That stated, the wealth and asset administration segments – with enormous development runways – additionally proceed to carry out nicely and help the general enterprise. However what’s actually driving this shift, and what alternative might form the subsequent section of development?

We unpack these particulars on this piece.

Broking below stress, distribution good points momentum

The wealth administration section contains brokerage, distribution, and lending.

Brokerage has historically been a serious contributor to this section’s revenues, accounting for 40% of the entire in FY25. Because the main full-service brokerage home, Motilal holds a 7.6% market share in money and eight.5% in F&O turnover. It additionally maintains the very best common income per consumer within the trade.

Additionally learn | Maruti Suzuki’s battle for dominance: Is the EV pivot sufficient to reclaim market share?

Nonetheless, brokerage income is below stress owing to a decline in broking quantity amid a unstable market and stricter F&O guidelines. On account of these, broking income fell 37% to ₹166 crore within the March quarter (Q4FY25).

This decline was partially offset by a 140% soar in distribution earnings to ₹187 crore. Whereas administration continues to prioritise the broking enterprise, there may be an rising shift towards distributing monetary merchandise.

Why the pivot to distribution is smart

Motilal sees vital potential in its distribution enterprise, primarily as a result of low cross-sell ratio of below 6% amongst its 40 lakh current shoppers. This means a considerable development alternative, and the low penetration highlights a powerful case for enlargement.

To faucet this, Motilal continues to increase its community of relationship managers (RMs)—a development seen throughout the trade—and is focusing on a threefold improve of their numbers over the subsequent few years. There may be additionally room for productiveness good points as solely 33% of Motilal’s present RMs have greater than three years of expertise. As these numbers improve, so ought to productiveness, driving development in property below administration (AUM).

This enlargement was a key driver of the sturdy development in distribution property in FY25. Distribution AUM accounted for 12% of its segmental AUM at ₹31,551 crore – up 33% from the earlier 12 months – as web gross sales elevated fourfold.

For Motilal Oswal, the distribution enterprise might show to be a key development driver because it generates recurring, annuity-like revenues. Distribution now accounts for 19% of the section’s income, up from 11% in FY24, whereas brokerage decreased from 47% to 42%. As this shift continues, steady recurring earnings from distribution might offset a number of the cyclicality of broking.

The chance on this house stays massive. In line with the Knight Frank Wealth Report, the variety of ultra-high-net-worth people in India is predicted to extend by 50% – from 13,263 in 2023 to 19,908 by 2028 – outpacing the worldwide development charge of 28%. This presents a possibility price about $2.5 trillion.

Regaining misplaced floor in asset administration

Motilal’s asset administration AUM elevated 63% from March 2024 to March 2025, when it stood at ₹1.33 trillion. Mutual funds comprised 93% of this, whereas the remaining got here from portfolio administration providers (PMS) and different funding funds (AIFs).

This development got here regardless of subdued market efficiency and was pushed by sturdy investor participation. This was mirrored in a fourfold improve in gross flows, a threefold rise in SIP flows, and a ninefold improve in web flows over the 12 months.

A key issue behind this momentum was Motilal’s sturdy maintain over particular person AUM, which accounted for 88% of the entire, nicely above the trade common of 60%. The corporate additionally improved its market positioning by rising the share of distinctive folios from 6% in March 2024 to 14% in March 2025.

Fund efficiency additionally performed a key function, as 90% of its methods outperformed the benchmark (FY25), putting them within the high quartile. This, coupled with the launch of latest funds, boosted product sales and folio additions. In consequence, Motilal regained misplaced floor, with its SIP market share doubling from 1.5% to three.2% in the course of the interval, and product sales share rising from 1.6% to 4.3%.

Additionally learn | Drive Motors This fall: Sturdy present, however can the momentum final?

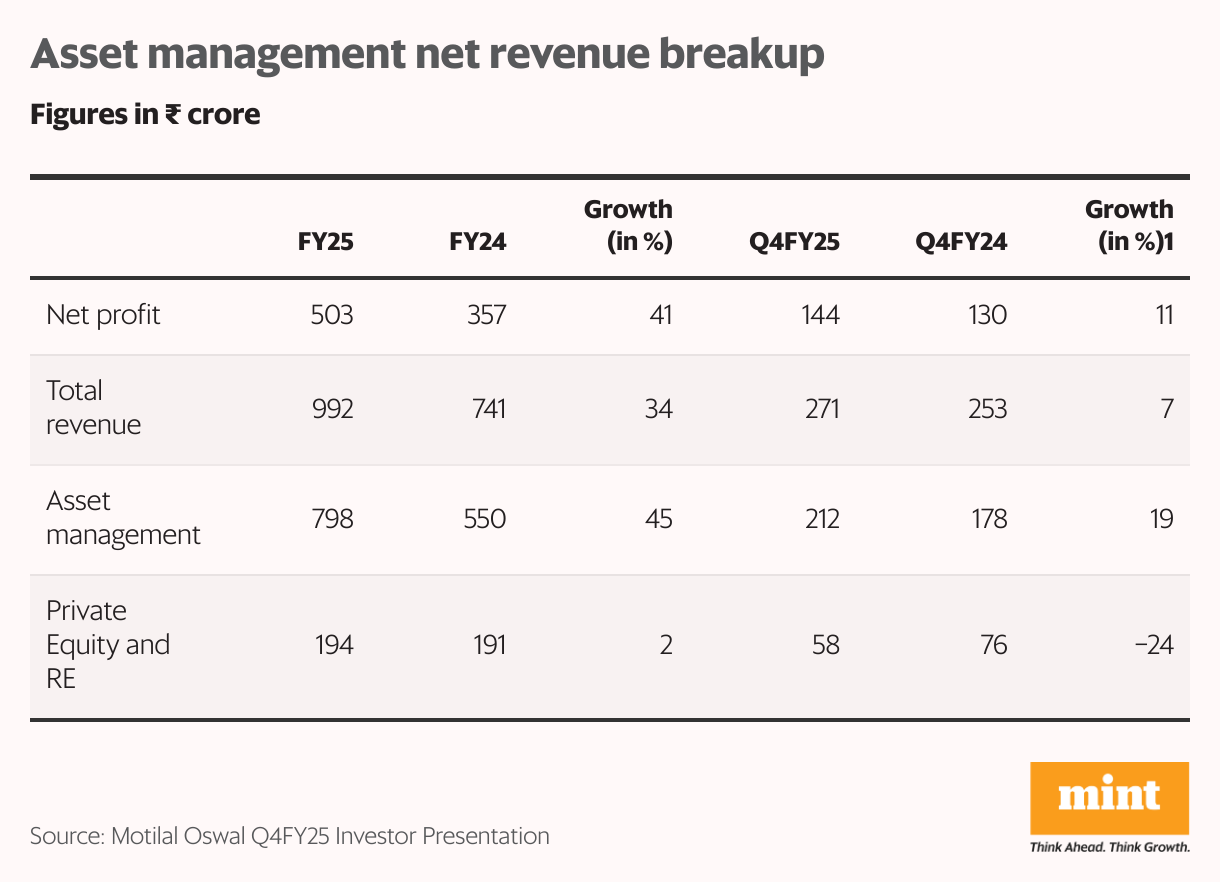

On the monetary facet, the section delivered a powerful full-year efficiency. Income rose 34% to ₹992 crore whereas web revenue grew 41% to ₹503 crore. Nonetheless, momentum slowed in Q4FY25, with income rising solely 7% and web revenue rising simply 11%.

Trying forward, Motilal’s precedence is rising fairness AUM, primarily by direct channels. It continues to put money into distribution infrastructure, and increase its gross sales crew and department footprint. These initiatives, backed by constructive trade tendencies and under-penetration of mutual funds, are anticipated to drive long-term development regardless of near-term headwinds.

Personal wealth administration

Personal wealth administration serves high-net-worth (greater than ₹5 crore) and ultra-high-net-worth (greater than ₹25 crore) shoppers. This section’s AUM grew 16% in FY25 to ₹1.4 trillion, with web gross sales doubling in the course of the 12 months.

Section income grew 30% to ₹920 crore in FY25, pushed by a 32% improve in recurring income and a 29% improve in transaction-based income. Web revenue grew 28% to ₹321 crore. Nonetheless, quarterly efficiency remained weak, with income and web revenue declining 5% and 6%, respectively, from the identical quarter of the earlier 12 months.

Personal wealth administration holds immense potential over the long run, and Motilal, regardless of being a frontrunner within the trade, lags within the personal wealth section. Nonetheless, the corporate believes that areas past tier-1 cities maintain sturdy potential. It’s trying to increase its presence in these underpenetrated places – like others within the trade – whereas increasing its product choices.

The corporate expects to proceed to develop market share in AUM past FY25 ranges, pushed by sturdy flows, development in RMs and consumer acquisitions. This development would end in wholesome income and revenue enlargement within the personal wealth and asset administration companies.

Funding banking posts resilient development

Motilal’s funding banking enterprise noticed sturdy development in FY25, finishing 39 offers in the course of the 12 months. It topped the certified institutional placement league desk and ranked third in preliminary public choices.

Additionally learn: Samhi’s GIC deal might speed up development. May a valuation rerating comply with?

With offers price ₹51,000 crore throughout FY25, web income grew 37% to ₹598 crore, whereas web revenue grew 31% to ₹258 crore. This development was nicely supported by a 42% improve in income and a 43% rise in revenue in Q4FY25.

Going ahead, administration expects the enterprise to ship sturdy development regardless of market volatility. To this finish, it has appointed a brand new management crew, and with its enviable deal pipeline, expects to enhance its rank in funding banking.

Truthful worth losses hit quarterly efficiency

The March quarter was a setback for Motilal Oswal. The corporate swung into the crimson, reporting a web lack of ₹64 crore, in comparison with a revenue of ₹724 crore in the identical quarter of the earlier 12 months. This marked its first quarterly loss in 5 years, the final being in Q4FY20.

The loss was primarily pushed by a fair-value lack of ₹430 crore, a pointy reversal from the fair-value achieve of ₹424 crore in Q4FY24. This additionally affected its income, which fell 45% to ₹1,190 crore within the quarter.

Annual efficiency stayed sturdy

Nonetheless, the poor This fall was offset by stronger efficiency within the first 9 months of FY25. Income elevated 17% to ₹8,339 crore in FY25, albeit at a gradual charge, whereas web revenue rose simply 3% to ₹2,508 crore, weakened by decrease income.

As a capital markets-led enterprise, Motilal Oswal’s earnings are naturally uncovered to cycles. The inventory presently trades at ₹666, down about 40% from its 52-week excessive, and is already pricing in a lot of the current weak spot.

It trades at a price-to-earnings a number of of 16, which is a reduction of about 20% to the 10-year median of 20. A restoration from right here hinges on a pickup in market sentiment and stability in earnings.

Nonetheless, the rising give attention to the distribution enterprise and the huge alternative in asset and wealth administration provide great scope for development. Whereas short-term challenges stay, the long-term outlook stays vivid as a result of rising financialisation of financial savings, mutual fund penetration, and rising variety of high-net-worth people.

For extra such evaluation, learn Revenue Pulse.

Concerning the creator: Madhvendra has over seven years of expertise in fairness markets and has cleared the NISM-Collection-XV: Analysis Analyst Certification Examination. He specialises in writing detailed analysis articles on listed Indian firms, sectoral tendencies, and macroeconomic developments. Comply with him on LinkedIn.

Disclosure: The author doesn’t maintain the shares mentioned on this article.

The aim of this text is simply to share attention-grabbing charts, information factors, and thought-provoking opinions. It’s NOT a suggestion. If you happen to want to think about an funding, you’re strongly suggested to seek the advice of your advisor. This text is strictly for academic functions solely.