AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $13.26 (-0.5%)

EPS YoY -55.6%|Rev YoY +0.0%|Internet Margin 1.7%

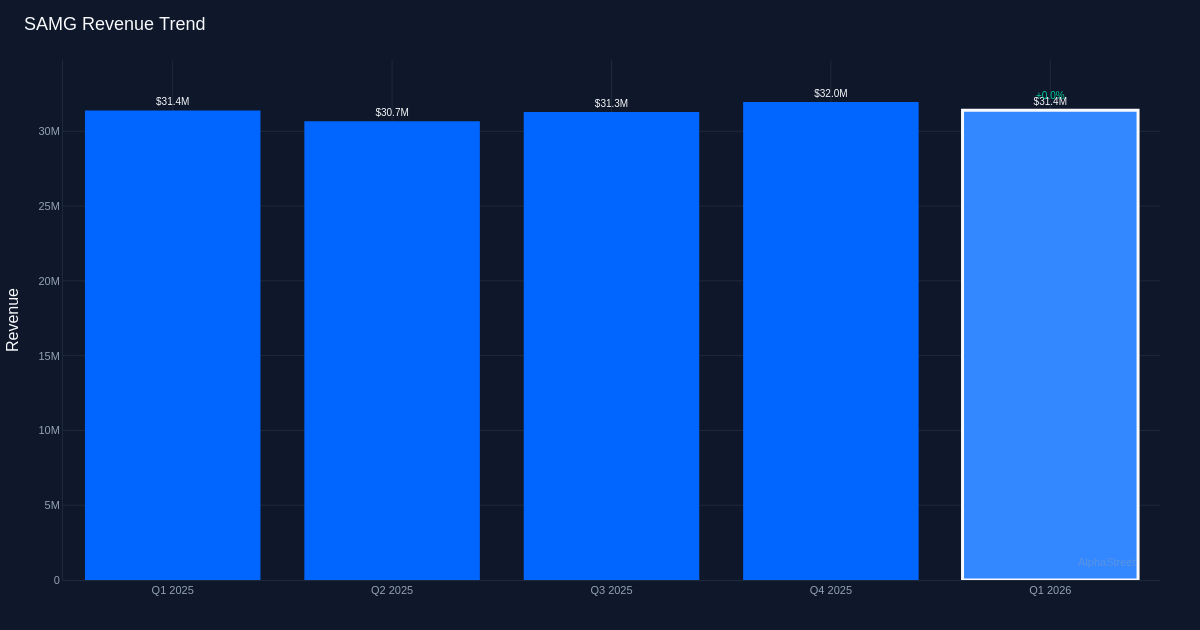

A regarding margin collapse overshadowed Silvercrest Asset Administration’s (SAMG) Q1 2026 outcomes, because the wealth and funding supervisor missed earnings estimates by 45.5%. The corporate reported adjusted EPS of $0.12 versus consensus expectations of $0.22, whereas income of $31.4M primarily matched each estimates and prior-year outcomes. The magnitude of the earnings miss relative to the modest income shortfall alerts a basic profitability downside fairly than a easy top-line stumble.

Margin compression tells the actual story behind this quarter’s disappointment. Internet revenue collapsed to only $533,000 from $3.9M within the year-ago interval, driving web margin right down to 1.7% from 12.4% a yr earlier—a surprising 10.7 share level contraction. This deterioration occurred regardless of income remaining fully flat year-over-year at $31.4M, indicating pure operational deleveraging. Administration acknowledged the associated fee stress straight, noting “we had been working a 60% of income for compensation a yr in the past,” implying that compensation expense has risen as a share of income and is materially impacting profitability. For an asset administration agency the place expertise retention is crucial however the place working leverage ought to theoretically enhance with scale, this inverse relationship between steady income and collapsing margins raises questions in regards to the sustainability of the enterprise mannequin at present staffing ranges.

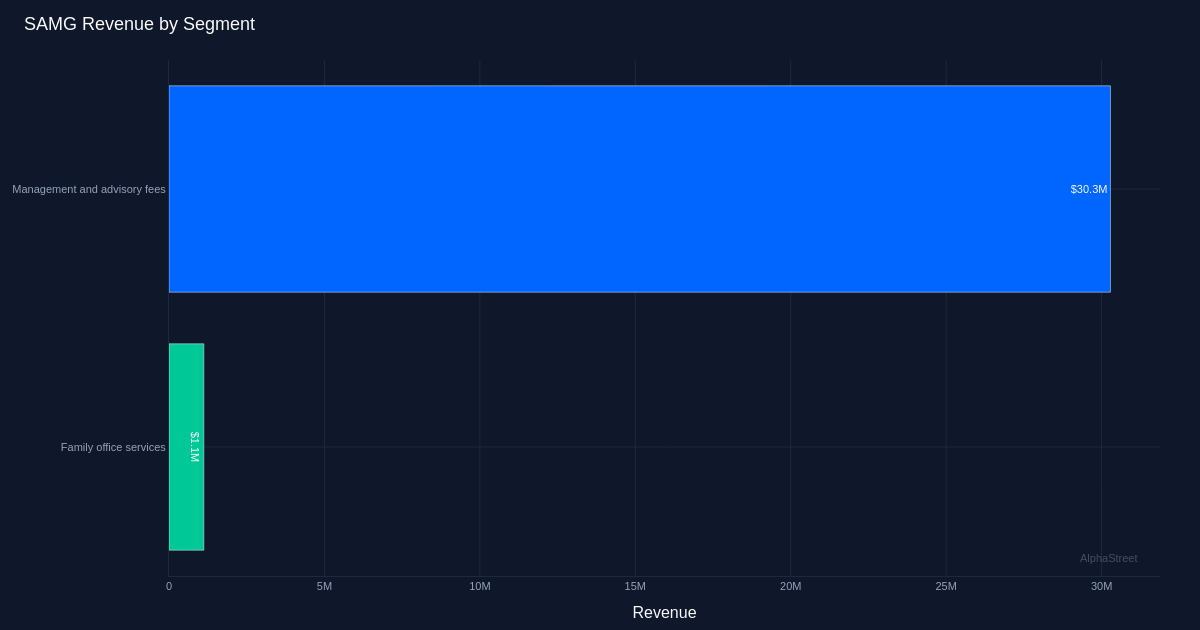

Belongings below administration present modest progress however haven’t translated to profitability positive factors. Administration famous that “12 months over yr Whole AUM grew 1.1% to $35.7 billion, up from $35.3 billion as of March 31, 2025,” whereas present information reveals whole belongings below administration at $36 billion with discretionary AUM at $23.1 billion. The income breakdown reveals administration and advisory charges of $30.3M comprising the overwhelming majority of the $31.4M whole, with household workplace providers contributing simply $1.1M. The issue isn’t shopper defection—AUM is rising—however fairly the lack to keep up pricing energy or management bills because the asset base expands. In asset administration, incremental AUM ought to drop disproportionately to the underside line given the largely mounted price base; the alternative is happening right here.

Capital allocation priorities seem targeted on shareholder returns regardless of deteriorating operations. Administration disclosed that “In the course of the first quarter of this yr, we repurchased Class A shares totaling roughly 1.9 million, which represented the completion of our beforehand introduced $25 million inventory repurchase.” Finishing a considerable buyback program whereas web margins compress to 1.7% and quarterly web revenue sits at simply $533,000 raises questions on whether or not capital could be higher deployed addressing the underlying operational challenges. The corporate generated EBITDA of $3.7M within the quarter, offering some cushion above web revenue, however even this metric seems weak relative to the income base.

Administration’s characterization of the quarter as “okay” understates the severity of the margin deterioration. In discussing efficiency, administration famous “It was a reasonably good quarter within the fourth quarter of final yr on that foundation and it was okay for the primary quarter of 2026.” This sanguine evaluation appears disconnected from a 55.6% year-over-year EPS decline and a web margin that has contracted by practically 11 share factors. Administration additionally highlighted that “Adjusted web revenue, which we outlined as web revenue with out giving impact to non core non recurring objects and revenue tax expense, assuming a company charge of 26% was roughly 1.5 million for the quarter or $0.13 and $0.12 per adjusted fundamental and diluted EPS respectively.” Even on this adjusted foundation, earnings stay considerably beneath year-ago ranges and fell wanting analyst expectations.

The muted inventory response suggests traders could have anticipated weak spot or are ready for a clearer turnaround narrative. Shares had been largely unchanged following the report regardless of the substantial earnings miss, indicating both that the deterioration was already mirrored in expectations or that the market is giving administration time to handle price construction points. The corporate’s current observe file provides little consolation—it has overwhelmed estimates in zero of the final one quarter, representing a 0% beat charge.

What to Watch: The compensation expense ratio would be the crucial metric in Q2 2026—traders must see proof that administration can stabilize this line merchandise as a share of income. AUM developments will point out whether or not shopper relationships stay intact, however margin restoration is the actual take a look at. Any steerage on the trail again to double-digit web margins would offer mandatory visibility. Lastly, look ahead to administration commentary on whether or not the finished buyback represented opportunistic capital deployment or alerts confidence in near-term operational enchancment, as the reply will dictate whether or not extra shareholder returns make sense earlier than profitability stabilizes.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market data. Human editors confirm content material.