Abstract: Abhijeet is investing Rs 12,500 a month into Sukanya Samriddhi and Rs 15,000 into fairness for targets which can be 17 to 26 years away. That sounds balanced. It is not, and the shortfall on the final milestone runs to almost a crore.

Abhijeet Prabhakar is 32. His daughter Ananya turned one a number of months in the past. He needs to fund three milestones for her: an undergraduate diploma on the age of 18, a postgraduate diploma at 22 and a marriage round 27.

He already places the total Rs 1.5 lakh a 12 months into Sukanya Samriddhi Yojana (SSY), a government-backed financial savings scheme particularly for lady kids, and has one other Rs 15,000 a month to spend money on mutual funds. His query: how ought to this be invested so no milestone catches him quick? And is there any profit to investing in Ananya’s identify slightly than his personal?

The second query has a brief reply. The primary one requires a reframe.

The issue most dad and mom miss

Abhijeet is making a mistake that almost all dad and mom make with out realising it. And that’s treating the SSY contribution and the mutual fund SIP as two separate selections when they’re actually one.

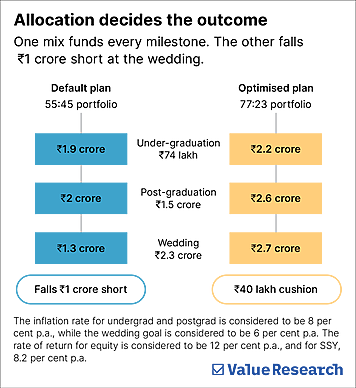

His Rs 1.5 lakh annual SSY contribution works out to Rs 12,500 a month right into a pure debt instrument. The Rs 15,000 SIP goes into fairness. Collectively, that’s an efficient 55:45 equity-to-debt break up for targets which can be 17 to 26 years away.

For a horizon this lengthy, that blend is just too conservative. The corpus will fall wanting the bigger milestones, the marriage particularly, the place the hole may run right into a crore or extra in tomorrow’s rupees.

The repair is conceptual earlier than it’s mechanical. SSY and the fairness SIP collectively kind a single portfolio with one mission: funding Ananya’s life. SSY is the debt sleeve. Mutual funds are the fairness sleeve. The correct query is what quantity to carry them in. And at 17 to 26 years, that proportion must be tilted closely towards fairness.

When you body it this fashion, most youngster planning questions reply themselves. Fund choice, tax effectivity, these turn out to be secondary. The primary determination is asset allocation. Get that proper and the remainder settles.

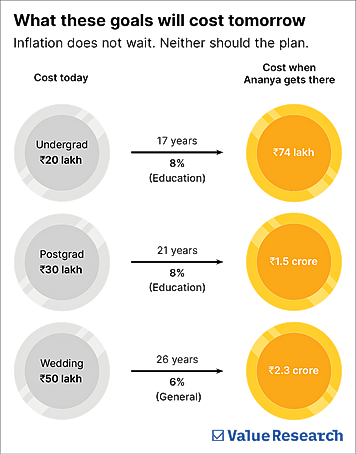

What these targets will really price

Earlier than deciding the combo, the targets must be clear.

Training in India is inflating at round 8 per cent a 12 months, effectively above headline inflation. A marriage may be tracked nearer to a traditional inflation charge of 6 per cent. Abhijeet’s three milestones, priced in tomorrow’s rupees, are considerably bigger than they appear right now.

The corpus doesn’t want to carry all three numbers directly. Every milestone attracts down a portion whereas the remainder retains compounding.

The correct portfolio for Ananya

The correct shift for Abhijeet is to cap his SSY contribution at Rs 75,000 a 12 months, half the present quantity, and redirect the freed Rs 6,250 a month into his fairness SIP, taking it from Rs 15,000 to Rs 21,250. The brand new break up sits at roughly 77 per cent fairness and 23 per cent debt.

For the fairness portion, a flexi-cap or multi-cap fund is the appropriate core holding. Each enable the fund supervisor to speculate throughout massive, mid and small-sized firms, which fits a protracted horizon effectively. Mid- and small-cap publicity generates greater long-term development potential; the large-cap portion supplies relative stability throughout downturns.

If Abhijeet nonetheless claims deductions beneath the previous tax regime, an ELSS fund can change the redirected Rs 6,250 every month, because it carries the identical 80C tax profit the SSY contribution did.

A 7 per cent annual step-up on the SIP, roughly in step with a modest annual wage enhance, retains contributions rising with earnings with out requiring a acutely aware determination annually.

The inflation charge for undergrad and postgrad is taken into account to be 8 per cent every year, whereas the marriage purpose is taken into account to be 6 per cent p.a. The speed of return for fairness is taken into account to be 12 per cent p.a., and for SSY, 8.2 per cent p.a.

Simulating the outcomes with the revised plan in an identical surroundings, 12 per cent annual development in fairness mutual funds and eight.2 per cent in SSY, all three milestones are funded, with a Rs 40 lakh cushion on the wedding ceremony.

The default 55:45 plan funds the primary two however falls Rs 1 crore quick on the final one. The allocation was the one factor that modified.

Two issues value understanding

The final mile. Fairness builds the corpus. It’s also the incorrect place to carry cash two years earlier than you want it. Start shifting the goal-specific portion right into a short-duration debt fund 24 to 36 months earlier than every milestone. Shift the undergraduate corpus when Ananya turns 15, the postgraduate corpus at 19 and the marriage corpus at 24. Many in any other case sound plans come aside at precisely this stage.

Investing in Ananya’s identify. Part 64(1A) of the Revenue Tax Act treats earnings earned in a minor’s identify because the mother or father’s earnings till the kid turns 18, which neutralises the supposed tax saving solely. There’s additionally operational friction: a minor PAN, necessary folio conversion at 18 and parent-as-guardian on each transaction. None of that is definitely worth the effort. Maintain the mutual funds in your individual identify, earmark the corpus on a monitoring sheet for Ananya’s targets and switch the models to her identify when she turns 18 through MF Central or the CAMS portal. SSY is the real exception. It’s, by design, a beneficiary account within the youngster’s identify.

The price of rising up is excessive and rising. The reply shouldn’t be a particular youngster plan or a bundled insurance coverage product. It’s the proper allocation, held for lengthy sufficient, with a transparent plan for the previous couple of years earlier than every milestone arrives.

That’s it. The whole lot else is noise.

Additionally learn: Course of earlier than efficiency

This text was initially revealed on Might 20, 2026.

")