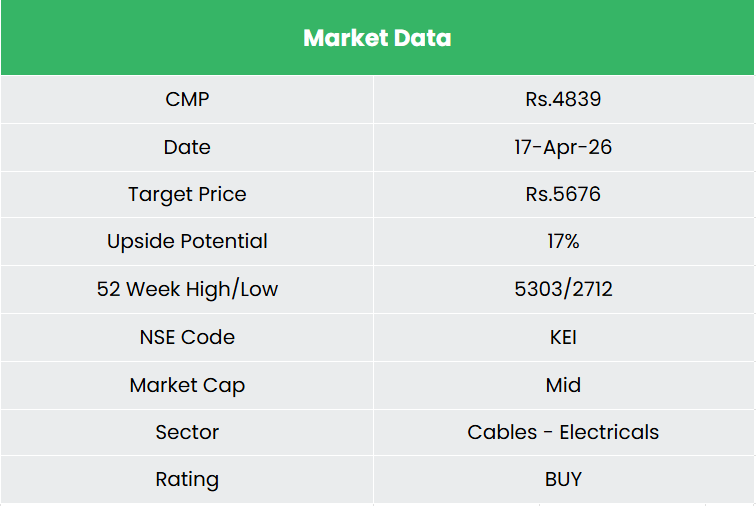

KEI Industries Ltd. – Cables nicely related

KEI Industries Restricted (KEI), integrated in 1992 and headquartered in New Delhi, is considered one of India’s main producers of wires and cables. Its product portfolio spans Additional-Excessive Voltage (EHV) cables as much as 400 kV, HT and LT energy cables, management and instrumentation cables, specialty cables (photo voltaic, rubber, EV, fire-survival, ESP, MVCC), home and winding wires, and stainless-steel wires. The corporate is moreover ahead built-in into EPC providers for energy transmission, distribution, and sub-station tasks.

KEI operates 9 manufacturing crops throughout Rajasthan, Dadra & Nagar Haveli, and Gujarat, supported by an in-house NABL-accredited R&D facility. On the distribution facet, KEI serves 2,000+ institutional clients and reaches retail markets by a pan-India community of over 2100 lively sellers, 27 depots, and 38 advertising places of work. Its export presence spans 60+ international locations throughout 4 abroad places of work. As of thirty first December 2025, KEI carried a consolidated order e-book of ₹37,243 Mn.

Merchandise and Companies

The corporate operates a diversified cables and EPC portfolio spanning EHV (as much as 400kV), HT/LT energy cables, and value-added segments reminiscent of instrumentation, management, and specialty cables (EV, photo voltaic, fire-resistant, marine and offshore). Income publicity is nicely distributed throughout core infrastructure and industrial end-markets, together with energy, oil & fuel, renewables, railways, roads & highways, actual property, and telecom, offering demand visibility and lowering sector-specific cyclicality.

Subsidiaries – As of FY25, the corporate has an affiliate firm and no different subsidiaries/joint ventures.

Funding Rationale

- Sanand Greenfield Growth Driving the Subsequent Part of Development – KEI’s Sanand greenfield enlargement represents a decisive inflection level, transitioning the corporate from being capacity-constrained to structurally growth-enabled, with ~₹2,000 crore capex unlocking ~₹6,000 crore peak income potential over the subsequent 2–3 years. With Part 1 (LT/HT) already operational and full commissioning (together with high-margin EHV) focused by FY27, the ability not solely provides scale however meaningfully upgrades product combine, being the one plant in India to fabricate the complete cable spectrum together with upcoming HVDC capabilities aligned with next-gen grid investments. This comes at an opportune time, with present utilisation at ~76% and a powerful order e-book (~₹3,700 crore), guaranteeing sooner absorption and lowering execution danger. Administration steerage of ~₹2,700 crore income from Sanand in FY27, scaling to full utilisation by FY29 (implying ~3–3.5x asset turns), signifies sturdy capital effectivity. Crucially, progress is predicted to be margin-accretive, supported by working leverage, growing share of EHV and exports, and a structurally enhancing B2C combine. Backed by confirmed institutional credentials in international EHV markets, Sanand positions KEI to straight convert incremental capability into high-quality export and home alternatives, making it a key driver of sustained income progress and profitability enlargement.

- Structural Shift Towards Excessive-Margin B2C Driving Earnings High quality – KEI’s growing tilt towards the B2C (retail) phase, now contributing ~50%+ of revenues marks a structural enchancment in enterprise high quality, with increased margins, higher working capital cycles, and decrease earnings volatility in comparison with the lumpy institutional phase. Supported by sturdy model recall, increasing seller/distributor community, and sturdy demand from actual property and housing, the wires phase (rising ~22–23%) is rising as a constant compounding engine. This shift not solely enhances margin stability but in addition improves return ratios and money movement visibility, making total progress extra sturdy and fewer cyclical.

- Q3FY26 – KEI reported consolidated web gross sales of ₹2,955 crore, up 19.5% YoY, with EBITDA rising 39% YoY to ₹354 crore and PAT rising 42.5% YoY to ₹235 crore. EBITDA margin expanded by ~170 bps YoY to 12.0% (vs 10.29% in Q3FY25), pushed by a richer product combine with the export share rising to ~18% of gross sales and continued traction within the retail phase.

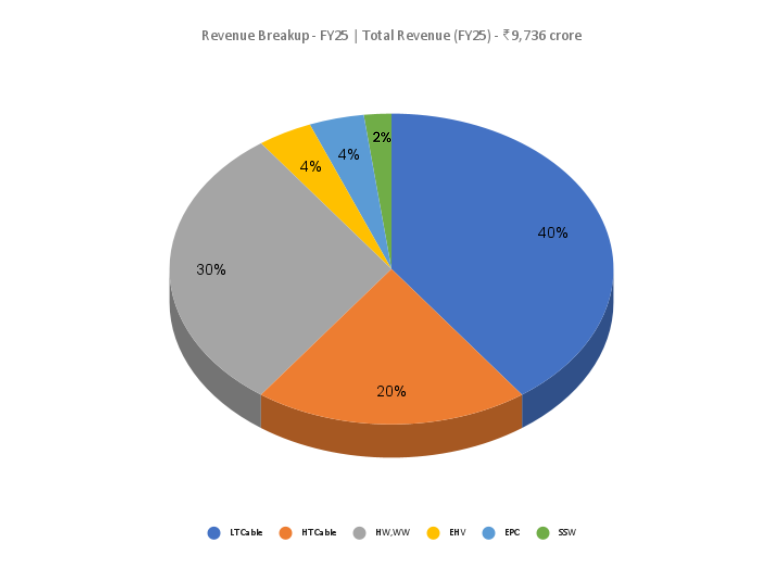

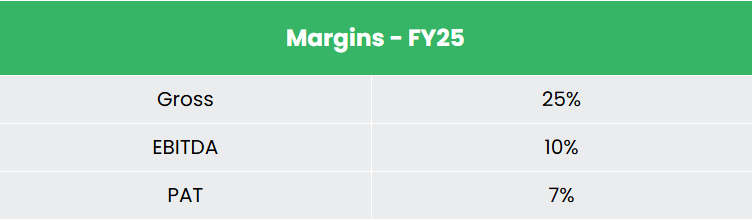

- FY25 – Consolidated web gross sales grew 20% YoY to ₹9,736 crore, with EBITDA at ₹1,063 crore up 20% YoY, posting a margin of 10.92%, and PAT at ₹696 crore, up 20% YoY.

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 19% and 23% respectively between FY23-25. Notably, the TTM income and web revenue progress stand at 22% and 35%. The stability sheet stays largely unencumbered, with a debt-to-equity ratio of 0.04, and the 3-year common ROE and ROCE are round 18% and 25% for FY23-25 interval.

Business

The Indian wires and cables trade constitutes roughly 39% of the broader electrical trade and is predicted to develop at an 11 – 13% CAGR between FY24 and FY29, reaching roughly ₹1,20,000 crore by FY29. Exports have emerged as a high-growth phase – India’s wire and cable exports rose from ₹8,322 crore in FY20 to ~₹16,765 crore in FY24, with an extra 8% YoY enhance recorded between April and October 2024.

Energy demand in India is projected to develop at a 5-7% CAGR between FY25 and FY29, reaching 2,160-2,180 BU. India’s put in energy capability stood at 475.2 GW as of thirty first March 2025, of which renewable power accounted for 220.1 GW (photo voltaic at 106 GW and wind crossing 50 GW). Beneath the Nationwide Electrical energy Plan (2022-32), put in capability is focused to succeed in 609 GW by FY32, with non-fossil sources accounting for 500 GW by 2030, requiring a cumulative funding of ₹33.6 trillion (US$ 384.5 Bn) over the last decade. Inside this, the T&D sector is ready to obtain ₹9.15 lakh crore of funding by FY32 – ₹4.2 lakh crore between 2022-27 and ₹4.9 lakh crore between 2027-32 – funding the addition of 1,91,474 ckm of transmission traces and 1,274 GVA of transformation capability.

Development Drivers

- Energy sector capex and T&D enlargement: Whole energy sector funding is projected to rise 1.7x from ₹14.7 lakh crore over FY19–24 to ₹24.5–25.5 trillion over FY25-29, with inter-regional transmission capability focused at 142,940 MW by FY27.

- Renewable power transition: India’s put in capability is projected to develop from 416 GW in FY23 to an estimated 770-780 GW by FY30, with renewables (ex-hydro) including 310-320 GW at an 18% CAGR to succeed in a 57% share of complete put in capability.

- Development and information centre demand: Development spending within the constructing phase is projected to develop ~1.4x from ₹12.5-13.5 lakh crore over FY20-24 to ₹18-19 lakh crore over FY25-29, whereas India’s information centre operational capability is predicted to almost double from 1,150 MW in December 2024 to 2,000-2,100 MW by March 2027.

- Railway electrification and infrastructure push: Railway electrification is predicted to generate incremental energy demand of ~23 BUs yearly between FY25 and FY29, whereas Union Price range FY26 allotted ₹11.21 lakh crore to the infrastructure sector, straight supporting specialised cable demand throughout metro rail, EV charging, and Good Metropolis tasks.

Peer Evaluation

Rivals: Polycab India Ltd, RR Kabel Ltd, and many others.

Amongst listed friends, KEI stands out for its constant return profile and operational self-discipline. Its FY25 ROCE of 21.3% and nearly debt-free stability sheet (D/E of 0.04x) mirror a well-capitalised progress platform, whereas its working margin of ~10-11% has held regular by commodity cycles. KEI has additionally delivered the sharpest working capital enchancment within the peer set, with debtor days compressing from 118 in FY21 to 67 in FY25. Its FY25 mounted asset turnover of ~10x comfortably outpaces Polycab’s ~7x, underscoring capital effectivity.

Outlook

The outlook stays sturdy, with administration guiding ~20% progress in FY26 supported by sustained demand throughout each retail (B2C) and institutional segments, alongside a gradual enchancment in working margins. Over the medium time period, the corporate targets ~20% CAGR over the subsequent 3–4 years, with EBITDA margins anticipated to succeed in ~11% by FY27, pushed by working leverage and a richer product combine. The wires phase continues to be a key progress driver, anticipated to maintain 22–23% progress, led by sturdy traction within the retail channel. Notably, the B2C phase’s contribution has elevated to ~52% of revenues (vs ~46% earlier), reflecting a strategic shift towards higher-margin, non-cyclical retail enterprise, which boosts margin stability, improves working capital cycles, and reduces dependence on lumpy institutional orders. Capability additions at Chinchpada and Pathredi (~₹1,500–1,600 crore incremental capability) additional assist near-term progress, whereas the institutional phase (~35% of revenues) stays important given excessive entry limitations and robust demand from railways, actual property, and renewables. Backed by continued capex and execution energy, the corporate is focusing on a scale-up to ~₹25,000 crore income over the subsequent 5 years.

Valuations

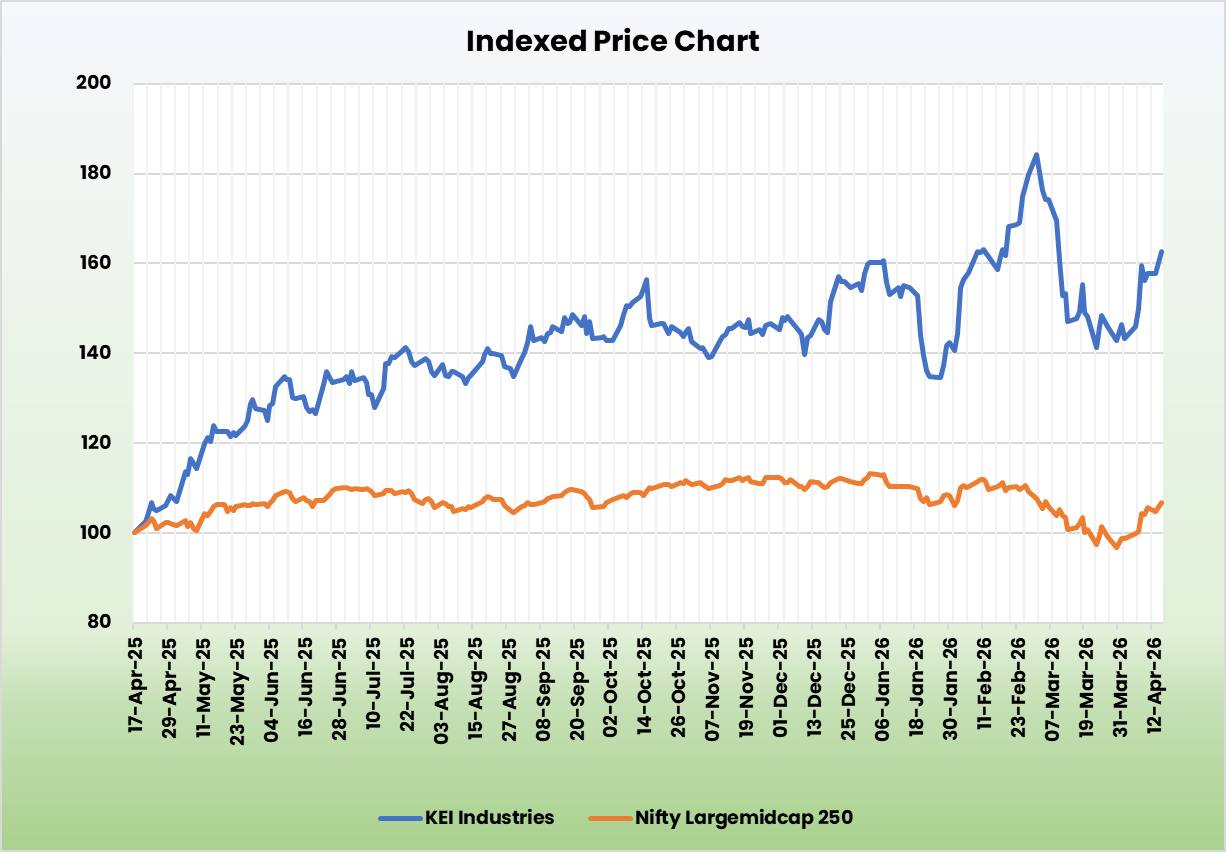

We imagine Sanand-led capability enlargement positions the corporate for a multi-year progress upcycle, unlocking scale, enhancing product combine, and driving margin-accretive earnings progress. We suggest a BUY score within the inventory with the goal value (TP) of Rs.5,676, 45x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back danger successfully.

SWOT Evaluation

| Energy | Weak spot |

|

|

| Alternatives | Threats |

|

|

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you might like

Put up Views:

1,077

{kind=link}