Lloyds Metals & Vitality Ltd – Empowering India’s Infrastructure

Integrated in 1977 and headquartered in Mumbai, Lloyds Metals & Vitality Ltd. (LMEL) is an built-in mining-to-metals firm with a quickly increasing presence throughout iron ore mining, beneficiation, pellets, direct decreased iron (DRI), and downstream metal. The corporate operates one among India’s most scalable mining ecosystems, anchored by its flagship iron ore operations in Gadchiroli, Maharashtra, and supported by a rising community of midstream and downstream belongings. As of Q2FY26, LMEL instructions an Environmental Clearance (EC) of 55 MTPA for iron ore, together with operational pellet, DRI, energy, and slurry pipeline infrastructure spanning Maharashtra and Odisha.

Merchandise and Companies

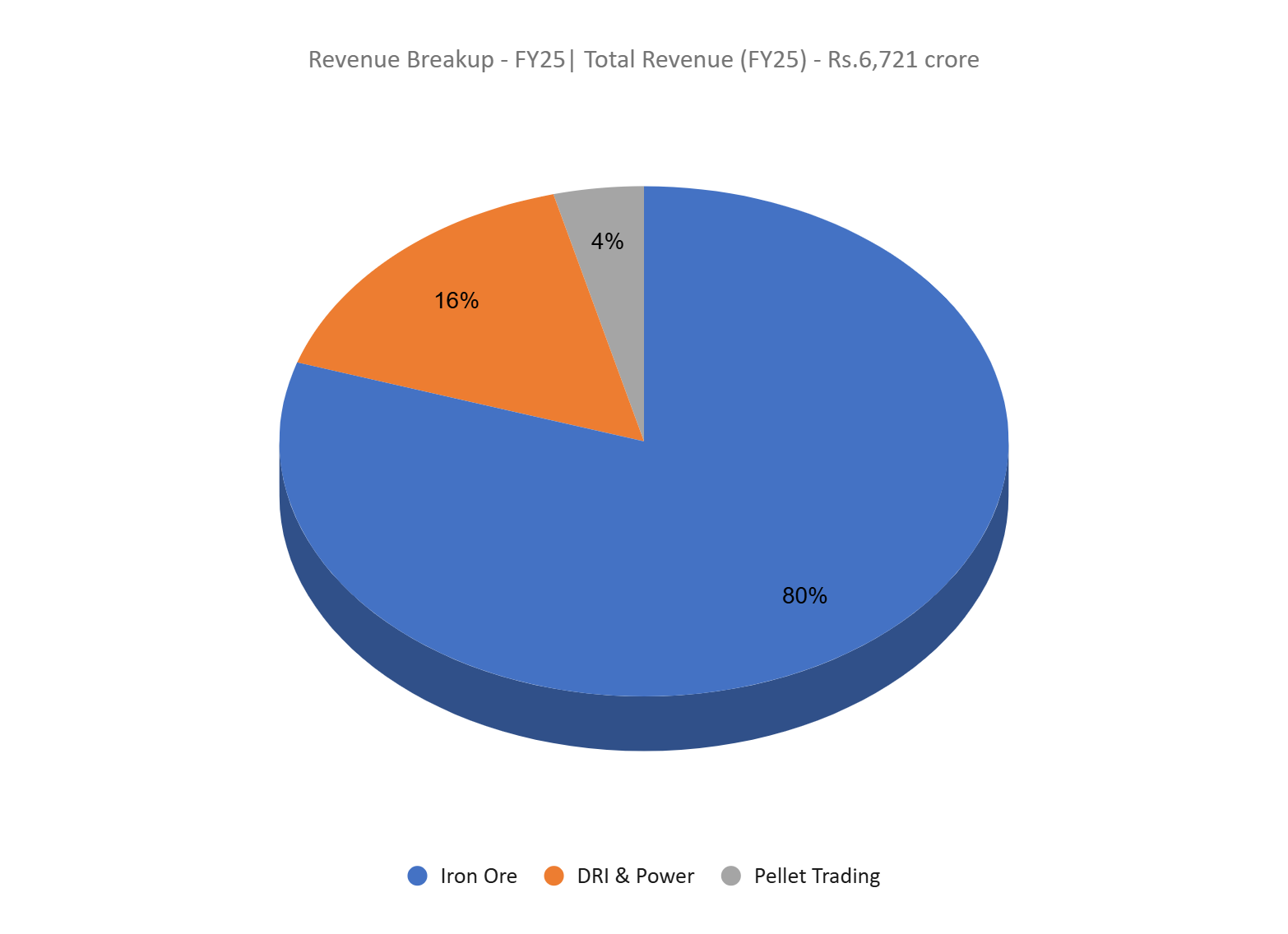

- Iron Ore – LMEL’s core upstream section comprising mining, extraction, and sale of calibrated ore and fines from its Gadchiroli operations. This section kinds the biggest contributor to income.

- DRI & Energy – The corporate produces direct decreased iron (DRI, together with captive energy technology that helps plant operations and allows incremental income by way of surplus gross sales. This built-in midstream section enhances margin stability and operational effectivity.

- Pellet Buying and selling – LMEL undertakes buying and selling of iron ore pellets, supplementing its personal pelletization initiatives and optimizing worth seize throughout the iron ore provide chain.

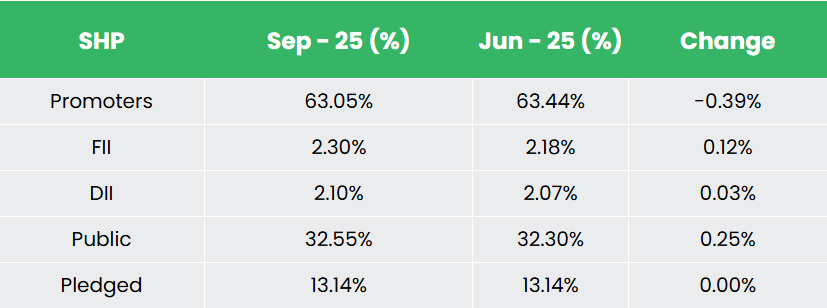

Subsidiaries: As of FY25, the corporate has 3 subsidiaries and no associates/joint ventures.

Funding Rationale

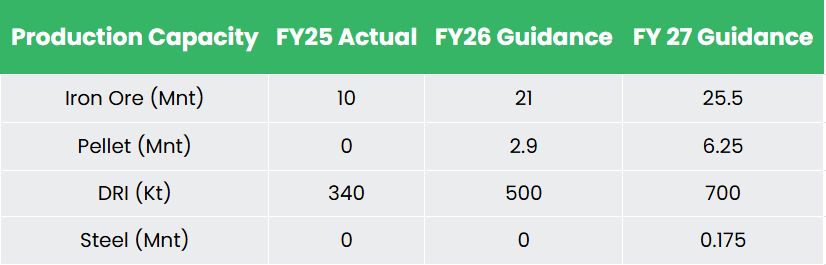

- Capability Enlargement – LMEL is executing an aggressive and value-focused growth program, backed by a lately enhanced 55 MTPA mining EC (environmental clearance), the corporate is transitioning from a pure iron ore miner into a completely built-in metals producer. Key initiatives embrace large-scale BHQ beneficiation modules (aiming for a 45MTPA enter by 2030, translating to a ~17MTPA output), expanded pellet capability, and commissioning of recent DRI items, every designed to transform low-value ore into high-margin, value-added merchandise. With these belongings phasing in from FY27 onwards, LMEL is positioning itself to structurally raise realizations, enhance product combine, and safe long-term development visibility throughout the iron ore–metal worth chain.

- Value Optimization & Structural Effectivity Levers – The corporate is embedding long-term price levers that instantly strengthen working margins. LMEL is setting up two slurry pipelines- an 85 km hall to Konsari and a 190 km hall to Chandrapur, which collectively are anticipated to cut back freight prices by Rs.500–600/t and Rs.800–1,000/t, respectively. These financial savings are structural as a result of slurry is considerably cheaper, safer, and extra dependable than street transport. Moreover, the corporate’s acquisition of Thriveni Earthmovers, one among India’s largest MDOs, enhances mining effectivity and is estimated to generate Rs.400–500/t of price financial savings on iron ore. With captive logistics, built-in energy provide, and improved beneficiation yields by way of the BHQ program, LMEL is constructing a sturdy low-cost working base. These initiatives materially widen the EBITDA unfold, cut back dependence on unstable third-party inputs, and enhance resilience by way of commodity cycles.

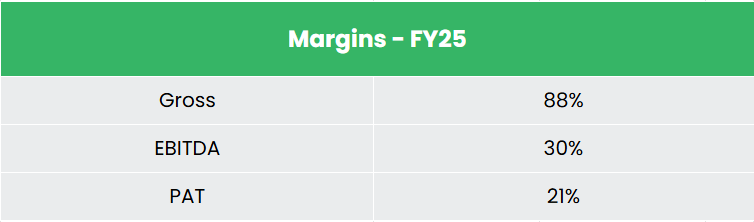

- Q2FY26 – Throughout the quarter, the corporate reported income of Rs.3,651 crore, a rise of 154% YoY in comparison with Rs.1436 crore in Q2FY25. Working revenue (EBITDA) elevated from Rs.445 crore in Q2FY25, to Rs.1,098 crore, marking a YoY development of 147%. Web revenue surged 88% YoY, from Rs.301 crore to Rs.567 crore. EBITDA margin in H1 of FY26 improved by 136 bps as in comparison with H1 of FY25, resulting from materialisation of price optimization efforts – slurry pipeline and better fastened price absorption resulting from worth added merchandise.

- FY25 – Throughout FY25, the corporate generated income of Rs.6,721 crore, a rise of three.02% in comparison with the FY24 income. Working revenue (EBITDA) grew by 12.5% YoY, to Rs.2,004 crore. The corporate reported a internet revenue of Rs.1,450 crore, a rise of 16.7% YoY.

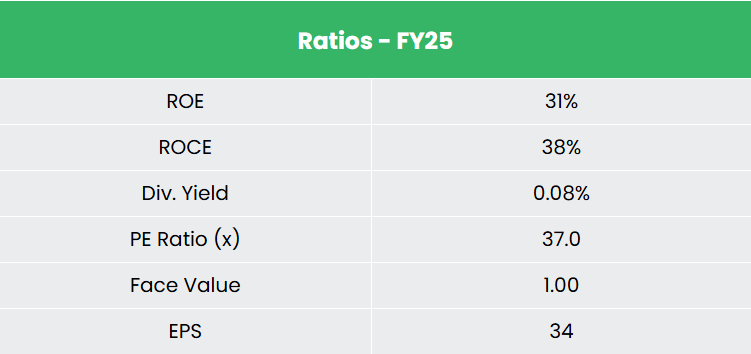

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 113% and 114% respectively between FY23-25. The corporate has a debt-to-equity ratio of 1.06. Common 3-year ROE and ROCE is round 46% and 66% for FY23-25 interval.

Trade

The mining sector performs a essential position in accelerating India’s financial development by supporting GDP growth, enhancing overseas change earnings, and strengthening downstream industries corresponding to development, infrastructure, automotive, and energy by way of dependable entry to important uncooked supplies. As the federal government intensifies its push on large-scale infrastructure together with roads, railways, airports, city housing, and industrial corridors, the demand for metal and iron ore is about to rise structurally. India is presently the second-largest producer of crude metal, the fourth-largest iron ore producer, and the biggest international producer of sponge iron (DRI), positioning the nation for sustained long-term development in ferrous supplies consumption. With rising home capability and powerful coverage help, each metal and iron ore demand are more likely to see multi-year momentum.

Progress Drivers

- 100% FDI permitted below the automated route, enabling international funding and know-how influx into mining.

- Minerals function the spine for core industries, making mining growth essential to broad-based industrial growth.

- Authorities initiatives corresponding to Gati Shakti, Make in India, PM Awas Yojana, and concrete infrastructure applications are set to considerably enhance metals and mining demand within the coming years.

Peer Evaluation

Rivals – NMDC Ltd and Gujarat Mineral Improvement Company Ltd.

In comparison with its friends, the corporate has delivered sturdy total efficiency with superior earnings development, and profitability.

Outlook

LMEL is poised to enter a structurally stronger development part as its value-added capacities start to commercialise over the following two to 3 years. For FY26, the corporate has outlined a capex program of roughly Rs.4,500–5,000 crore, normalizing at Rs.6,000-6,500 crore within the coming years. This funding cycle marks LMEL’s transition from a predominantly ore-sales mannequin to an built-in pellet–DRI–metal platform, which is predicted to materially enhance realisations and earnings high quality as downstream capacities ramp up. EBITDA margins are projected to stay strong, supported by higher-grade BHQ output, enhanced product combine, and price efficiencies from captive energy and logistics. With the primary BHQ module anticipated to start operations in FY27 and extra downstream belongings phasing in by way of FY28–FY29, LMEL is positioned for sustained quantity development, margin growth, and stronger money movement visibility over the medium time period.

Valuations

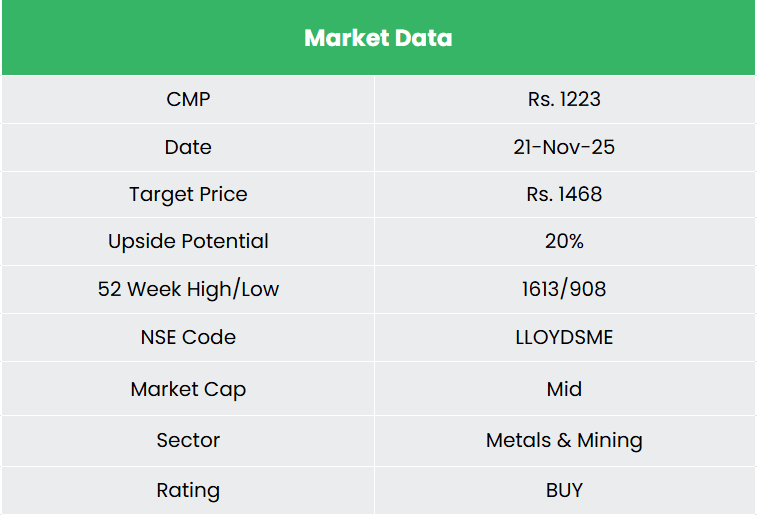

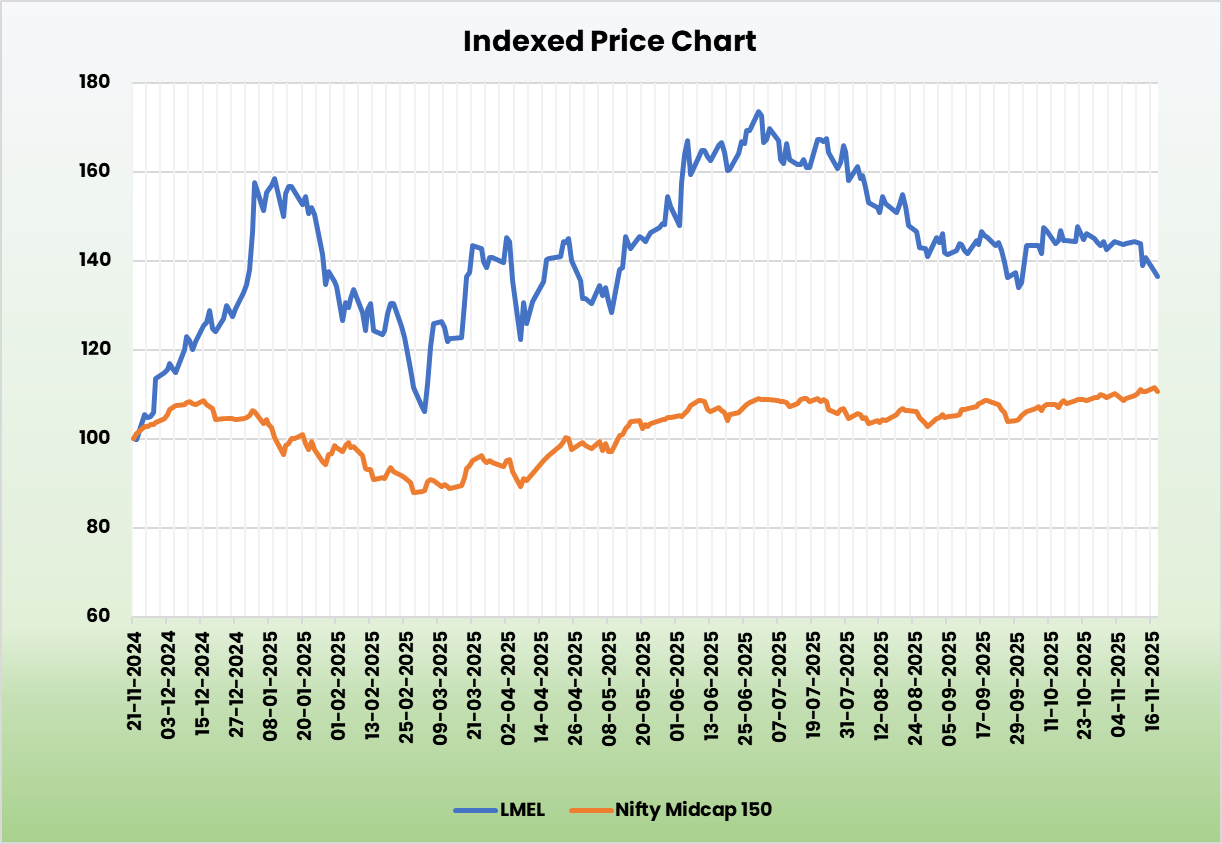

The corporate is nicely positioned to execute its large-scale growth plans, supported by sturdy moats, sustained price benefits, and clear multi-year earnings visibility. We suggest a BUY ranking within the inventory with the goal worth (TP) of Rs.1,468, 29x FY27E EPS. Be aware: We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully

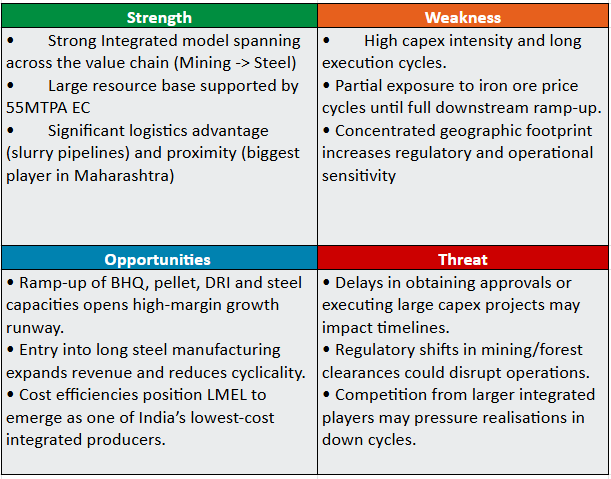

SWOT Evaluation

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you could like

Publish Views:

17

{kind=link}