AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $7.76 (+4.3%)

EPS YoY -76.6%

|

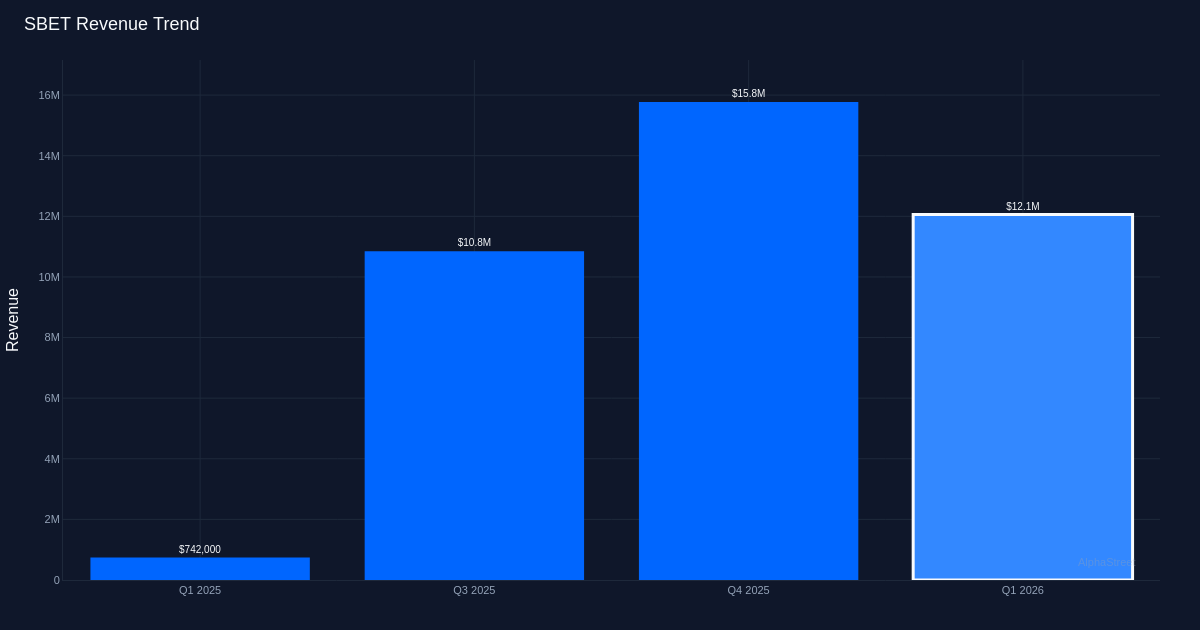

Sharplink (SBET) delivered a Q1 2026 earnings miss, reporting a loss per share of $3.25 in opposition to analyst expectations of a $0.01 loss—a miss that raises elementary questions in regards to the firm’s enterprise mannequin viability regardless of explosive income progress. The capital markets agency posted $12.1 million in income, marking a pointy year-over-year progress, but managed to burn by way of $685.6 million in web losses through the quarter. The inventory’s 4.3% uptick to $7.76 suggests buyers are specializing in the income trajectory reasonably than the alarming deterioration in profitability.

The standard of Sharplink’s progress is deeply troubling, with working leverage shifting within the flawed course at scale. Administration acknowledged the associated fee explosion, noting “SG&A bills within the first quarter had been $9.9 million in comparison with $1.1 million within the prior 12 months quarter,” however the nine-fold improve in working bills doesn’t clarify the 700-fold improve in web losses. The mathematics factors to important non-operating prices or asset impairments that administration has not totally disclosed in accessible commentary.

Profitability developments throughout current quarters paint an image of maximum instability reasonably than growth-stage predictability. The wild swings in current quarters —from worthwhile to massively unprofitable and again—point out both distinctive income high quality points or substantial one-time prices that aren’t being clearly communicated. Administration’s remark that “web loss for the quarter ended March 31, 2026 was $685.6 million versus $1 million loss within the prior 12 months” states the very fact however presents no clarification for the 685x deterioration.

Administration’s strategic pivot towards tokenized real-world belongings and liquid restaking suggests an try and journey rising crypto infrastructure developments, however the connection to present financials stays opaque. The commentary that “in January we took a portion of our portfolio round 8% and we put it in a composable liquid restaking token alongside Consensus, Linea, Etherfi and Eigencloud” signifies lively treasury administration of the substantial ETH place, however gives no readability on how this generated $12.1 million in quarterly income or produced a $685.6 million loss. The statement that “so far there’s about 30 to 35 billion of on chain actual world belongings which have been tokenized” positions Sharplink in a rising market, however with out disclosure of the corporate’s market share, income mannequin, or unit economics on this area, buyers are left connecting dots with out adequate knowledge factors.

The earnings miss comes in opposition to minimal analyst protection and expectations, with the corporate posting a 0% beat charge over the past quarter of reported outcomes. The truth that consensus anticipated a near-breakeven quarter at a $0.01 loss whereas the corporate delivered 325x that loss suggests both a catastrophic breakdown in steering communication or analysts working with incomplete details about the enterprise mannequin. For a monetary providers agency in capital markets, this degree of forecasting disconnect is especially problematic, because it suggests the income and expense drivers are neither clear nor predictable.

The constructive inventory response regardless of the large earnings disappointment signifies the market is both pricing in asset worth from the ETH holdings reasonably than working efficiency, or viewing the income progress as validation of a viable enterprise rising from growth stage. At $7.76 per share with 4.02 ETH per share in holdings, buyers seem like assigning enterprise worth primarily based on the cryptocurrency focus reasonably than conventional earnings multiples. This creates a hybrid valuation framework the place Sharplink trades partly as a levered guess on Ethereum and partly as a capital markets platform, however the 4.3% achieve suggests the previous is driving sentiment greater than working fundamentals.

What to Watch: Administration should present detailed reconciliation of the $685.6 million web loss, breaking out working losses from any asset impairments or mark-to-market prices on the ETH portfolio. The sustainability of the income mannequin wants clarification—particularly whether or not the $12.1 million represents recurring platform charges, transaction-based income, or positive aspects from treasury administration. Sequential income developments in Q2 will reveal whether or not Q1’s decline from This fall was seasonal or structural. Lastly, buyers want transparency on the corporate’s money burn charge and runway given the magnitude of losses, together with any hedging technique for the concentrated Ethereum publicity that represents over half the market capitalization on a per-share foundation.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market info. Human editors confirm content material.