 11% enhance in income. Pushed by 52 new merchandise and stock-keeping models (or product traces) launched in FY25, the ICH enterprise crossed the ₹1,000 crore milestone in the course of the 12 months.

About 49% of Piramal’s ICH enterprise got here from energy manufacturers akin to Lacto Calamine, Little’s, and CIR, serving to it submit a sturdy 20% rise in fourth-quarter income.

About 21% of the phase’s gross sales got here from e-commerce, which registered an general 39% year-on-year development for Piramal Pharma in FY25. This negated a slowdown in Piramal Pharma’s i-range merchandise (i-Tablet emergency contraceptive, i-Know house kits for being pregnant and different assessments, and so forth.) caused by regulatory value controls.

Prospects for inorganic development stay open as effectively. Whereas Piramal Pharma has clarified that it gained’t be re-entering the home prescription formulations enterprise, it might contemplate buying home over-the-counter portfolios.

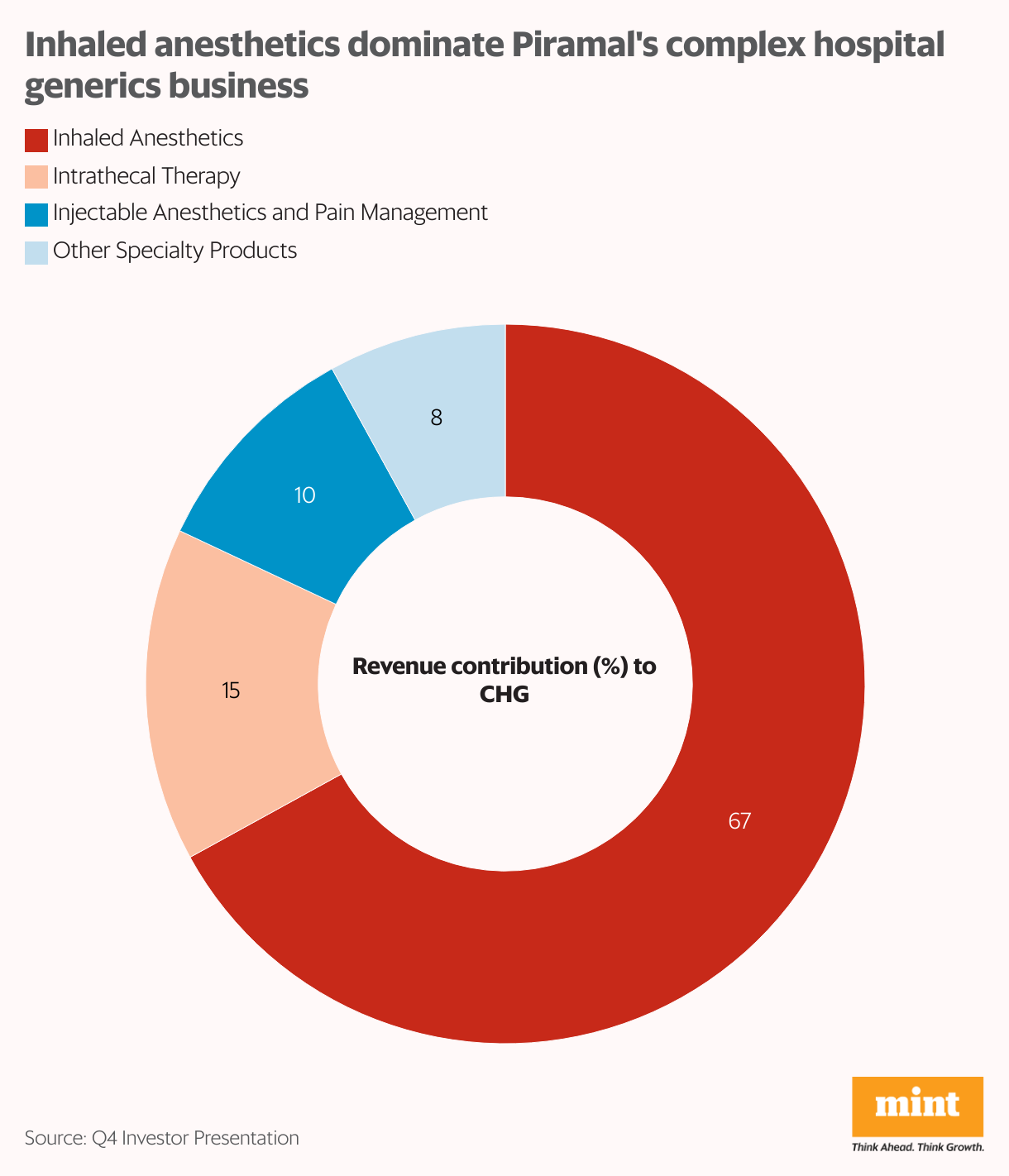

Complicated hospital generics: Cautious optimism

Piramal’s CHG phase posted an 8% year-on-year income development in FY25, the slowest amongst all its segments. It additionally dragged down Piramal’s general margin because of one-time bills and capability enlargement in India. However the facility is now operational and anticipated to ship revenues beginning FY26.

Piramal Pharma has additionally managed to hold on to its main market share in its major companies—inhaled anesthetics and intrathecal remedy. It instructions a 75% share of the US market in intrathecal baclofen, and a 44% share in inhaled anesthetics by the industry-leading ‘Sevoflurane’.

Sevoflurane accounts for 86% of the $1 billion international inhaled anesthetics market. Piramal Pharma plans to leverage its Sevoflurane services to attempt to seize the $400 million marketplace for the drug exterior the US and China.

Current launches have additional improved prospects for Piramal Pharma’s CHG enterprise. In 2025, Piramal launched an injectable to deal with psychiatric problems, and has acquired commercialization rights for the neonatal cardiovascular drug ‘Neoatricon’. The administration goals to develop the phase to $600 million by FY30.

CDMO pipeline propels hopes

To cater to rising US shopper demand, Piramal lately introduced new capital expenditure price $90 million in its US CDMO services at Lexington and Riverview. This could assist it seize a bigger share of antibody-drug-conjugates (ADCs) and injectables. The injectables market is projected at $20 billion by 2028.

The phase additionally boasts of two.8x enlargement in its improvement pipeline from 52 merchandise in FY17 to 145 in FY25.

One other tailwind can come from the US Biosecure Act, which if authorized will profit Indian CDMOs by prohibiting imports of biotechnology gear from China. Piramal’s administration goals to develop its CDMO enterprise to $1.2 billion by FY30.

Quick-term volatility

However the near-term headwinds, Piramal has affirmed its FY30 outlook of $2 billion in income with 25% EBITDA margin and 1x internet debt/EBITDA. Brokerages count on the corporate’s revenue earlier than tax (PBT) margin to develop to 16% by FY28.

However short-term volatility can’t be dominated out. Brokerages have slashed their value goal for Piramal to a variety from ₹230 to ₹340 per share. Introduction of futures and choices (F&O) contracts on the counter on the finish of this month may also add to the volatility.

At 2.45 pm on Monday, Piramal Pharma shares had been up about 0.30% at ₹205.50 apiece, down from a 2% bounce earlier within the day. Nifty Pharma was up about 0.70%.

Ananya Roy is the founding father of Credibull Capital, a Sebi-registered funding adviser.

Disclosure: The writer doesn’t maintain shares of the businesses mentioned. The views expressed are for informational functions solely and shouldn’t be thought-about funding recommendation. Readers are inspired to conduct their very own analysis and seek the advice of a monetary skilled earlier than making any funding choices.