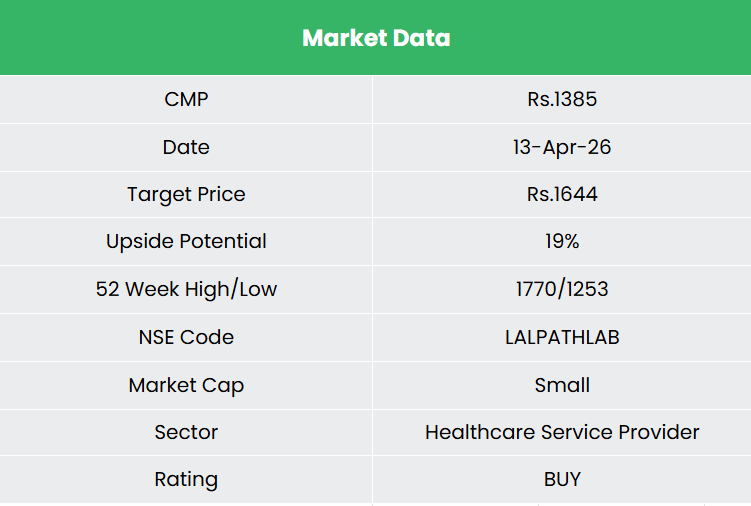

Dr Lal Pathlabs Ltd. – Increasing entry to superior diagnostics

Dr. Lal PathLabs Restricted, integrated in 1995 and headquartered in New Delhi, is India’s largest shopper healthcare model in diagnostic providers by income. The corporate operates throughout pathology and radiology diagnostics by way of a pan-India hub-and-spoke community of 298 medical laboratories (together with a Nationwide Reference Lab in Delhi and Regional Reference Labs in Kolkata, Bengaluru, and Mumbai), 6,607 Affected person Service Facilities (PSCs), and 12,365 Choose-up Factors (PUPs) as of FY25. DLPL provides a complete take a look at menu spanning 385 take a look at panels, 3,172 pathology assessments, and 1,455 radiology and cardiology assessments, with specialised verticals in genomics (Genevolve), reproductive diagnostics (L-CoRD), and auto-immune problems (L-ACE).

Merchandise and Providers

The corporate supplies a wide selection of diagnostic and preventive healthcare providers, together with routine blood assessments, specialised screenings (akin to thyroid, diabetes, liver, kidney, and most cancers assessments), full physique checkups, infectious illness diagnostics (like COVID-19, dengue, and tuberculosis), and superior assessments supporting continual illness administration, fertility assessments, and autoimmune problems.

Subsidiaries: As of FY25, the corporate has 8 subsidiaries.

Funding Rationale

- Quantity restoration and pricing optionality driving earnings inflection – The corporate’s earnings progress seems poised for acceleration, with key levers already falling into place even when the total influence is but to be seen. Affected person quantity progress, which bottomed at 2.7% two years in the past, has been steadily recovering with YTD FY26 at 4.4%. This restoration is going on forward of the total influence of 600 – 800 new assortment centres added yearly and earlier than the Tier 3/4 franchisee community reaches important mass, and crucially, earlier than any value improve. DLPL has not raised costs in over three years and has truly simply lower costs to move on GST enter advantages to sufferers, making a value hike within the subsequent 3/4 quarters a near-certainty as indicated by the administration. When applied, this pricing lever will coincide with an already bettering base, income per affected person is rising at 7.7% YoY pushed by higher take a look at combine, whereas assessments per affected person have elevated from 2.97 to three.11, indicating profitable upselling and menu growth. Combining a 2 – 3% quantity uplift with a possible 3 – 5% value improve is anticipated to drive general income progress to fifteen – 17%, versus the present 11 – 12% baseline. With structurally sustainable EBITDA margins of 27 – 28%, this incremental income is anticipated to translate effectively into earnings. Additional, a debt-free steadiness sheet with ₹1,411 crore in money ensures no curiosity drag, enhancing revenue conversion.

- Excessive ROCE franchise with premium valuation justified by high quality – A key spotlight from the Q3FY26 investor presentation is the reported ROCE of 48% (excluding money and investments), which supplies a extra related measure of core working effectivity. That is supported by the development in fastened asset turnover from 10.1x in FY23 to 12.3x in FY25, indicating higher utilisation of the asset base, pushed by the hub-and-spoke mannequin and franchisee-led growth. The moderation to 7.2x in 9MFY26 displays a better capex section (~₹150–160 crore vs. a normalised ₹50–70 crore), primarily in direction of initiatives akin to Sovaaka, radiology centres, and precision diagnostics. As the present funding cycle stabilises, asset turns are anticipated to normalise, supporting working leverage. The corporate’s community, together with NABL-accredited labs, CAP-accredited reference labs, and in-house high quality management programs, additionally helps its positioning within the diagnostics section. The important thing monitorable stays the interpretation of present investments into sustained progress and return ratios.

- Q3FY26 – Income got here in at ₹660 crore, up 10.6% YoY, pushed primarily by pattern quantity progress of seven.8% and income per affected person rising 7.7% to ₹927 (mix-led, not pricing). EBITDA earlier than distinctive gadgets stood at ₹179 crore, up 16.3% YoY, with margins increasing 140 bps to 27.2%. PAT declined 6.8% YoY to ₹91 crore on account of a one-time ₹30 crore cost associated to new labour code implementation; adjusting for this, underlying profitability improved.

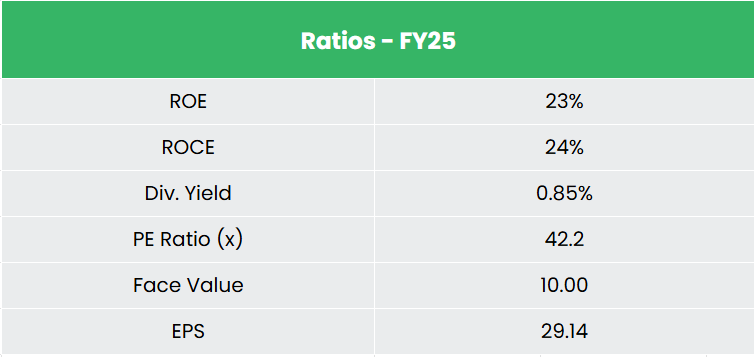

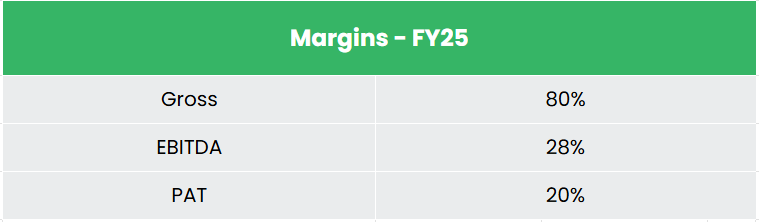

- FY25 – Income was ₹2,461 crore, up 10.5% YoY. EBITDA stood at ₹696 crore with margins at 28.3%, posting a 14% YoY progress. PAT grew 36% YoY to ₹492 crore, implying a 20.0% margin.

- Monetary Efficiency – The three-year income and internet revenue CAGRs stand at 6% and 12% respectively (FY23–25). Notably, TTM income and internet revenue CAGRs have improved to 11% and 32% respectively. The three-year common ROE and ROCE are 20% and 24%, and the corporate carries a debt-to-equity ratio of 0.07x.

Business

Healthcare spending in India stood at ~3.3% of GDP in 2022 and is anticipated to pattern upward over the medium time period, supported by a Union Finances FY26 – 27 allocation of ₹1.04 – 1.06 lakh crore (~9.8% YoY progress). The hospital section, valued at ~US$126 billion in FY24, is projected to develop at ~8% CAGR to ~US$193.6 billion by FY32, with a structural mattress shortfall of ~3 million beds offering long-term demand visibility for organised personal gamers. Hospital mattress capability can also be anticipated to increase at ~8% CAGR by way of 2030. Progress is prone to be led by Tier II and III cities, the place demand is projected to develop at 16 – 18% CAGR, forward of metro markets at 12 – 14%, indicating the subsequent section of growth. Moreover, a rising geriatric inhabitants and rising disposable incomes are driving greater healthcare consciousness and spend, significantly in direction of preventive care and high quality diagnostics, supported by rising recognition of the significance of well timed and correct testing.

Progress Drivers

- Beneficial FDI Coverage: 100% FDI is permitted below the automated route for greenfield hospital initiatives; cumulative FDI inflows into hospitals and diagnostic centres reached US $12.25 billion between April 2000 and June 2025.

- Rising Demand from Demographics and Illness Burden: Life expectancy is projected to succeed in 84 years by 2045, and life-style illnesses now account for ~50% of in-patient spending, driving sustained demand for specialised care.

- Authorities Initiatives – Along with this, the expansion of the diagnostic trade in India was pushed by supportive insurance policies and schemes launched by the Indian Authorities, akin to, Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) and the PM Ayushman Bharat Well being Infrastructure Mission (ABHIM).

Peer Evaluation

Opponents – Vijaya Diagnostic Centre Ltd, Metropolis Healthcare Ltd, and so on.

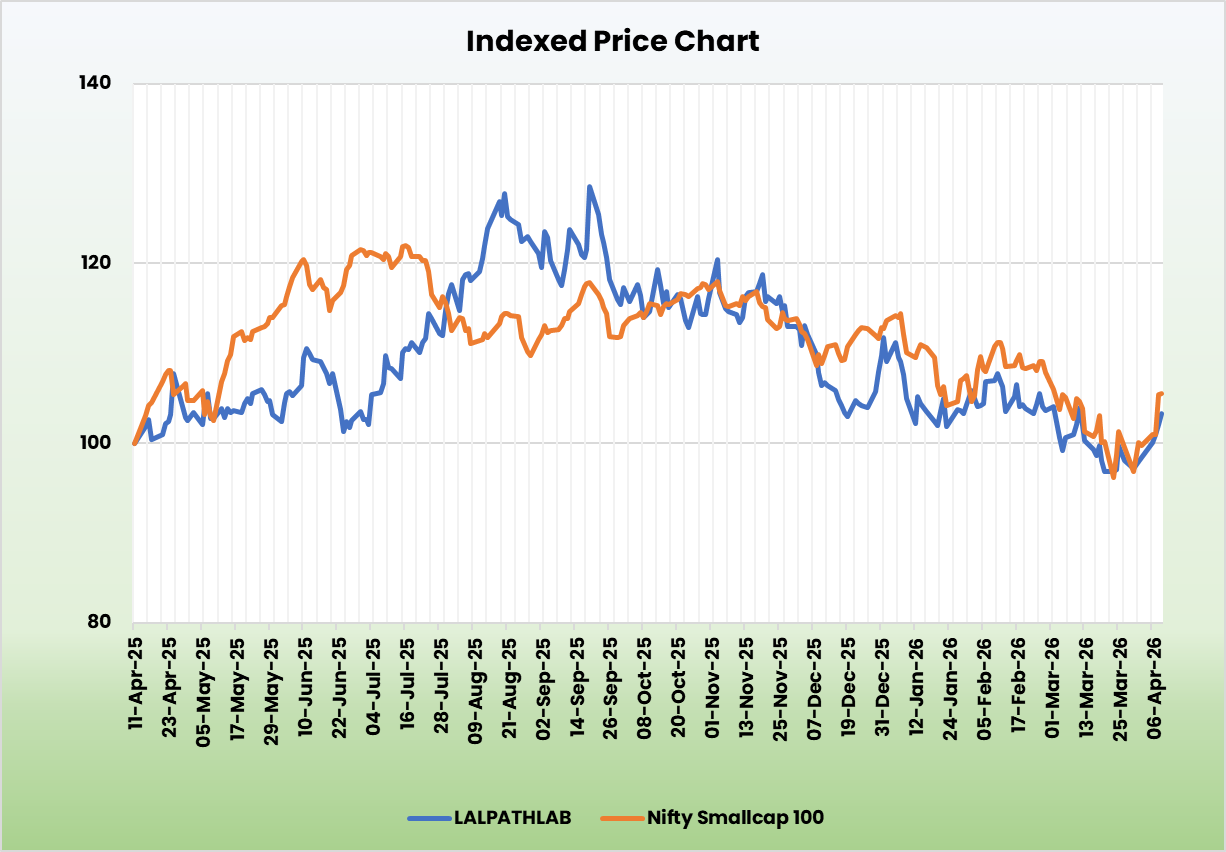

In comparison with its friends, the corporate demonstrates a superior return profile and asset effectivity and is buying and selling at a extra enticing valuation regardless of of trade main internet revenue margins.

Outlook

CARE upgraded the corporate’s credit standing from AA to AA+ in March 2026, reinforcing steadiness sheet power, with affected person quantity progress remaining the important thing near-term monitorable. India’s diagnostics trade is approaching a structural shift, with organised gamers anticipated to extend market share from ~20% in FY24 to ~30% by FY28, positioning DLPL nicely given its scale, model legacy, and in depth community of labs and assortment centres. The near-term earnings outlook is supported by 3 converging drivers – quantity restoration, pricing actions, and working leverage which is anticipated to play out over the subsequent 12 – 18 months. Key monitorables embrace sustained quantity restoration (significantly Q4FY26 traits), timing of value hikes, potential M&A in South India to deal with geographic gaps, scalability of the Sovaaka mannequin, and enter value pressures from foreign money actions.

Valuations

We consider the structural rise in healthcare demand in India positions Dr Lal PathLabs Ltd nicely to leverage its market management, supporting sustained progress momentum over the medium to long run. We suggest a BUY score within the inventory with the goal value (TP) of Rs.1,644, 50x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

SWOT Evaluation

| Power | Weak point |

|

|

| Alternatives | Threats |

|

|

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Submit Views:

1,171

")

{kind=link}