AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $15.33 (+56.9%)

EPS YoY +114.3%|

|Web Margin -6.4%

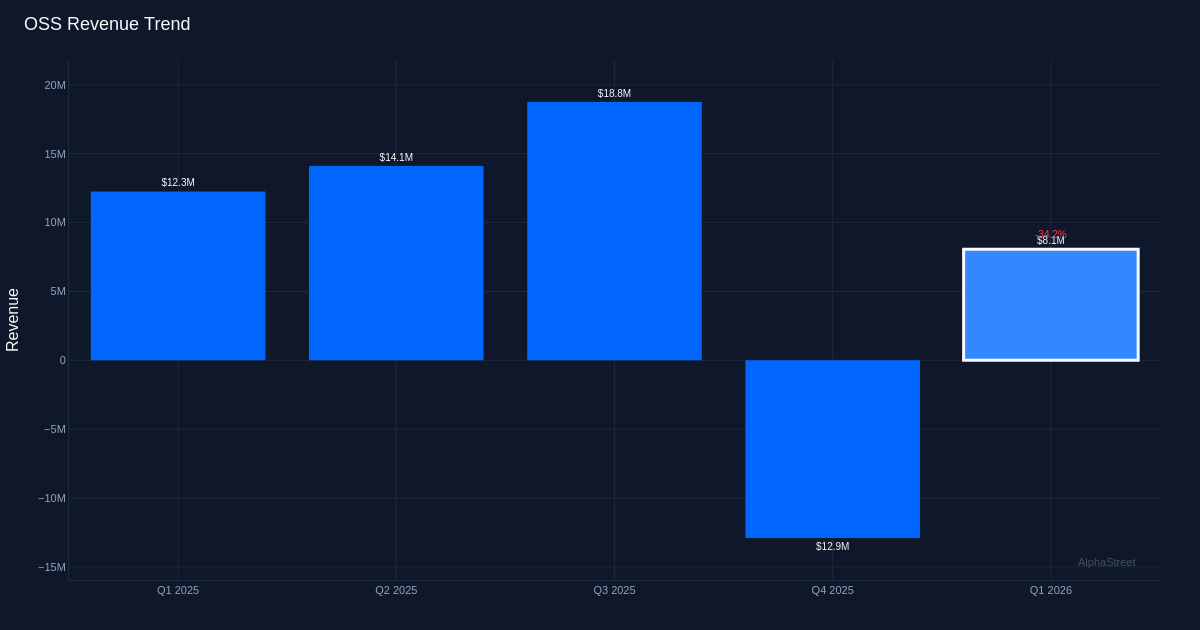

One Cease Methods (OSS) delivered a turnaround in Q1 2026, posting adjusted earnings of $0.01 per share versus analyst expectations of a $0.05 loss—a 120% beat that marked a pointy reversal from the $0.07 loss recorded a 12 months earlier. The efficiency, pushed by a 55% year-over-year income surge to $8.1 million and bolstered by $15 million in new bookings, despatched shares hovering 56.9% to $15.33 as traders embraced the corporate’s bettering operational trajectory and strengthening pipeline.

The standard of the earnings beat deserves scrutiny past the headline numbers. Whereas income progress accelerated sharply, the corporate’s web margin remained destructive at (-)6.4%, although it improved from Q1 2025. The gross margin of 51.5% demonstrates pricing energy and favorable product combine, notably essential within the pc {hardware} area the place element value inflation has pressured friends. Working margin of -8.3%, whereas nonetheless destructive, displays the corporate’s funding section slightly than structural unprofitability. The divergence between gross margin power and working losses factors to fastened value leverage as the important thing variable—as income scales, the trail to sustained profitability seems clearer.

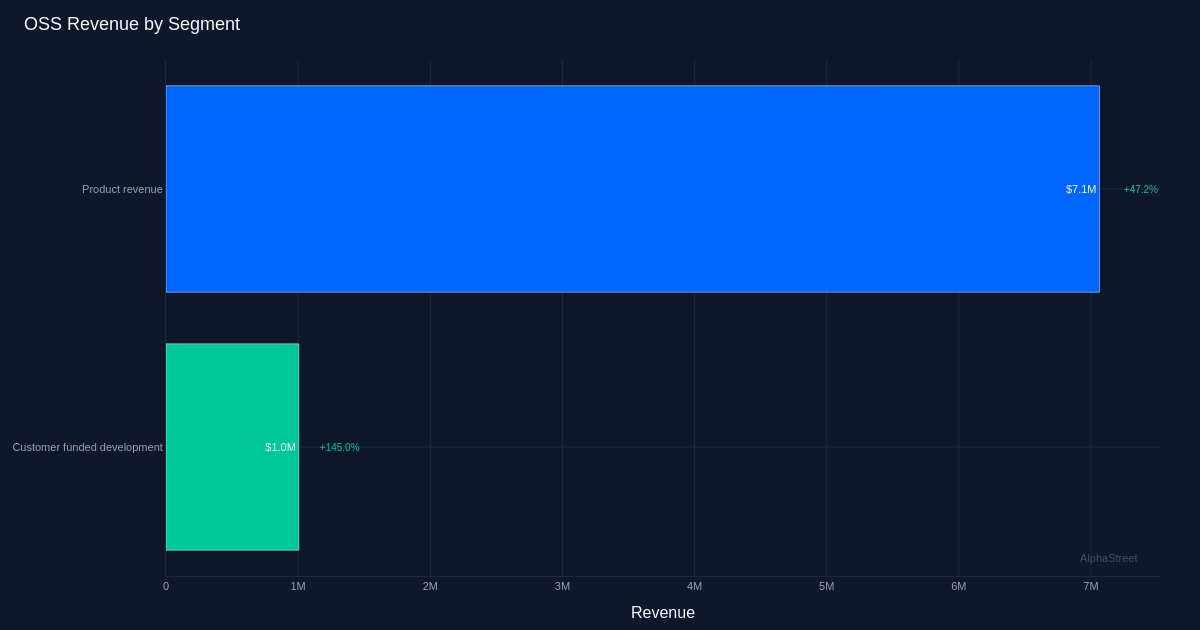

Section efficiency reveals balanced power throughout the enterprise mannequin. Product income of $7.1 million grew 47.2% year-over-year, representing the core industrial engine and accounting for 88% of whole income. Buyer-funded growth income of $1.0 million surged 145%, indicating deepening relationships with strategic clients keen to fund customized options—a high-margin, sticky income stream that usually converts to bigger manufacturing orders. The outsized progress in customer-funded growth suggests design wins that would materialize into important manufacturing quantity in coming quarters, although the timing stays unsure given the project-based nature of this phase.

The forward-looking indicators matter greater than the backward-looking outcomes. The book-to-bill ratio of 1.8 and bookings of $15 million in 1 / 4 that generated $8.1 million in income sign accelerating momentum. Administration emphasised this level: “In the course of the quarter, we generated almost $15 million in new bookings that we anticipate to ship in 2026 and 2027.” This backlog conversion timeline suggests income recognition unfold throughout six quarters, implying a quarterly run-rate of $2.5 million from these bookings alone—earlier than contemplating extra new orders. Administration highlighted particular program visibility, noting “We anticipate this program to generate roughly $2 million in orders in 2026 with a 5 12 months alternative within the vary of an combination 10 million to $15 million.” The corporate’s confidence in 20-30% progress charges seems grounded in tangible pipeline slightly than aspiration, with administration commentary suggesting “that’s main us to have that as we transfer by way of the factored parts of that’s what’s persevering with to strengthen our optimistic feeling concerning the potential to develop at that 20 to 30% vary.”

Provide chain constraints emerge as the first governor on upside potential. An analyst statement throughout the name crystallized the chance value: “It seems like if there weren’t the availability chain points, there’s an opportunity you, you possibly can have truly bumped up your outlook for 2026.” Part availability slightly than demand seems to be the binding constraint, suggesting that as provide chains normalize, the corporate may speed up income conversion from its increasing backlog. This dynamic is especially related in specialised pc {hardware} the place lengthy lead-time elements like customized processors or military-grade components can delay complete system deliveries.

Working money stream of $4.0 million within the quarter—representing 49% of income—offers monetary flexibility uncommon for an organization at this income scale. This money technology, mixed with optimistic web revenue and rising bookings, positions the corporate to self-fund progress with out dilutive capital raises. The money stream power suggests environment friendly working capital administration and favorable fee phrases with clients, essential components for a {hardware} firm navigating element procurement challenges.

The 56.9% inventory surge displays investor enthusiasm for the inflection from constant losses to profitability, however the $15.33 worth should be evaluated towards execution threat. At this stage, the market is pricing in profitable conversion of the $15 million backlog and continued bookings momentum. The valuation seems to low cost materials threat of provide chain disruption or program delays, frequent hazards in protection and specialised computing contracts.

What to Watch: Q2 2026 outcomes will make clear whether or not the book-to-bill power interprets to sustained income progress or if provide chain constraints delay backlog conversion. Monitor gross margin trajectory—sustaining the 51.5% stage whereas scaling quantity would validate pricing energy and favorable combine. Monitor customer-funded growth conversion to manufacturing orders, as this represents the highest-quality income pipeline. Any steering updates on the $10-15 million five-year program alternative and progress towards the 20-30% annual progress goal will sign administration’s confidence in sustaining the inflection.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market info. Human editors confirm content material.