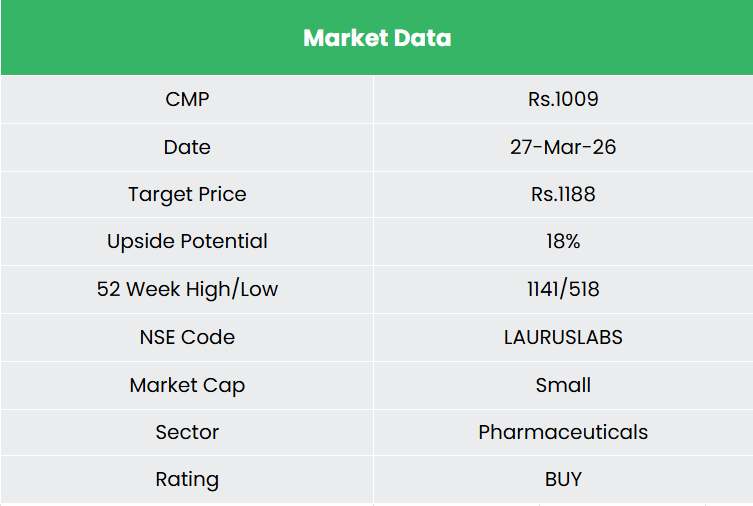

Laurus Labs Ltd. – Chemistry for Higher Dwelling

Laurus Labs Restricted, included in 2005 and headquartered in Hyderabad, India, is a research-driven, built-in pharmaceutical firm with a diversified presence throughout Energetic Pharmaceutical Elements (APIs), Completed Dosage Kinds (FDF), Contract Improvement and Manufacturing (CDMO), and Biotechnology segments, catering to international markets throughout therapeutics resembling antiretrovirals (ARVs), oncology, and different advanced segments. The corporate operates 15 growth and manufacturing amenities, has over 7,800 KL reactor capability, and maintains partnerships with 6 international pharma corporations, supported by a robust R&D engine with 237 patents granted.

Merchandise and Companies

The corporate operates throughout 4 core enterprise segments: Contract Improvement and Manufacturing (CDMO), Generics – Completed Dosage Kinds (FDF) & Energetic Pharmaceutical Elements (API), and Biotechnology.

- CDMO – Gives end-to-end drug growth and manufacturing providers to international pharmaceutical, biotechnology, crop science, animal well being, and specialty ingredient corporations, with key markets together with the US, EU, and Japan.

- Generics (API and FDF) – The corporate is among the many main third-party suppliers of antiretroviral (ARV) APIs globally, supported by one of many largest high-potent API capabilities in India. Its portfolio spans ARV, oncology, steroids, hormones, and cardiovascular therapies, catering to main international generic pharmaceutical corporations. The FDF phase focuses on oral stable dosage formulations.

- Biotechnology – Provides built-in providers starting from clone and pressure engineering to large-scale manufacturing, supporting purchasers throughout the microbial precision fermentation worth chain. Its options cater to areas resembling regenerative drugs, vaccines, and cultured meat.

Subsidiaries: As of FY25, the corporate has 8 subsidiaries, 2 affiliate corporations and a three way partnership.

Funding Rationale

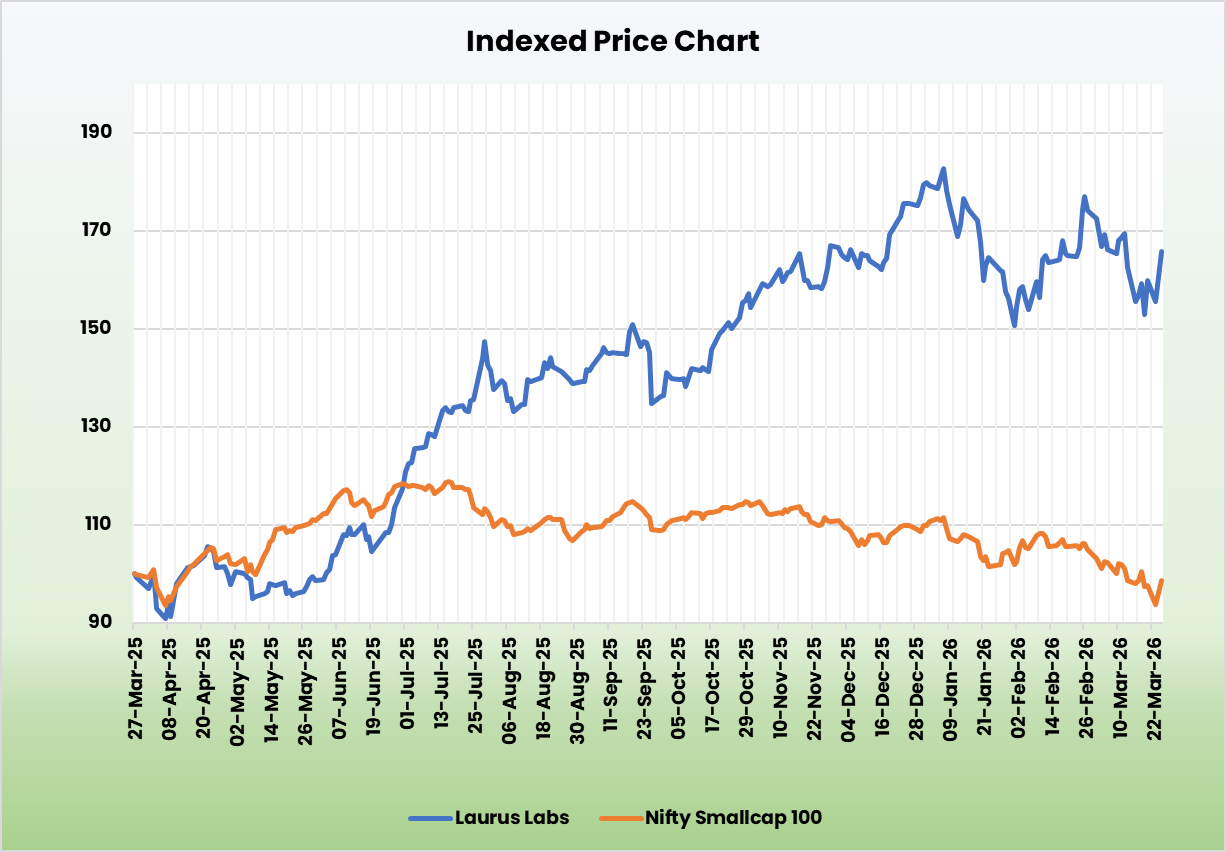

- Quantity pushed generics progress with secure pricing dynamics – Laurus holds one of many strongest positions globally as a provider of ARV APIs, and that is producing secure earnings from the division. The generics enterprise delivered Rs.1,327 crore in Q3FY26 (+37% YoY), pushed primarily by quantity. ARV annual steerage has been revised upward from Rs.2,500 crore to Rs.2,600 crore (±Rs.200 crore), supported by accomplished debottlenecking of ARV manufacturing traces and reallocation of capability, which was disclosed as full in Q2FY26. Past ARV, robust offtake from not too long ago launched merchandise in developed markets (US, Canada, EU) is including a brand new non-ARV FDF income layer. The oral stable facility enlargement is progressing properly, a big a part of the brand new plant capability turned operational in Q3FY26, and the three billion pill capability in Unit II for the KRKA CMO companion got here on-line with income anticipated from Q1FY27. The KRKA Pharma three way partnership is establishing an FDF manufacturing facility in Hyderabad with Section-1 completion anticipated by mid-2027, offering a sturdy European formulation income channel. CMO exercise ranges are rising with good utilisation visibility.

- Scaling a future prepared CDMO platform – The CDMO enterprise grew 43% in 9MFY26, supported by robust recurring enterprise from present long-term buyer relationships. Three industrial NCEs (New Chemical Entity) have been equipped within the final 18 months. Over 110 lively pipeline initiatives are in execution, with a well-balanced combine of massive pharma and mid-sized biotechs. Administration is anticipating the CDMO enterprise to develop Q4FY26. On capability-building: Laurus has made important investments in peptide growth and manufacturing infrastructure, with qualification of commercial-scale peptide amenities anticipated inside CY26. Giant-scale capability enlargement continues at Vizag, increasing capabilities together with peptides, movement chemistry, high-energy chemistries and purifications. The antibody drug conjugate and gene remedy course of growth lab has been operationalised in Hyderabad, and building of the GMP manufacturing facility is on monitor – although significant ADC revenues aren’t anticipated within the subsequent two years, this positions Laurus forward of the curve in next-generation CDMO modalities. Within the Bio division, whereas Q3 was muted, building of the commercial-scale fermentation facility at Vizag is progressing as deliberate, with Section-1 capability of over 400 kiloliters anticipated to be operational by finish of 2026, unlocking the following leg of Bio CDMO progress. Administration expects CDMO’s contribution to complete revenues to develop over time (presently 30%).

- Margins increasing, stability sheet strengthening – EBITDA margins have expanded each single quarter for 3 consecutive quarters – 24.8% → 26.0% → 27.3%, pushed by higher product combine and working effectivity, with administration guiding a 60% gross margin ground for Q4FY26 and FY27. ROCE has improved progressively from 12.7% to 16.3% to 18.5% during the last three quarters, with additional enchancment guided. Concurrently, the stability sheet has been quickly deleveraged and working money movement of Rs.1,477 Cr in 9MFY26 comfortably self-funds the Rs.735 crore CAPEX deployed in the identical interval.

- Q3FY26 – In Q3, the corporate reported a income of Rs.1,778 crore, up 26% YoY. EBITDA grew 70% YoY, to Rs.485 crore, pushed by a large enlargement in EBITDA margins of 720bps to 27%. PAT elevated 174% Rs.252 crore (14.2% margin, up from 6.5% in Q3FY25).

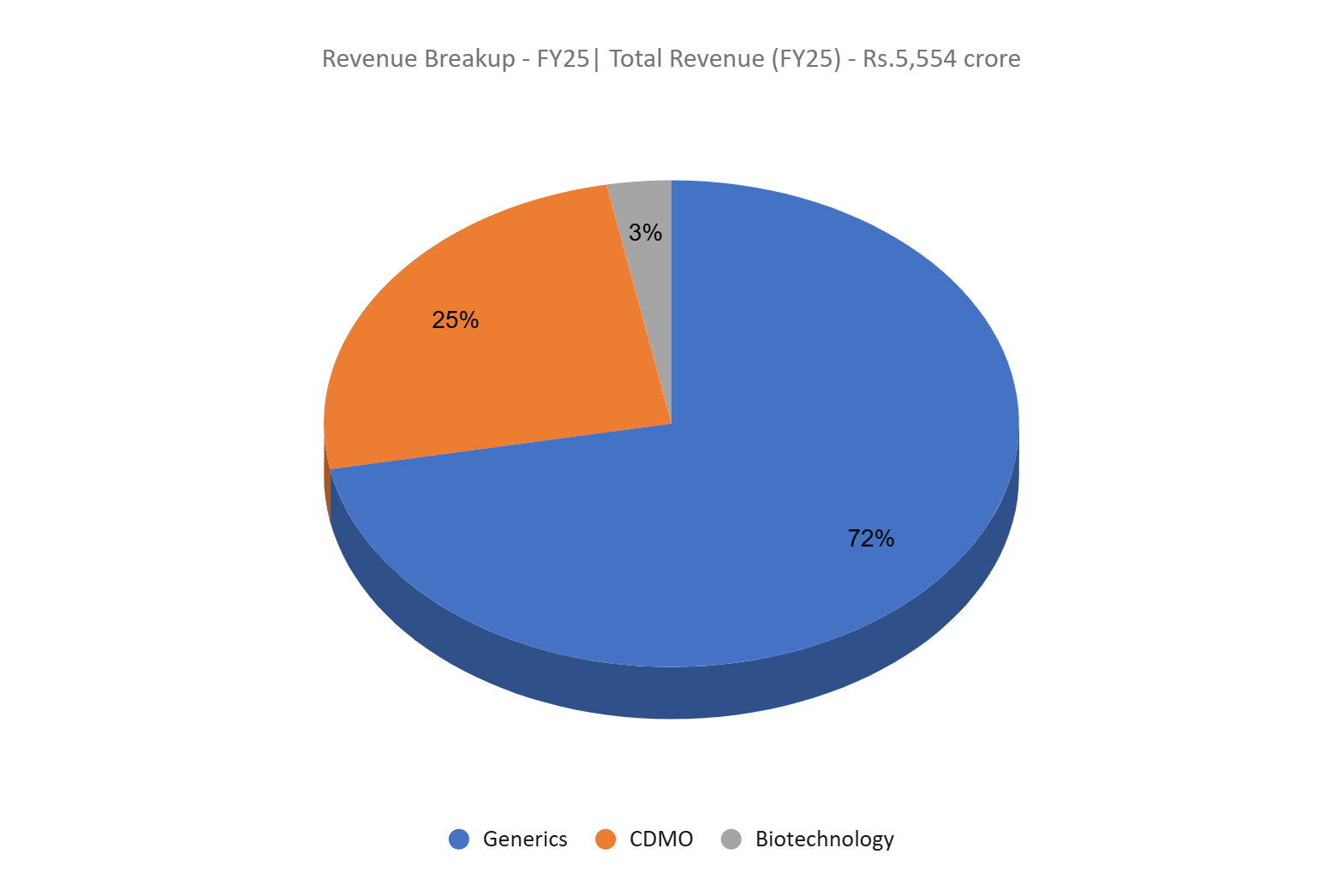

- FY25 – In FY25, income grew 10% YoY to Rs.5,554 crore. EBITDA was recorded at Rs.1,115 crore (20% Margin), up 40% YoY, and PAT grew 112% YoY to Rs.358 crore.

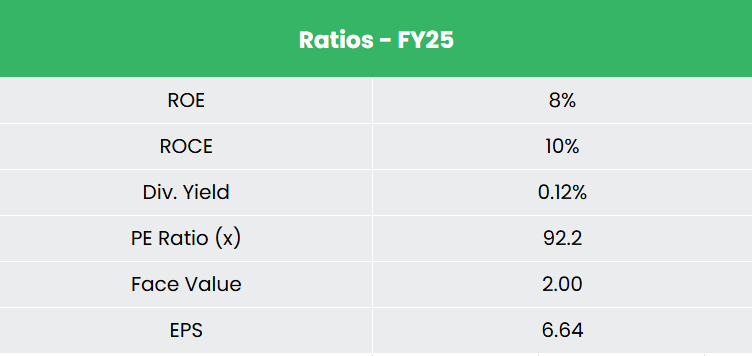

- Monetary Efficiency – The three-year income and internet revenue CAGR stand at 4%, and -27%, nevertheless, the TTM income and internet revenue progress have drastically improved to 27% and 321%, respectively. The three-year common ROE and ROCE are round 11% and 13%, and the corporate carries a debt-to-equity ratio of 0.46, serviced by an curiosity protection ratio of ~7x.

Business

The Indian pharmaceutical business is a worldwide chief in generic medicines and low-cost vaccines, rating because the world’s third largest market by quantity and 14th by worth. In accordance with Bain & Co., the Indian pharmaceutical market was valued at Rs. 4,71,295 crore (US$ 55 billion) in 2025 and is projected to succeed in Rs. 10,28,280–11,13,970 crore (US$ 120–130 billion) by 2030. India contributes 20% of worldwide generic exports by quantity and provides 55-60% of UNICEF’s vaccines and 99% of WHO DPT vaccine demand, underscoring its manufacturing depth and price benefits.

Development Drivers

- FDI & Coverage Help – 100% FDI is permitted underneath the automated route for greenfield pharmaceutical initiatives, with 74% permitted for brownfield investments.

- Rising Healthcare Demand & Power Illness Burden – India’s rising center class, increasing healthcare entry, and rising prevalence of continual diseases resembling diabetes, cardiovascular issues, and CNS situations proceed to drive long-term demand.

- Enlargement of Home Manufacturing & API Self-Reliance – Authorities schemes such because the Manufacturing-Linked Incentive (PLI) for prescription drugs, bulk drug parks, and help for KSM/API manufacturing are lowering import dependence and enabling large-scale home capability creation.

Peer Evaluation

Rivals – Zydus Lifesciences Ltd, Cipla Ltd, and so on.

In comparison with friends resembling Cipla and Zydus Lifesciences, Laurus Labs has a comparatively greater publicity to APIs and CDMO, positioning it extra upstream within the pharmaceutical worth chain, alongside its formulations enterprise. In distinction, friends have a bigger presence in branded formulations, significantly in home markets.

The corporate’s comparatively decrease return ratios are in step with its ongoing funding section, marked by capability enlargement and investments in new capabilities, which usually contain longer gestation durations earlier than full utilization and working leverage advantages are realized.

Outlook

Administration has guided gross margins of roughly 60% for Q4FY26 and thru FY27, supported by a beneficial product and division combine, with EBITDA margins anticipated to enhance additional as working leverage builds. ROCE, which has improved progressively to 18.5% during the last three quarters, is guided to maneuver greater as asset utilisation will increase towards the normalised 1.1x goal. Probably the most crucial near-term sign to look at is Q4FY26 CDMO efficiency, administration has explicitly dedicated to CDMO rising year-on-year over Q4FY25 (Rs.461 Cr), and supply on this may affirm that the enterprise is transitioning from lumpy development-led campaigns to recurring industrial provides, which administration has guided will represent the vast majority of FY27 CDMO revenues. On ARVs, the annual run price has been revised upward to Rs.2,600 ± 200 Cr following accomplished capability debottlenecking, with progress remaining volume-led and secure although continued monitoring of PEPFAR and World Fund procurement choices stays important given ARV’s ~40% contribution to complete revenues.

Valuations

We consider Laurus Labs is coming into a section of earnings re-rating, supported by secure generics money flows and a CDMO phase scaling from development-led revenues to industrial provides. We suggest a BUY score within the inventory with the goal worth (TP) of Rs.1,188, 60x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully.

SWOT Evaluation

| Energy | Weak spot |

|

|

| Alternatives | Threats |

|

|

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please observe that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

1,423

Stabilized This fall Gross sales, however Fiscal 2027 Outlook Is Nonetheless the Actual Story")

{kind=link}