Vishal Mega Mart Ltd – Reasonably priced Necessities for Each Indian Family

Based in 2001 and based mostly in Gurugram, Vishal Mega Mart Ltd. is a number one retail hypermarket chain in India, providing a broad spectrum of merchandise together with attire, groceries, electronics, and residential necessities. The corporate operates by way of a mix of its personal manufacturers and third-party manufacturers, reaching clients by way of a nationwide community of 717 shops, together with a web-based buying app and web site. The corporate serves primarily center and decrease – center earnings customers and is current in 472 cities throughout 28 states and a pair of union territories. It’s acknowledged as a number one offline-first diversified retail chains within the nation.

Merchandise and Companies

The corporate’s choices may be categorized throughout 3 enterprise segments:

- Attire – Product portfolio consists of t-shirts, shirts, denim, athletic and leisure put on, evening put on, innerwear, western put on, formal put on, and ethnic put on for males, ladies, kids, and infants.

- Basic Merchandize – Dwelling home equipment, crockery and utensils, residence merchandise and furnishings, toys, stationery, journey merchandise and footwear, and so on.

- Quick-moving shopper items (FMCG) – Biscuits, savoury snacks (namkeen), noodles, tea, espresso, staples resembling mustard oil, soya oil, clarified butter (desi ghee) and spices, and non-food merchandise resembling child diapers, hair oil, sanitary pads and handwash, amongst others.

Subsidiaries – As of FY24, the corporate has 2 subsidiaries and no different affiliate firms/joint ventures.

Funding Rationale

- Pan-India Footprint – The corporate has established a robust pan-India footprint with 717 shops throughout the nation (42% within the North, 29% East, 21% South, and eight% West), and added 23 new shops together with entry into 16 new cities in Q1FY26, increasing its complete buying and selling space to 12.4 million sq. ft. The corporate continues to penetrate underrepresented areas, with profitable growth into Kerala and pilot retailer launches in Maharashtra and Gujarat geared toward strengthening its presence in Western India. It is usually scaling up a cluster-based technique by way of smaller-format shops, with six such shops at present operational in Uttar Pradesh and Haryana, performing according to income and profitability targets. These strategic initiatives permit the corporate to speed up its presence in high-potential, underpenetrated markets whereas sustaining a capital-efficient progress mannequin. The smaller-format shops supply faster rollout and quicker breakeven, making them best for Tier-2 and Tier-3 places.

- Enlargement methods – The corporate is actively increasing its digital footprint by way of e-commerce and fast commerce, with 670 out of 717 shops servicing fast commerce orders throughout 455 cities as of June 30, 2025. This phase has already attracted ~10 million registered customers and now contributes 6 – 8% to retailer revenues. Notably, 20% of fast commerce clients are solely new to the model, making this an incremental income channel. As one of many first retail gamers to introduce e-commerce in a lot of its working cities, the corporate has efficiently broadened its buyer attain whereas sustaining sturdy unit economics. Moreover, it continues to serve the “first-price” value-conscious phase, whereas strategically working to improve customers to increased value factors. With 95% of income coming from loyal clients and a 17% YoY enhance in loyalty memberships, the corporate enjoys sturdy buyer retention and repeat buy behaviour. Its deal with non-public labels – contributing ~60% of gross sales quantity – additional helps margin growth and model differentiation.

- Q1FY26 – Throughout the quarter the corporate reported sturdy monetary efficiency, with income rising 21% YoY to Rs.3,140 crore, in comparison with Rs.2,596 crore in Q1FY25. EBITDA grew by 26% YoY to Rs.459 crore, up from Rs.366 crore, whereas internet revenue elevated 37% YoY to Rs.206 crore in comparison with Rs.150 crore. The corporate achieved a same-store gross sales progress (SSSG) of 11.4%, supported by the next variety of buyer transactions. Gross margins remained steady within the vary of 28.2% – 28.4%, whereas EBITDA margins improved from 14.1% to 14.6%. The margin growth was primarily pushed by operational efficiencies and improved transaction volumes, reflecting the corporate’s potential to drive profitability alongside income progress.

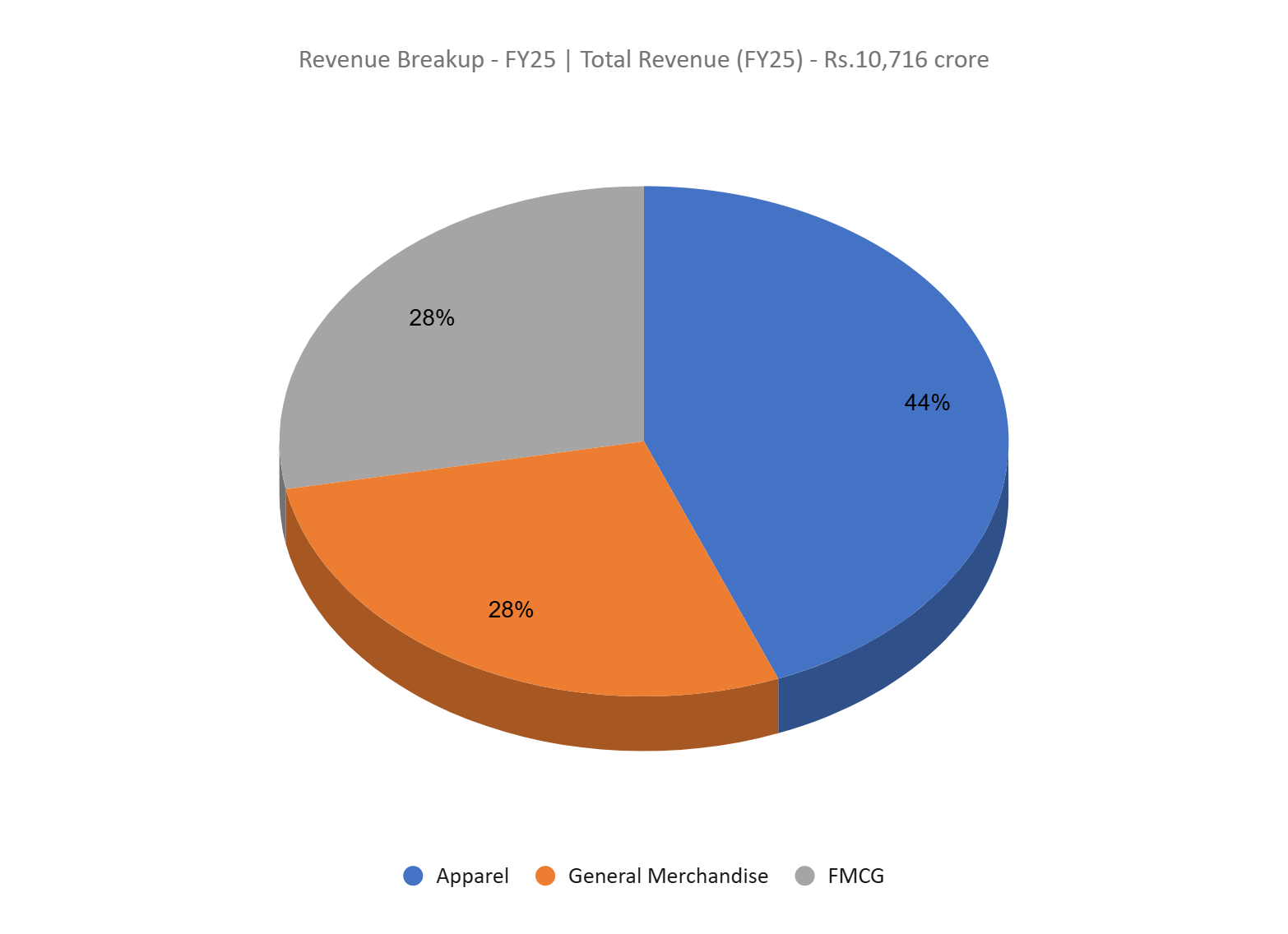

- FY25 – The corporate generated income of Rs.10,716 crore, a rise of 20% in comparison with FY24 income. Working revenue is at Rs.1,530 crore, up by 23% YoY. The corporate posted internet revenue of Rs.632 crore, a soar of 37% YoY.

- Monetary Efficiency – The corporate has generated a income and internet revenue CAGR of 24% and 47% over the interval of three years (FY23-25). Common 3-year ROE & ROCE is round 9% and 11% for FY23-25 interval. The corporate has a sturdy capital construction with a debt-to-equity ratio of 0.27.

Business

India’s retail and e-commerce sectors are experiencing strong progress, pushed by rising incomes, urbanization, and altering shopper preferences. The e-commerce market is projected to succeed in USD 91.24 billion by 2029, whereas the organised retail sector is predicted to the touch USD 230 billion by 2030. Contributing over 10% to GDP and using 35+ million folks, the sector is ready to create 25 million new jobs by 2030. With a rising center class, growing rural connectivity, and the third-largest e-retail shopper base globally, India is rising as a key marketplace for each offline and on-line retail, supported by sturdy financial fundamentals and digital integration.

Development Drivers

- India’s giant and increasing center class with rising buying energy, mixed with a largely untapped retail market.

- 100% FDI permitted trough the automated route in on-line retail of products and companies.

- Fast digital adoption and growing web penetration, particularly in Tier II and Tier III cities, are enabling better entry to e-commerce platforms, increasing the patron base and driving progress throughout each on-line and offline retail channels.

Peer Evaluation

Rivals: Avenue Supermarts Ltd (DMART), V-Mart Retail Ltd, and so on.

In comparison with its friends, the corporate has delivered a stronger general efficiency, with superior gross sales progress, margin-driven earnings growth, and steady returns on capital employed.

Outlook

The corporate’s confirmed potential to duplicate its success throughout numerous geographies and retail codecs positions it properly for scalable, sustainable progress. The corporate’s strategic deal with increasing its bodily footprint, accelerating smaller-format retailer rollouts, and strengthening its digital presence by way of e-commerce and fast commerce enhances its working leverage whereas lowering regional focus danger. These initiatives are anticipated to drive constant top-line progress, incremental buyer acquisition, and margin enchancment. With sturdy earnings visibility, cost-efficient growth, and a defensible worth positioning in India’s mass-market retail phase, the corporate emerges as a compelling funding alternative within the evolving retail panorama.

Valuation

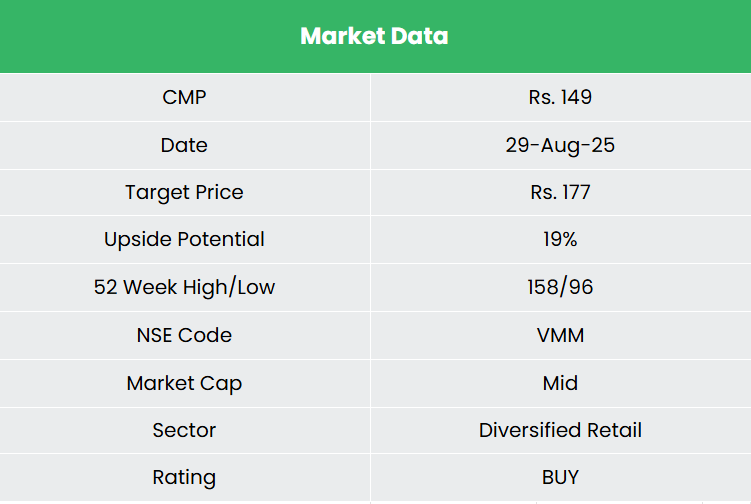

We imagine Vishal Mega Mart’s in depth product portfolio and buyer retention methods locations it in a robust place within the India’s retail area. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.177, 101x FY27E EPS.

Be aware: We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

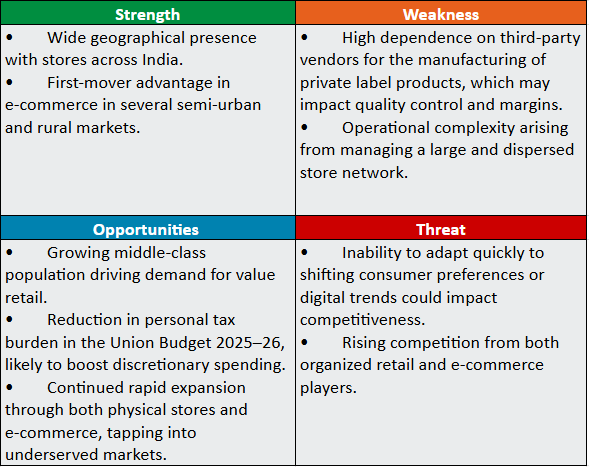

SWOT Evaluation

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM on no account assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Put up Views:

57

{kind=link}