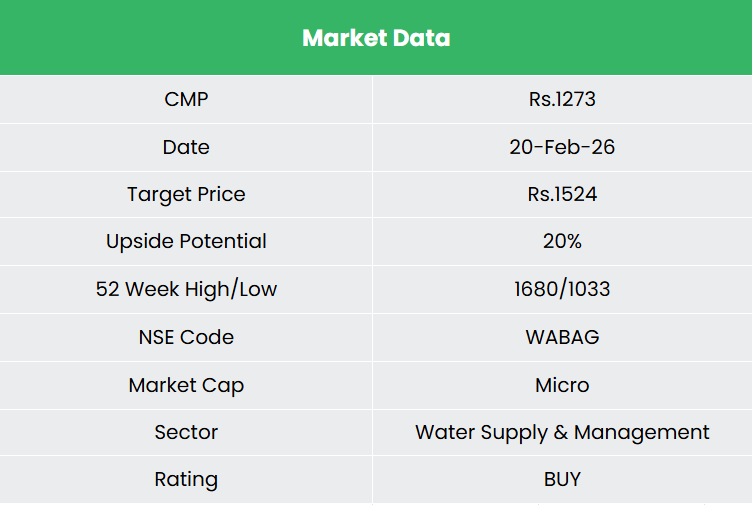

Va Tech Wabag Ltd. – World Water Options Supplier

Included in 1995 and headquartered in Chennai, VA Tech Wabag Restricted (WABAG) is a pure-play Indian multinational firm targeted completely on water and wastewater remedy. The corporate operates in over 25 international locations throughout 4 continents and is recognised among the many world’s prime three personal water operators and the third-largest desalination participant globally. Since inception, WABAG has executed greater than 1,500 vegetation (over 6,500 installations globally throughout legacy operations), supported by 125+ in-house proprietary applied sciences and devoted R&D centres in Europe and India, reinforcing its place as a technology-driven international water options chief.

Merchandise and Companies

WABAG affords end-to-end water and wastewater administration options throughout all the lifecycle from challenge improvement and EPC execution to long-term O&M. The corporate’s choices spans ingesting water remedy, desalination, wastewater remedy, recycle & reuse, effluent remedy, ZLD, sludge remedy & power restoration.

Subsidiaries: As of FY25, the corporate has 15 subsidiaries and a couple of affiliate firms.

Funding Rationale

- Capturing the Water Demand from New Age Industries – Past its core municipal portfolio, WABAG is strategically aligning with India’s subsequent capex wave throughout photo voltaic PV, inexperienced hydrogen, semiconductors, knowledge centres and bio-energy sectors which are inherently water-intensive and require high-purity, dependable and recyclable water options. Photo voltaic cell and semiconductor manufacturing rely upon ultra-pure water (UPW) for wafer cleansing and course of stability; inexperienced hydrogen requires demineralised and desalinated water as feedstock; whereas knowledge centres demand giant volumes of handled water for cooling with rising regulatory emphasis on reuse. WABAG’s breakthrough UPW order from RenewSys Photo voltaic and the Rs.1,000 crore 100 MLD desalination challenge for Indosol Photo voltaic Non-public Restricted display confirmed execution functionality throughout desalination, tertiary RO, effluent remedy and ZLD techniques. With India concentrating on 130 GW photo voltaic manufacturing and accelerating hydrogen and semiconductor investments, incremental demand for 100 – 150 MLD of high-purity and recycled water capability is prone to materialise over the medium time period. WABAG’s confirmed experience coupled with ongoing engagements and superior bidding discussions with hydrogen builders, semiconductor fabs and knowledge centre operators positions it as a most popular expertise associate relatively than a commoditised EPC contractor. These segments supply larger technical entry limitations, recurring O&M potential and superior margin profile, offering a multi-year progress runway and potential valuation re-rating as the corporate transitions from municipal EPC to a high-value industrial water options platform.

- Sturdy Order E book with Sturdy Worldwide Diversification – WABAG ended Q3FY26 with a sturdy order guide of Rs.163 billion, providing sturdy multi-year income visibility with a balanced mixture of 64% EPC and 36% O&M, supporting each execution progress and annuity stability. Worldwide tasks contribute ~50% of income (YTD) and order backlog, underscoring geographic diversification. The corporate continues to consolidate its Center East management with the 300 MLD SWA desalination mega challenge at Yanbu Al-Bahr, KSA, a 50 MLD BWRO plant in Saudi Arabia and most popular bidder standing for the Hadda ISTP challenge. It additionally secured an ADB-funded DBO order from the Melamchi Water Provide Improvement Board, Nepal, strengthening its South Asia presence. Multilateral-funded tasks such because the JICA-backed 400 MLD Perur desalination plant in Chennai and World Financial institution/AIIB-supported tasks in Bangladesh and Bengaluru improve counterparty high quality. With Rs.1,200 crore order consumption in Q3, improved working capital days and debt discount, WABAG displays disciplined execution alongside scale growth.

- Q3FY6 – In the course of the quarter, the corporate reported consolidated income from operations of Rs.961 crore, up 18.5% YoY in comparison with Rs.811 crore in Q3FY25. EBITDA elevated 24.6% YoY to Rs.131 crore from Rs.105 crore, with EBITDA margin enhancing to 13.6% versus 13.0% within the corresponding quarter final 12 months. Consolidated internet revenue stood at Rs.92 crore, registering a 30.6% YoY progress from Rs.70 crore in Q3FY25.

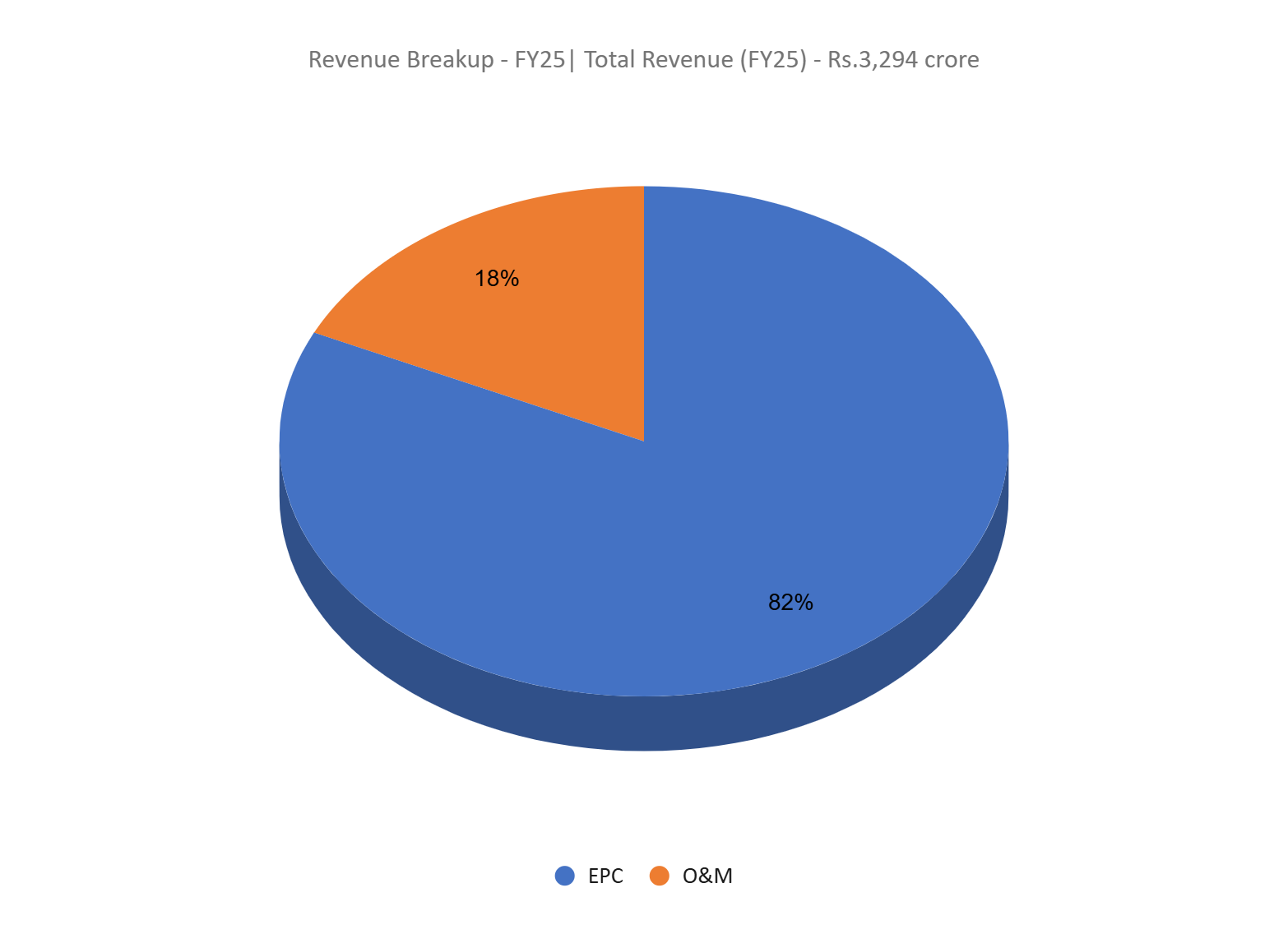

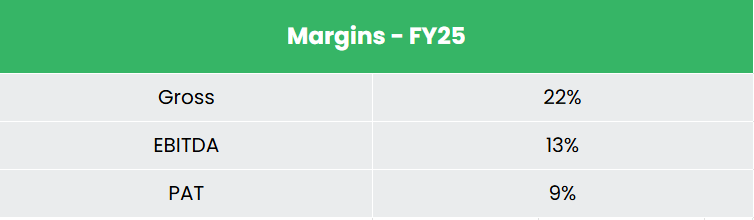

- FY25 – Throughout FY25, the corporate reported a income of Rs.3,294 crore, representing a 15% YoY enhance in comparison with Rs.2,856 crore in FY24. EBITDA stood at Rs.430 crore, up ~14% YoY from Rs.377 crore within the earlier 12 months, and internet revenue was recorded at Rs.295 crore, registering an ~18% YoY progress over Rs.250 crore in FY24.

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 3% and 32% respectively between FY23-25. Notably, the TTM income progress has materially improved to twenty%. The corporate has a debt-to-equity ratio of 0.1, and the 3-year common ROE and ROCE are round 11% and 20% for FY23-25 interval.

Trade

The worldwide water remedy trade is witnessing regular structural progress, pushed by rising water shortage, urbanisation and tightening environmental laws. The worldwide water and wastewater remedy market was valued at roughly US$ 347.9 billion in 2024 and is projected to achieve US$ 623.2 billion by 2034, implying a CAGR of ~7.6%, supported by rising investments in wastewater administration, desalination and water reuse infrastructure. Regionally, Asia-Pacific stays the fastest-growing market, anticipated to develop from US$ 125.6 billion in 2024 to US$ 282.8 billion by 2034 (8.5% CAGR), pushed by fast industrialisation and concrete infrastructure investments. Authorities-led spending continues to underpin demand, together with India’s water sector allocation of Rs.99,500 crore and Africa’s Water Funding Motion Plan concentrating on US$30 billion annual investments by 2030, highlighting sturdy long-term progress visibility for water remedy resolution suppliers.

Development Drivers

- Coverage-led infrastructure spending – Massive authorities programmes akin to Nationwide Mission for Clear Ganga, AMRUT, AMRUT 2.0, Jal Jeevan Mission and Swacch Bharat Mission and international water safety investments are driving sustained challenge pipelines throughout municipal and industrial segments.

- Water shortage and local weather stress – Local weather fashions predict that almost two-thirds of the worldwide inhabitants might face water stress by 2030, accelerating adoption of desalination and reuse options.

- Industrial water demand – Growth in refining, petrochemicals, semiconductors and power sectors is rising demand for effluent remedy and ultrapure water techniques.

- Regulatory tightening and sustainability focus – Stricter environmental norms are driving adoption of superior wastewater remedy and recycling applied sciences globally.

Peer Evaluation

Opponents – Ion Alternate (India) Ltd, Enviro Infra Engineers Ltd, and many others.

In comparison with friends, WABAG stands out for its superior money conversion and steadiness sheet energy, regardless of delivering average return ratios. The corporate has reported a CFO/PAT (3yr median) of 1.68x, considerably stronger than ION Alternate (0.15x) and Enviro Infra (-0.27x), indicating materially higher earnings high quality and dealing capital self-discipline. Wabag additionally maintains a low debt-to-equity ratio of 0.10x, among the many lowest within the peer set, supporting liquidity and lowering execution threat inherent in EPC companies.

Outlook

WABAG is concentrating on a calibrated growth in worldwide markets, with a transparent strategic concentrate on the Center East, Africa, CIS, Southeast Asia and South Asia, the place desalination and water reuse demand stays structurally sturdy. The corporate continues to observe an asset-light engineering-led mannequin, supporting superior money era and wholesome return ratios. With EBITDA margins sustaining inside the guided 13–15% vary and income progress of ~18% aligning with medium-term steerage, operational momentum stays intact. A powerful liquidity place gross money of Rs.1,080 crore and internet money of Rs.891 crore as of December 2025 supplies flexibility to pursue giant and sophisticated tasks. Backed by a diversified order guide, enhancing working capital effectivity and powerful worldwide tender pipeline, WABAG stays properly positioned to ship regular progress with disciplined capital allocation.

Valuations

At present ranges, we imagine the inventory affords a compelling play on a globally diversified, asset-light water infrastructure platform with enhancing margins, sturdy money place and multi-year income visibility. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.1,524, 20x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back threat successfully.

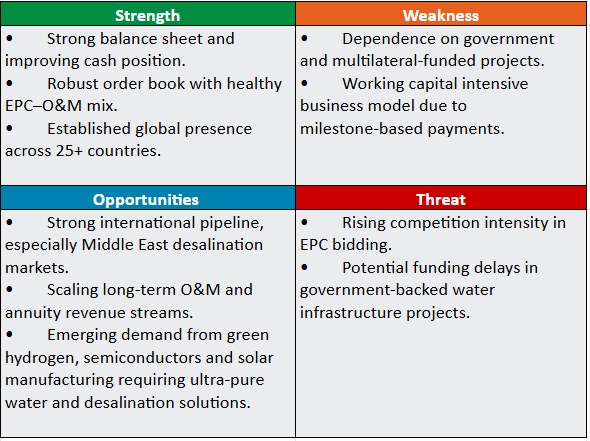

SWOT Evaluation

![]()

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles you could like

Submit Views:

1,908

{kind=link}