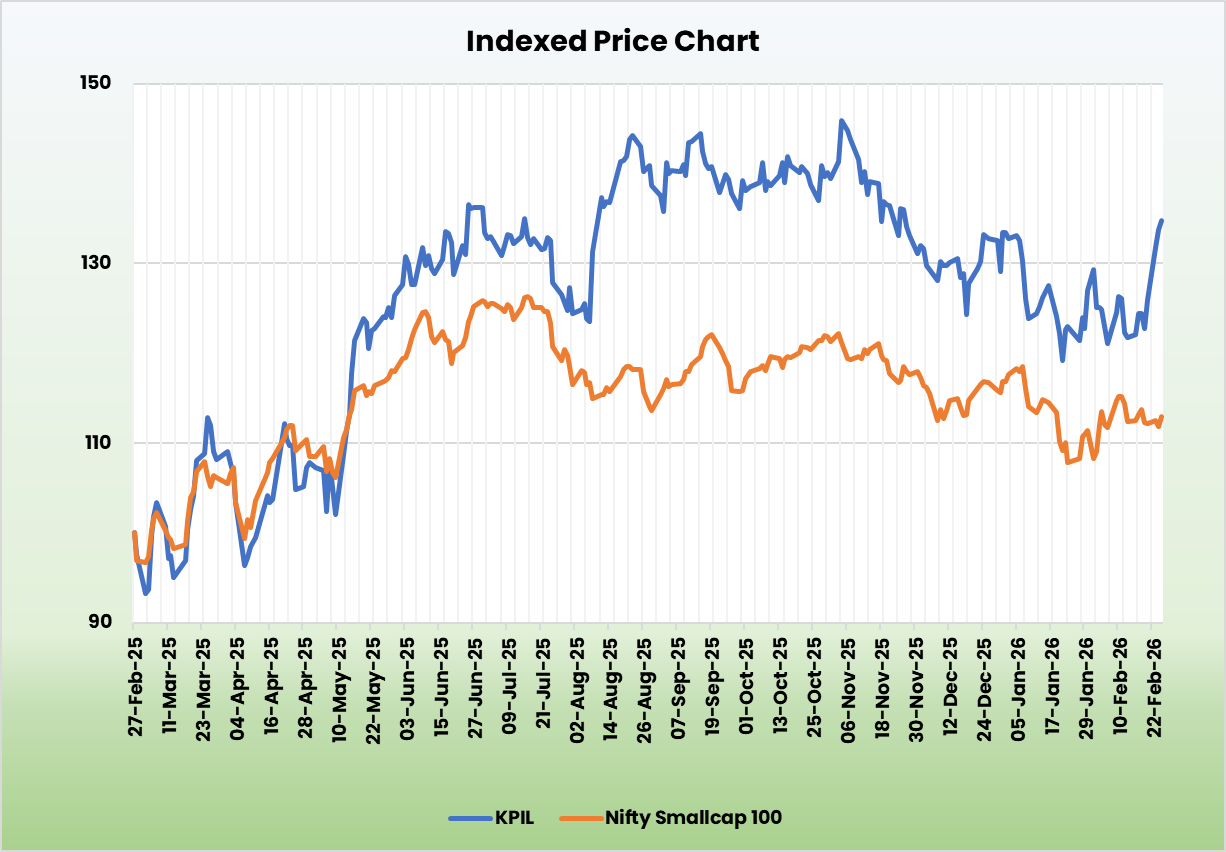

Kalpataru Initiatives Worldwide Ltd. – Propelling Worth Accretive Development Globally

Kalpataru Initiatives Worldwide Restricted (KPIL), integrated in 1981 and headquartered in Mumbai, is a globally diversified Engineering, Procurement and Development (EPC) firm working throughout six enterprise verticals spanning power and infrastructure. The corporate has presence throughout 76 international locations with dwell tasks in 30+ nations, and executes work throughout 5 continents, positioning it among the many high EPC gamers globally within the T&D house outdoors China. KPIL employs over 10,900 individuals throughout 40+ nationalities. In-house capabilities span design, engineering, procurement, development, and operations & upkeep, and are supported by one of many largest transmission tower manufacturing setups on this planet with a commissioned capability of 240,000 MTPA throughout two vegetation in India.

Merchandise and Providers

The corporate offers a broad vary of providers throughout its diversified enterprise segments.

- Energy T&D – Transmission traces, substation, transmission tower manufacturing, photo voltaic EPC, tower testing, inexperienced hydrogen & derivatives.

- Oil & Fuel – Course of pipeline, cross nation pipeline, refineries & fertiliser vegetation.

- Buildings and Factories – Residential and business buildings, knowledge centres, airports, industrial vegetation and factories.

- Water and Irrigation – Water provide, irrigation, desalination, consumption and therapy and so on.

- City Infra – Roads and highways, elevated metro rail, tunnelling, flyovers, metro rail and so on.

- Railways – Observe laying, signalling and telecom, stations facility, rail over bridges, and so on.

Subsidiaries – As of FY25, the corporate has 22 subsidiaries and 1 three way partnership.

Funding Rationale

- Robust Order Visibility Anchored by Core Segments – The corporate’s strong order e-book of Rs.63,287 crore offers wholesome multi-year income visibility, supported by Rs.19,456 crore of order inflows in FY26 YTD, making certain sustained execution momentum over the following three years. With ~70% of the order e-book concentrated within the T&D and B&F segments – which proceed to drive scale and profitability – latest wins mirror sturdy positioning in giant, strategic tasks throughout these core verticals. Order inflows stay largely domestic-led (74%), complemented by worldwide diversification (26%), whereas further L1/favourably positioned tasks of ~Rs.7,000 crore provide near-term conversion potential. Notably, the order e-book has doubled over the previous 4 years, underlining constant mission wins and reinforcing long-term development visibility.

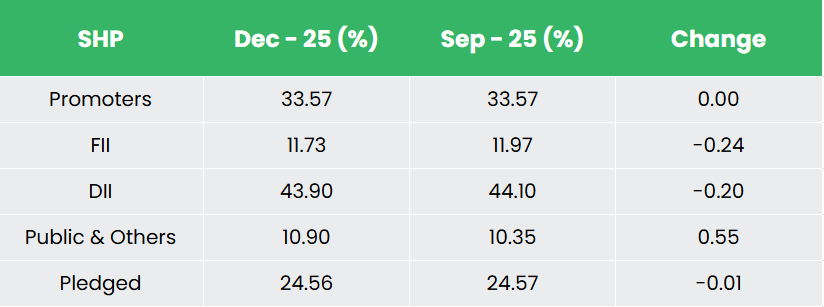

- Strengthening Steadiness Sheet Supporting Scalable Development – The corporate continues to reinforce its stability sheet power via bettering working capital self-discipline and prudent debt administration, supported by higher collections from the water enterprise and regular execution of enormous residential tasks. Internet working capital has improved to 79 days on the consolidated degree and 97 days at standalone thereby outperforming the year-end goal of 100 days, reflecting disciplined bidding and well timed mission supply. Consolidated and standalone web debt declined by 29% and 16% QoQ to Rs.2,240 crore and Rs.1,849 crore respectively as of December 2025, pushed by improved operational efficiency and money circulate visibility, with additional discount anticipated in This autumn. Moreover, the divestment of the Vindhyachal Highway asset in January 2026 indicators a strategic shift away from non-core companies, enabling capital redeployment into core EPC segments and supporting capital return ratio enchancment.

- Robust Segmental Efficiency Driving Execution Momentum – The corporate continues to construct sturdy traction throughout its core T&D and B&F segments, supported by strong order inflows and wholesome execution. The T&D enterprise stays a key development driver, with order backlog exceeding Rs.25,752 crore as of December 2025 (+12% YoY) and income rising 37% YoY in 9MFY26 to Rs.8,992 crore, led by sturdy execution throughout India and key worldwide markets comparable to Sweden. Sustained investments in renewable integration and grid infrastructure, backed by an estimated Rs.90,000 crore annual capex pipeline in India by Energy Grid Company of India Ltd, proceed to strengthen visibility. The B&F phase has additionally delivered sturdy efficiency, with order inflows crossing Rs.10,911 crore in FY26 YTD and order e-book rising 40% YoY to Rs.18,596 crore, pushed by wins in knowledge centres, residential, healthcare and industrial tasks. Further development help comes from the Oil & Fuel phase (+58% YoY income development) and Railways (+15% YoY), whereas bettering collections within the water phase are anticipated to help restoration in execution momentum.

- Q3FY26 – Throughout the quarter, the corporate reported consolidated income of Rs.6,665 crore, up 16% YoY in comparison with Rs.5,732 crore in Q3 FY25. EBITDA grew 7% YoY from Rs.479 crore to Rs.513 crore, although EBITDA margin contracted 70bps YoY to 7.7%. Internet revenue stood at Rs.149 crore, up 7% YoY from Rs.140 crore in Q3 FY25.

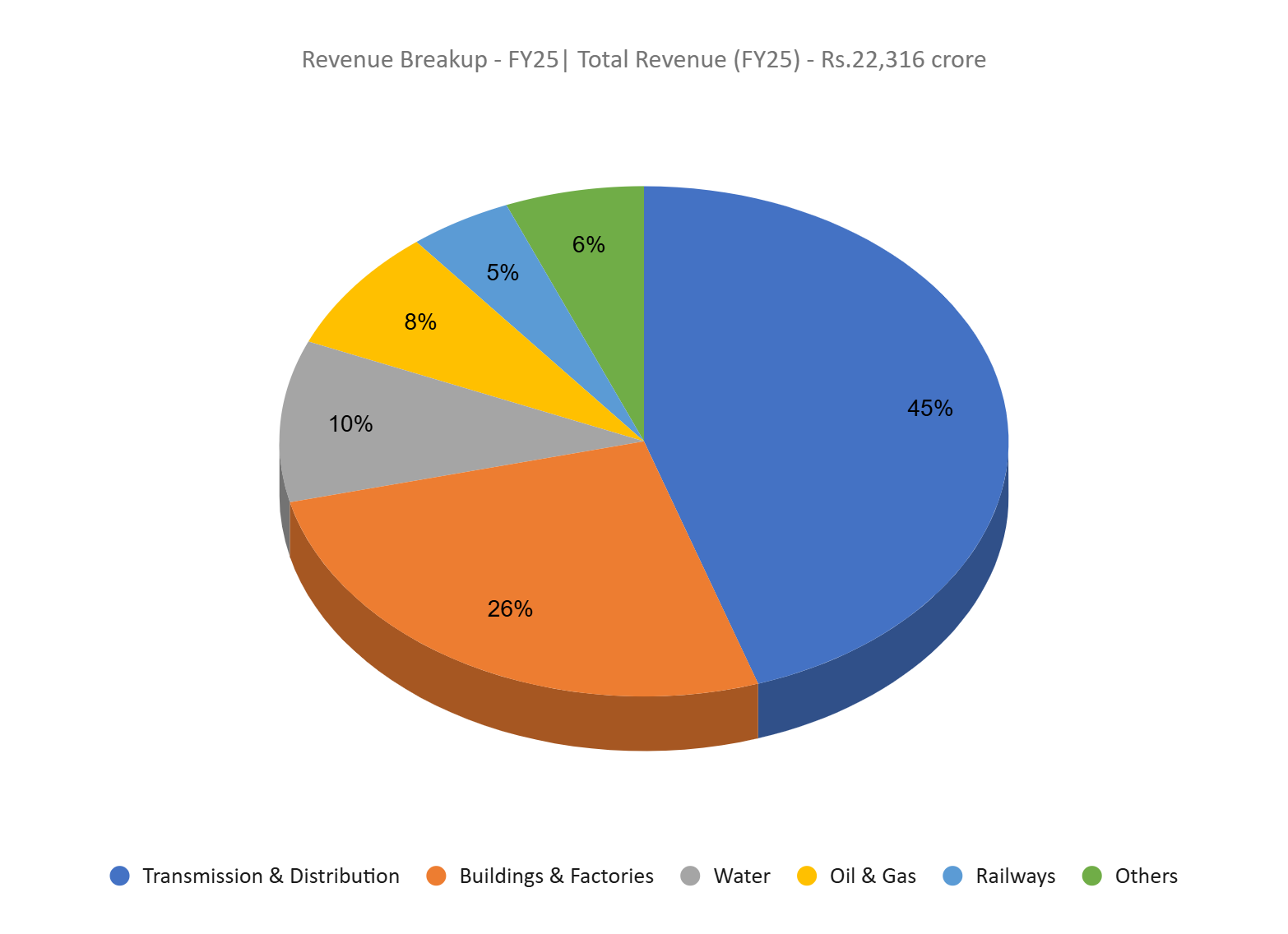

- FY25 – Throughout FY25, the corporate reported consolidated income of Rs.22,316 crore, representing a ~14% YoY improve. EBITDA stood at Rs.1,834 crore, up 13% YoY, and revenue after tax was recorded at Rs.567 crore, posting a development of 10% YoY.

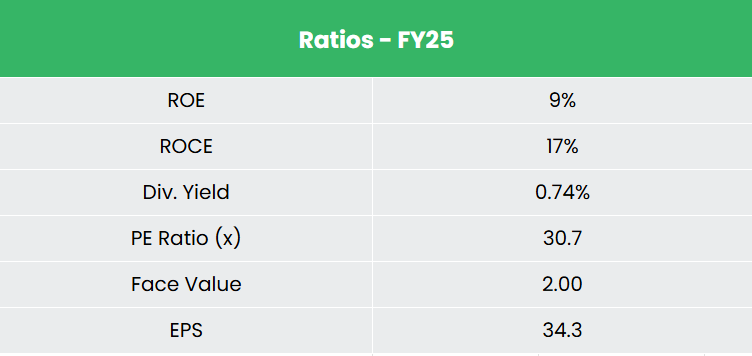

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 15% and 14% respectively between FY23-25. Notably, the corporate reported TTM income and web revenue development charges of 25% and 62%, respectively. The corporate has a debt-to-equity ratio of 0.69x, and the 3-year common ROE and ROCE are round 10% and 15% for FY23-25 interval.

Trade

The Indian infrastructure and energy transmission sector sits on the coronary heart of the nation’s financial transformation, underpinning key end-markets. India’s whole put in electrical energy capability reached 505 GW as of October 2025, with renewable power now accounting for practically 50% of the put in base together with 129.9 GW of photo voltaic and 53.6 GW of wind – driving huge demand for brand spanking new transmission and evacuation infrastructure. As of Could 2025, transmission traces of 220 kV and above measured 4,94,994 circuit kilometres, and India plans to speculate Rs.9,15,920 crore by 2032 solely in further transmission traces to help its objective of practically tripling clear energy capability. On the civil infrastructure aspect, India’s Nationwide Highways community expanded to 1,46,342 km in FY25 with 10,660 km constructed through the yr, whereas Indian Railways earned a file Rs.2,62,000 crore (US$30.58 billion) in FY25 income with a budgetary CAPEX of Rs. 2,65,200 crore (US$31.43 billion) for FY26. India is anticipated to spend Rs.143 lakh crore (US$1,727 billion) on infrastructure throughout seven fiscals via 2030, greater than double the Rs.67 lakh crore spent within the previous seven years, positioning the nation as one of many fastest-growing infrastructure markets globally.

Development Drivers

- Infrastructure capex outlay – Union Funds 2025-26 raised the capital funding outlay for infrastructure to Rs.11,21,000 crore (US$128.64 billion), equal to three.1% of GDP, with file allocations for roads and railways driving a sustained EPC mission pipeline

- Energy transmission growth pushed by renewable scale-up – India’s 500 GW non-fossil gasoline goal by 2030 necessitates Rs. 9,15,920 crore (US$107 billion) in new transmission investments by 2032.

- Liberalised FDI and coverage help – 100% FDI is permitted underneath the automated route within the energy sector, with cumulative FDI in development infrastructure reaching Rs.3,15,768 crore (US$36.85 billion) between April 2000 and June 2025.

Peer Evaluation

Rivals – IRB Infrastructure Builders Ltd, Techno Electrical & Engineering Firm Ltd, and so on.

In comparison with friends, KPIL demonstrates sturdy return ratios and superior earnings high quality, with a CFO/PAT of two.95x indicating constant money conversion relative to reported earnings. The corporate’s diversified revenue-mix throughout six enterprise verticals and geographies offers extra secure efficiency via sectoral cycles, lowering dependence on any single end-market.

Outlook

The corporate stays on monitor to ship its FY26 development targets, supported by a stronger stability sheet, bettering mission combine and disciplined execution. The finished divestment of a non-core asset and continued discount in promoter pledge mirror a sharper deal with capital effectivity and governance. With a gentle influx of higher-margin tasks, PBT margins have already improved by 110 bps (consolidated) and 80 bps (standalone) in 9MFY26, forward of full-year steering. A sturdy order backlog, primarily in T&D and B&F, offers sturdy income visibility whereas supporting margin growth. Internet debt discount and environment friendly working capital administration proceed to reinforce monetary flexibility regardless of Rs.500+ crore capex deployed through the yr. The corporate expects ~25% income development in FY26, together with earnings enchancment of a minimum of 100 bps on the consolidated degree and 50 bps at standalone and stays assured of reaching consolidated EPS exceeding Rs.50 for the yr.

Valuations

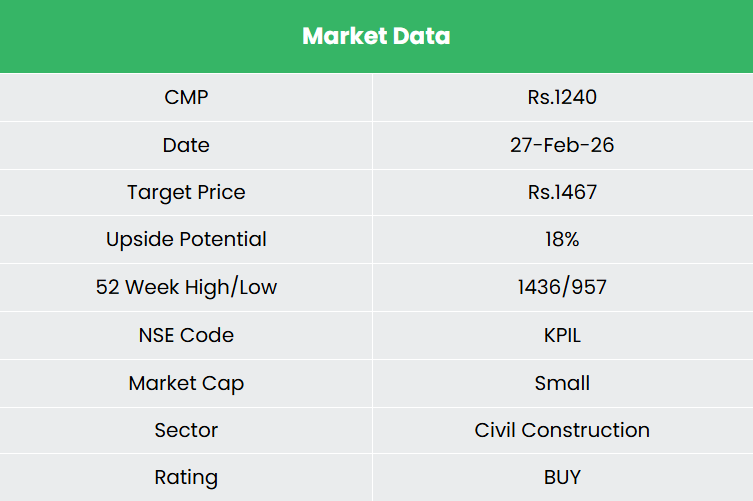

We consider the corporate presents a compelling play on margin-accretive development backed by a strengthening stability sheet, bettering mission combine and robust execution visibility. We suggest a BUY score within the inventory with the goal value (TP) of Rs.1,467, 26x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

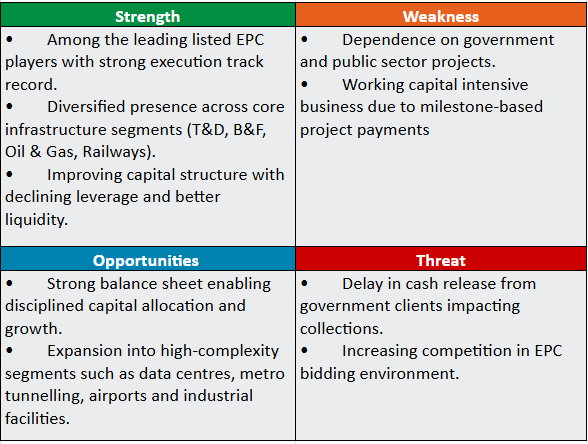

SWOT Evaluation

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you might like

Publish Views:

1,392

{kind=link}