Picture supply: Getty Photographs

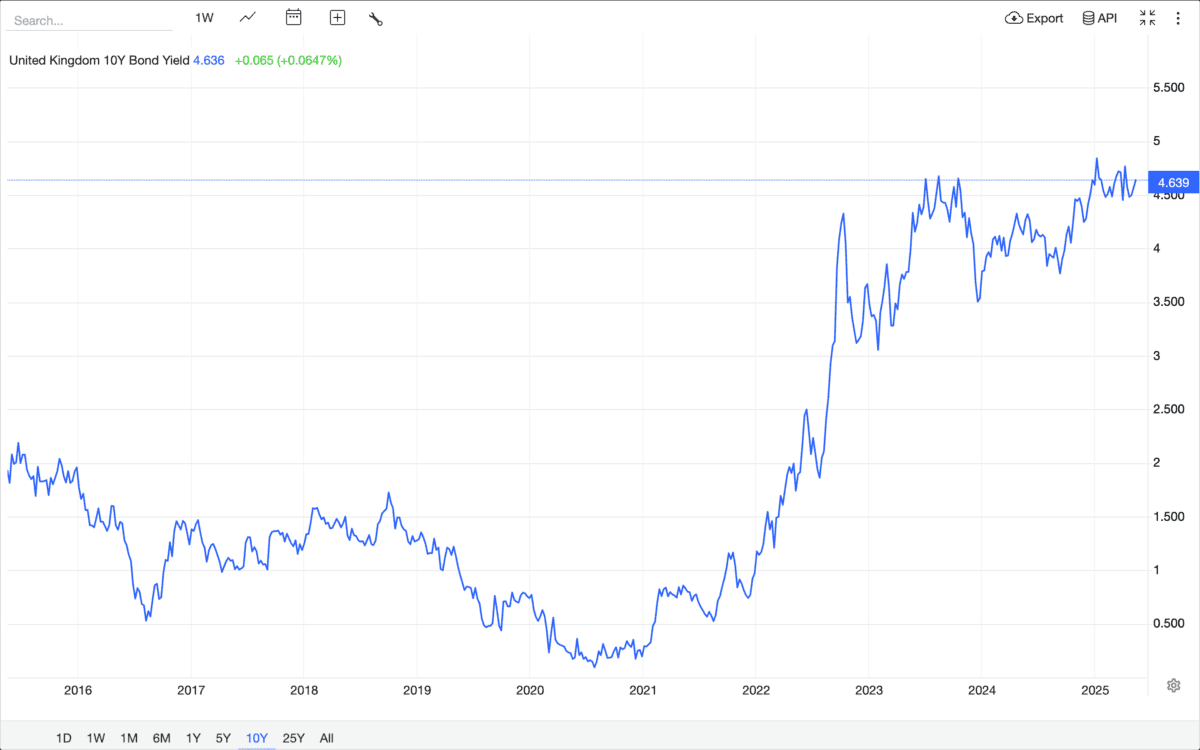

In relation to passive revenue, UK traders have a selection. And with 10-year authorities bonds providing a yield of greater than 4.6%, bonds are wanting fairly engaging proper now.

That represents a 10-year excessive and it’s one thing to be taken critically. However I feel traders can do even higher within the inventory market.

Bond market

Regardless of the asset class, investing effectively is about being grasping when others are fearful. And the present state of the bond market suggests to me that there’s some worry round for the time being.

A 4.6% yield means somebody who invests £10,000 in UK gilts can anticipate to obtain £460 annually till 2035. 5 years in the past, the identical funding would have returned round £200 per 12 months.

Supply: Buying and selling Economics

With a bond, the one means traders don’t get their anticipated return is that if the UK authorities defaults on its obligations. And that makes them a lot much less dangerous than any inventory funding.

In brief, gilts proper now provide an unusually excessive yield with a comparatively low danger. And that’s one thing passive revenue traders ought to take note of when enthusiastic about alternatives.

Shares

UK gilts haven’t been this engaging for greater than a decade. And whereas I’m sticking to the inventory marketplace for funding alternatives, that is one thing I’m taking account of.

I’m wanting additional forward than the subsequent 10 years, however the state of affairs is much more stark with the 30-year bond. The present yield is just below 5.5% – once more, the very best it’s been in a decade.

Supply: Buying and selling Economics

Within the context of my very own investing, meaning I shouldn’t be taking a look at shares the place I don’t anticipate to make at the very least 5.5% per 12 months over the subsequent 30 years. And that’s a reasonably excessive bar.

There are, nonetheless, a number of shares that I feel would possibly effectively make the grade. One in every of these is FTSE 250 housebuilder Vistry (LSE:VTY).

Shareholder returns

Vistry appears like an odd selection for passive revenue traders. The agency has lately suspended its dividend and there’s an ongoing investigation from the Competitors and Markets Authority.

Neither of these is one thing I search for in a inventory to contemplate. However the share value has fallen a lot that I feel there’s a superb likelihood it might do higher than 5.5% per 12 months going ahead.

For one factor, there’s an ongoing share buyback programme. At present ranges that by itself is equal to round 6.25% of Vistry’s present market worth.

The dividend was suspended earlier this 12 months following some accounting irregularities. However I feel these is likely to be short-term in nature and shouldn’t derail the distribution for too lengthy.

Revenue alternatives

Bonds are unusually engaging from a long-term passive revenue perspective. Regardless of this, I nonetheless assume I can discover higher alternatives for my portfolio within the inventory market for the time being.

Vistry doesn’t appear like probably the most promising funding for the time being, but it surely’s effectively value a more in-depth look. I feel its partnerships enterprise has some glorious long-term prospects.

It’s truthful to say there are some short-term dangers and alternatives. However I’m critically contemplating it for my Shares and Shares ISA as potential alternative to do higher than a 30-year bond.